Page 2 of 2

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 8:41 am

by International

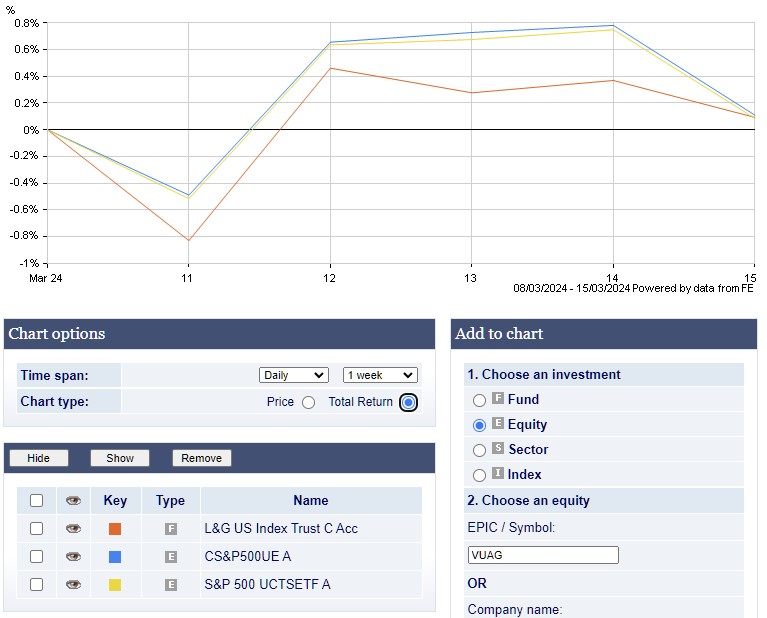

And this is a narrower view (from HL's charts this time).

that seems to show the OEIC (orange) falling relative to the ETFs from the start of the period.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 9:08 am

by GeoffF100

International wrote:I'd be converting >500K in the first go around so losing 1% would be 5 years of current platform fees! Not the planned saving.

So to mitigate I could:

1) Do things in stages, like dollar-cost-averaging

2) Sell the OEIC, taking note of when I did that. Don't buy the EFT until it has swung below (relatively) what I sold the OEIC for

Even if I stick with OEICs and move to another platform I am still going to do a tidy up so the need to avoid swings in the wrong direction still stands.

Option 1. Yes, that is sensible. You would probably have difficulty doing a £500K+ ETF trade at quote anyway. £50K trades would make more sense.

Option 2. The ETF price may never swing below what you paid for the OEIC, and you will be out of the market, potentially losing ground against both funds while you wait. (The crossover point depends on the starting point for the graph, by the way.) You cannot, of course, guarantee to sell the OEIC when its price is above that of the ETF, because it is forward priced.

If tidying up is costly, you meed to question whether it is worth it. Tidy portfolios are not necessarily any more profitable than untidy ones.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 10:02 am

by International

GeoffF100 wrote:If tidying up is costly, you meed to question whether it is worth it. Tidy portfolios are not necessarily any more profitable than untidy ones.

Yes, I agree that. The context is here:

viewtopic.php?t=42245 . I'm looking to reposition myself to be retired (or FI at least) and this whole platform/OEIC/ETF decision is driven by my realisation that I am haemorrhaging platform fees which are dragging me by ~0.2% in my ISA and arguably ~0.17% in my pension.

When we get to retirement withdrawal rates where I think about numbers like growth of 5% less inflation of 3%, leaving 2% then 0.2% drag seems a lot!

I appreciate your help with thinking through the potential switch costs.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 10:37 am

by EthicsGradient

International wrote:And this is a narrower view (from HL's charts this time).

that seems to show the OEIC (orange) falling relative to the ETFs from the start of the period.

The L&G OEIC tracks the

FTSE USA index, not the S&P 500. It's similar (587 constituents), but not identical, so you expect variations, and not because of the OEIC v. ETF comparison.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 10:54 am

by paulnumbers

one good argument in favour of ETF's is that there are many brokers available for them that do not have percentage fees, whereas for OEIC's they are few and far between.

And with the current crop of cashback deals, it can be quite profitable switching between brokers once a year.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 11:22 am

by tjh290633

Some M&G funds used to be quoted on the stock exchange, in the 1970s and earlier

TJH

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 12:29 pm

by Lootman

Vanguard popularised index fund investing for retail clients, certainly. But they did not invent indexing, whose roots can be traced back to the 1970s or earlier. Institutions were using index funds before individual investors - Wells Fargo was a pioneer there:

https://www.investmentnews.com/industry ... unds-69099The first ETF was from State Street although iShares is often credited with popularising them around the turn of the century, when it was part of Barclays.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 1:09 pm

by GeoffF100

International wrote:GeoffF100 wrote:If tidying up is costly, you meed to question whether it is worth it. Tidy portfolios are not necessarily any more profitable than untidy ones.

Yes, I agree that. The context is here:

viewtopic.php?t=42245 . I'm looking to reposition myself to be retired (or FI at least) and this whole platform/OEIC/ETF decision is driven by my realisation that I am haemorrhaging platform fees which are dragging me by ~0.2% in my ISA and arguably ~0.17% in my pension.

When we get to retirement withdrawal rates where I think about numbers like growth of 5% less inflation of 3%, leaving 2% then 0.2% drag seems a lot!

I appreciate your help with thinking through the potential switch costs.

I do not claim to have studied your portfolio in detail, but it is high risk, and an impolite critic might call it a pig's breakfast. Nonetheless, there will costs in changing it, and it is best to avoid hasty decisions. 0.2% drag is a real drag if you are only getting a real return of 2% (minus costs and taxes), which is about what Vanguard predicts for the next ten years. Nonetheless, if you do the accounting correctly, it will be difficult to do much better than that. Look before you leap.

You need to consider the big picture. You need financial projections for the various options. We do not have much good to say about financial advisers here, but that is the kind of thing they do.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 3:04 pm

by londoninvestor

EthicsGradient wrote:The L&G OEIC tracks the

FTSE USA index, not the S&P 500. It's similar (587 constituents), but not identical, so you expect variations, and not because of the OEIC v. ETF comparison.

Also, the L&G OEIC prices daily at 15:00, whereas the ETF prices are likely to be taken at the daily exchange close (16:30). So you wouldn't expect identical day-on-day returns even if they tracked the same underlying index: the same "day" on the chart refers to a slightly different 24-hour period for the OEIC than it does for the ETFs.

Re: Future of OEIC vs ETFs

Posted: March 16th, 2024, 3:13 pm

by londoninvestor

International wrote:that seems to show the OEIC (orange) falling relative to the ETFs from the start of the period.

Note though that all three of them have an almost identical return measured over the 5-day period.

The reason the orange line is at the bottom is that the ETFs have their best day (relative to the OEIC) on the first day of the period, and their worst day on the last day.

Re: Future of OEIC vs ETFs

Posted: March 17th, 2024, 8:55 am

by tjh290633

1nvest wrote:International wrote:Hello,

I'm with HL who charge percentage platform fees for "funds" but a flat fee for ETFs. I have been pondering either:

- Moving to iWeb and staying with "Funds", which are OEICs in my case.

- Staying with HL and moving to ETFs.

I have noticed that in the UK we seem to have a good choice of OEICs, which is not the case elsewhere.

I think I have got my head around the differences between the two from reading this forum and other resources. I think I prefer "funds"/OEICs to ETFs, but it is more a case of familiarity.

My question is this: given that ETFs are newer and more fashionable, do you think OEICs/funds will gradually die out in favour of ETFs?

Thanks for any thoughts.

Predominately ETF's are held via a broker, who takes your money and buys the shares (funds) you like ... in their name. Requires a linked bank account, where transfers can be blocked. Somewhat similar to depositing money into a bank savings account, where the money becomes the banks, and where they pay you (often relatively small amounts) of interest for that 'loan', and increasingly nowadays object/delay/block your loan being repaid.

Some funds such as FCIT have savings plan options (

https://www.columbiathreadneedle.co.uk/ ... ained/gia/ £40+VAT/year fee), where you send them a cheque and buy shares in the fund more directly with the fund managers. Sell shares and they'll post you a cheque for the proceeds. Direct bank transfers are also supported however a cheque is more flexible - even if there maybe a higher cost to cash a cheque if you don't have a account at the place that cashes the cheque for you. Largely cuts out the broker, market maker and bank risk factors.

I'm not fan of lending to others, such as banks (cash deposits/savings accounts) or the state (Gilts), especially when they get to set the terms and conditions (tax rates etc.). Nor come to that even Pounds, would rather hold/use US dollar bills. Gold combined with stocks can serve well, and if stocks are held directly with a fund, cheques based, you could be in a situation where you're carrying physical gold and cheque(s) around ... outside of the fiat/virtual banking system. Assuming a bad case situation cashing a cheque might incur a 5% of value cost, as might cashing in gold be at 5% below spot price. Better that than having "your" money locked by others, and more generally the costs are minimal, maybe even zero (or in the case of gold, you might buy a coin at 2% above spot, sell at 1% above spot to a retailer, or privately both buy and sell at 1% above spot).

For such diversity reasons, I opine that ETF's will not totally eliminate funds, nor will paper money totally eliminate gold/silver. They may (have) a smaller market share, but remain active/available. If anything there's a possible situation where ETF's have already peaked in market share/alternatives bottomed, where in percentage terms ETF's start losing a proportion of market share.

There is a lot of misinformation here. FCIT is not a fund, it is an Investment Trust. They used to have a savings scheme through F&C Asset Management, which they sold to Columbia Threadneedle indirectly. You have an account with CT, and if you buy shares in FCIT they are held in a nominee account on your behalf. This is the same with any other broker. Your name does not appear on the shareholders' register. If you want a regular savings scheme, this is done by a direct debit. If you sell shares you will get the proceeds by BACS transfer. That having been said, CT are also a fund manager, having bought the Threadneedle business, which in turn came from Eagle Star. This works independently of the business dealing with F&C IT shares.

TJH

Re: Future of OEIC vs ETFs

Posted: March 21st, 2024, 12:14 am

by Hariseldon58

ETFs often reduce the indicated costs by securities lending.

I hold both OEICs and ETFs, the differences are not sufficient to move from one to the other just for the sake of it.

Re: Future of OEIC vs ETFs

Posted: March 21st, 2024, 8:10 am

by International

FT have published an article on this topic.

The mutual fund at 100: is it becoming obsolete?

https://www.ft.com/content/6d4f870c-f39 ... e65484f35a