HYP06 is a 'HYP-othetical' high yield portfolio, chosen in early 2011 and backtested from Jan. 13, 2006.

It was conceived as a lump-sum investment to gauge how a purist iteration of Stephen Bland's (aka pyad's) system would have faced the crash of 2007-08. Dividends were hammered for several years while the portfolio was young. Could it overcome early setbacks?

The deviser's guidelines were followed, except that 20 shares were fictitiously bought in equal amounts, rather than his 15. By 2011 most practitioners seemed to be seeking safety in numbers. All shares were in the FTSE 100 index and were the highest current yielders subject to fundamental filtering: chiefly, five years of rising dividends and not too much debt. Only one company could hail from each sector-- HYP's vital safety feature. No deviation or repetition allowed.

The result was full of perennially high-paying blue chips such as Tesco, Unilever, BATS and Vodafone. The demo was not meant to give brilliant results but characteristic ones: it plugged a chronological hole between Pyad's HYP1 of Nov. 2000 and the real-money Footsie HYP which I acquired in Jul. 2011.

HYP06 was to be subjected to 'light, judicious tinkering', such as selling a share if it stopped paying dividends but not if it cut them. There would be no trimming to correct biases which might evolve in supplying income. Later I would forgive what might transpire to be temporary lapses of payouts, e.g. Tesco.

The pretend portfolio, accounted to Dec. 31, has been front-tested almost twice as long as it was jobbed backward. Its progress was reported annually on The Motley Fool until 2016. An update for the ensuing four years follows:

MEMBERSHIP (deletions italicised)

BAe Systems (BA.)

BHP (BHP)- bought 2012

BOC International (BOC)- bid 2006

BAT Industries (BAT)

Centrica (CNA)

Compass (CPG)

Diageo (DGE)- bought 2008

DSG International (DSGI)- sold 2008 (dividend passed)

GKN (GKN)- sold 2009 (dividend passed)

GlaxoSmithKline (GSK)

IMI (IMI)- bought 2009

International Power (IPR)- bought 2006, bid 2012

Kelda (KEL)- bid 2006

Land Securities (LAND)

Legal & General (LGEN)

National Grid (NG.)

Next (NXT)- bought 2010

Pearson (PSON)

Persimmon (PSN)- sold 2008 (dividend passed)

Rexam (REX)- sold 2009 (dividend passed)

Royal Dutch Shell B (RDSB)

Scottish & Newcastle (SCTN)- bid 2008

Severn Trent (SVT)- bought 2008

South32 (S32)- BHP spinoff 2015

Standard Chartered (STAN)

Tesco (TSCO)

Unilever (ULVR)

Vodafone (VOD)

INCOME

2006 (from Jan. 13): £2,939

2007: £3,149 +7.1%

2008: £3,239 +2.9%

2009: £2,990 -2.7%

2010: £3,235 +8.2%

2011: £3,646 +12.7%

2012: £4,127 +13.2%

2013: £4,239 +2.7%

2014: £5,608 +32.3%

2015: £4,907 -12.5%

2016: £4,708 -4.1%

2017: £5.866 +24.6%

2018: £4.960 -15.4%

2019: £5,075 +2.3%

TOTAL TO DATE: £58,688

The same sum as Pyad used for HYP1, £75,000 gross, would have produced £5,075 in 2019, assuming £23 instant-withdrawal-account interest (at a beggarly 0.5%) on capital receipts from past corporate actions yet to be recycled.

Dividends totalled £5,052, a small rise from 2018, when they had shrunk by a worst-yet 15.4%. That was partly down to special payouts vanishing, especially from Next-- with only £3 from South32, the BHP spinoff, to swell the harvest in 2019. However regular payouts rose by 4.2%: twice the 2.1% increase for the Retail Prices Index in the year to Nov. 2019, assumed to be the same in the calendar year.

HYP06's cumulative income, 2006-19, is £58,688 (including £671 from uncommitted cash) or almost four-fifths what was invested: an average 5.6% pa yield. In 2019 the return on the capital's brought-forward market value was 4.2%, compared with an average 4.0% over HYP06's lifespan and 3.6% in 2018. Revenue compounded at 4.3% pa nominal, 1.3% real.

Year 14's income was worth one-fifth more than Year One's after deflation by the RPI. Income rose nominally in nine of 14 years. The biggest dip was the aforesaid 15.4% of 2018, followed by 12.5% in 2015.

CORPORATE ACTIONS

The newest capital changes are BHP's special distribution a year ago and National Grid's in Jun. 2017. Admin has been light. No bids since International Power seven years back, hence little sleep deprivation for the legendary Doris.

Pyad thought what he called market trading-- letting it sift and reorder portfolios-- would likely give better results than gratuitous fiddling. I agree.

A rule imposed by myself- to provide for uptake of rights issues and placings without injecting more capital- was that no brand-new share could be acquired until the Unallocated stash amounted to 150% of unit cost. For HYP06 the trigger was £5,625: one-twentieth of £75,000 plus 50%. Given my lifelong disdain for cash calls, I now think this stipulation is too stringent and have scrapped it for my real HYPs, preferring to redeploy windfalls pronto.

In HYP06 idle capital is £5,024, enough to finance a 21st constituent... perhaps WPP?

BALANCE

That holdings' value or income may diverge vexes many HYPers. Not me. My yardstick is that a stake worth more than twice average weight (5%, one-twentieth) is obese and one worth 2.5% is anorexic, but I lose no sleep if they wax or wane.

At year end the most valuable holding was Compass at 19.2% of HYP06's value, followed by Next (9.3%). Thus two positions cover more than a quarter of realisable value. Both, as we gave seen, are doughty payers and I will not touch them. Apart from South32, the five least valuable holdings-- all defined above as underweight-- are Centrica (1.3%), Vodafone (also 1.3%, but after capital reductions), Land Securities and Standard Chartered (1.6% apiece), and Tesco (2.1%). Their combined capital contribution is under 8%, a lot less than either of the two porkers.

Centrica and Vodafone do not look like upping dividends in the short term. Indeed Centrica's may go west. But since none of the five anorexics is a lost cause over ten or 20 years, they will be left to cure themselves or be plucked by predators.

Income is potentially less skewed since Compass and Next reverted to regular payouts only. In 2018 BAT was the biggest payer with 11.4% of the haul; this year it was top again with 11.8%, but in Year One Vodafone chipped in 16.4% and during the last decade Next was supplying almost one-quarter. The average annual top payout in 2006-19 was 12.1% of the total. I detect no sign of a constant deterioration which would bring dangerous over-dependence on an unvarying handful of members.

During the financial crisis which HYP06 was notionally pitted against, DSG International (Dixons), GKN and Rexam suspended dividends and were dumped. Alas, so was Persimmon. Had it been reprieved it would have titivated results with its Capital Return Plan, as with HYP1; inertia would have born fruit. More recently Tesco was the sole company to drop the divi, but it quickly returned to the list. I grow lazier and more indulgent.

DERISKING

One way to defend purchasing power is to fix a withdrawal rate and increase the sum spent only by inflation each year, regardless of how much faster receipts increase. The surplus goes into an income reserve against future cuts and suspensions. Once the reserve is full enough-- say one year of current spendable income-- a higher index-linked withdrawal rate can be contemplated.

For HYP06 the initial withdrawal was set at 3.55%+RPI, steered by an All-Share Index yield of 2.9% at the launch in Jan. 2006 and the portfolio's actual historic yield of 3.9% at end-2006 from the first 11.5 months' receipts. The withdrawal rate stuck for seven years; but by end-2013 ten months of spendable income reposed in the kitty and specials were flowing in. It appeared feasible to raise the rate to 4.26%+RPI, a 20% hike.

Receipts continued so buoyant that the enhanced rate did not prevent the income reserve rising from 9 to 16 months between Years 8 and 10. Another uplift was justifiable, by 15%, giving 4.90%+RPI. That has lowered the reserve to 14 months, which feels a plump enough cushion; nonetheless the dim immediate vista for divis militates against further rises. I could live with almost 5% plus cost-of-living protection for some time (1).

PROSPECTS

The outlook is squally: income growth is stumbling, at best slow. Partly that is my bad. Two replacements, Standard Chartered and BHP, proved inept despite their internationally diversificatory appeal.

Tesco had a great fall. There has been chopping at Pearson and Vodafone and a dollar-terms freeze lasting several years at Shell, though Pearson has begun restoration and the oil giant offers to do more for owners.

BATS, Compass and IMI braked dividend growth. National Grid promises little more than matching inflation. Glaxo is on a prolonged freeze. Land Securities is restoring its payout pianissimo while retail-exposed REITs are under scrutiny. Next overcame sales resistance more nimbly than most, shining this Christmas; it vaguely hints at restoring specials, though cash could go to those accursed buybacks.

The only constituents to lift payouts at 5% pa or more since 2015 are BATs, Compass, Land Securities, Legal & General and Unilever. The deceleration cracked open the income reserve for the first time, modestly, in 2018 and 2019: a total of £420 has been abstracted from an end-2017 balance of £6,788. There is 14 months' worth of index-linked payout in the kitty. It ought to suffice.

CAPITAL

2006 (Jan. 13): £75,000 before 1% purchase costs

2006: (Dec. 31) £86,941 +15.9%

2007: £89,948 +3.5%

2008: £71,587 -20.4%

2009: £76,848 +7.3%

2010: £90,581 +17.9%

2011: £95,192 +5.1%

2012: £105,428 +10.8%

2013: £126,767 +20.2%

2014: £126,439 -0.3%

2015: £119,199 -5.7%

2016: £130,544 +9.5%

2017: £137,178 +5.1%

2018: £121,984 -11.1%

2019: £141,312 +15.8%

High Yield Portfolios are where capital does not matter, but market values tell something about their horsepower as income generators. A selection whose dividend stream widely outpaces its realisable value may be running into trouble, chomping its capital covertly.

HYP06 has hit a new record year-end value: it would have been worth £141,312 at Dec. 31, a 15.8% rise after an 11.1% decline in 2018. Its previous peak value was £126,767, six years ago. The portfolio is now nominally worth 88% more than at its putative launch; in real terms, 38% more, not a mark of capital incineration. The most serious erosion between year ends was 20.4% in 2008, crisis time. Amid all the bumps HYP06's compound annual growth is 4.6% pa versus inflation of 3.0%.

For relativists, the portfolio beat the FTSE 100 index in nine of 14 years and by 1.3 percentage points last year, after trailing it in 2015-18 when big-divi blue chips were way out of vogue. HYP06's sole bad undershoot of the Footsie was in 2009, during the 'dash for trash' which benched HY shares; although it put on 7.3%, recovery plays fared far better. The latter-day spell of relative weakness was against momentum and growth picks. Now it is whispered that Value may arise from its coma, with Boris as resuscitator.

Four holdings were devalued last year: Centrica, Pearson, Shell and Vodafone. All were in my erstwhile Sturdy Seventeen, compiled in 2010. Centrica, Land Securities, Tesco and Vodafone are worth less than when bought in 2006. Sturdiness is becoming a memory, sooner than I guessed a decade ago.

---------------------------------------------------------------------------------------------------------------------

(1) Derisking produces current withdrawal rates of 6.0%+RPI for pyad's HYP1 after 19 years; 4.3% for the 'Basket of Seven' and 3.6% for the 'Basket of Eight' after the same span as HYP06. As in other comparative tests, derisked HYP income emerged materially greater than from collections of investment trusts, even after wider dividend variability from a HYP's narrower selection of equities. That is the method's best argument.

Got a credit card? use our Credit Card & Finance Calculators

Thanks to Rhyd6,eyeball08,Wondergirly,bofh,johnstevens77, for Donating to support the site

A HYP-othetical portfolio: Year 14 review

Forum rules

Tight HYP discussions only please - OT please discuss in strategies

Tight HYP discussions only please - OT please discuss in strategies

-

Luniversal

- 2 Lemon pips

- Posts: 157

- Joined: November 4th, 2016, 11:01 am

- Has thanked: 14 times

- Been thanked: 1163 times

-

MDW1954

- Lemon Quarter

- Posts: 2365

- Joined: November 4th, 2016, 8:46 pm

- Has thanked: 527 times

- Been thanked: 1013 times

Re: A HYP-othetical portfolio: Year 14 review

Thanks, Luni. Interesting. I remember you setting it up.

In retrospect, your Damascene laxity re: dividends came a little too late in the case of Persimmon. That might have altered the outcome considerably!

MDW1954

In retrospect, your Damascene laxity re: dividends came a little too late in the case of Persimmon. That might have altered the outcome considerably!

MDW1954

-

monabri

- Lemon Half

- Posts: 8426

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: A HYP-othetical portfolio: Year 14 review

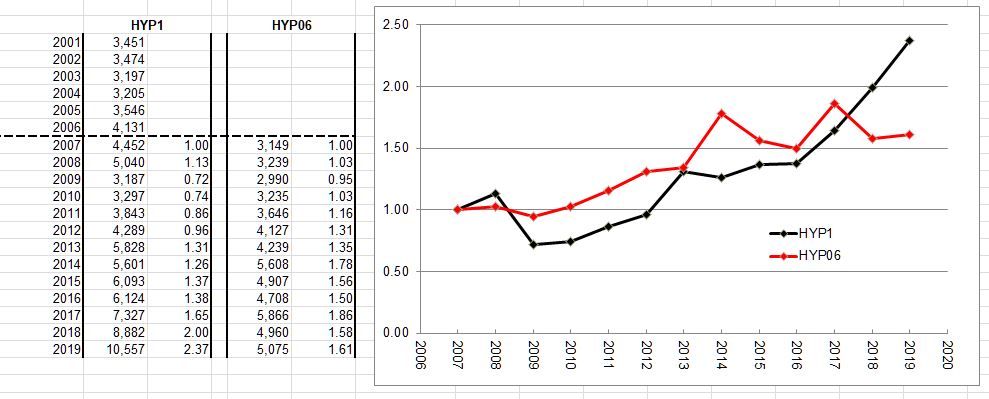

I thought I'd compare the income stream from HYP06 to HYP1 - with 2007 as a baseline. I've normalised the income and calculated the increase in income relative to the baseline.

For a good deal of the time, HYP06 was ahead of HYP1 but in the last couple of years, HYP1 has got it's nose out in front.

(I wanted to do the same exercise for B7/8 baskets, for comparison, but I couldn't find the yearly incomes....especially important in those dark years when income dropped in HYPxx).

When one looks at the individual selections, I was expecting to see many of HYP1's choices in HYP6. Did you (L'Uni) deliberately try to select a bunch of shares that did not feature in HYP1?

p.s. WPP divi has been held - is it a good candidate ?

For a good deal of the time, HYP06 was ahead of HYP1 but in the last couple of years, HYP1 has got it's nose out in front.

(I wanted to do the same exercise for B7/8 baskets, for comparison, but I couldn't find the yearly incomes....especially important in those dark years when income dropped in HYPxx).

When one looks at the individual selections, I was expecting to see many of HYP1's choices in HYP6. Did you (L'Uni) deliberately try to select a bunch of shares that did not feature in HYP1?

p.s. WPP divi has been held - is it a good candidate ?

-

monabri

- Lemon Half

- Posts: 8426

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: A HYP-othetical portfolio: Year 14 review

MDW1954 wrote:Thanks, Luni. Interesting. I remember you setting it up.

In retrospect, your Damascene laxity re: dividends came a little too late in the case of Persimmon. That might have altered the outcome considerably!

MDW1954

That thought crossed my mind too but it is only 1 in 20....although is is a significant "payer" in the last couple of years.

-

daveh

- Lemon Quarter

- Posts: 2204

- Joined: November 4th, 2016, 11:06 am

- Has thanked: 413 times

- Been thanked: 809 times

Re: A HYP-othetical portfolio: Year 14 review

monabri wrote:MDW1954 wrote:Thanks, Luni. Interesting. I remember you setting it up.

In retrospect, your Damascene laxity re: dividends came a little too late in the case of Persimmon. That might have altered the outcome considerably!

MDW1954

That thought crossed my mind too but it is only 1 in 20....although is is a significant "payer" in the last couple of years.

A significant payer and a significant capital gainer. I purchased in 2008 at 646p per share. Todays price is 2724 and I've received 1.5x the purchase cost in dividends for a overall gain of 474%. I didn't sell when they cut the dividend as I thought they would come back eventually. There was a point near the bottom when I thought of buying more*, but as they werne't paying a dividend I didn't.

* My reasoning was that the price was massively down, they were making money and had paid down debt so weren't going bust. We still needed more housing into the future so there was a market for their product.

-

MDW1954

- Lemon Quarter

- Posts: 2365

- Joined: November 4th, 2016, 8:46 pm

- Has thanked: 527 times

- Been thanked: 1013 times

Re: A HYP-othetical portfolio: Year 14 review

daveh wrote:monabri wrote:MDW1954 wrote:Thanks, Luni. Interesting. I remember you setting it up.

In retrospect, your Damascene laxity re: dividends came a little too late in the case of Persimmon. That might have altered the outcome considerably!

MDW1954

That thought crossed my mind too but it is only 1 in 20....although is is a significant "payer" in the last couple of years.

A significant payer and a significant capital gainer.

Exactly! It's pretty much the star performer of HYP1.

MDW1954

-

Luniversal

- 2 Lemon pips

- Posts: 157

- Joined: November 4th, 2016, 11:01 am

- Has thanked: 14 times

- Been thanked: 1163 times

Re: A HYP-othetical portfolio: Year 14 review

monabri wrote:For a good deal of the time, HYP06 was ahead of HYP1 but in the last couple of years, HYP1 has got its nose out in front.

(I wanted to do the same exercise for B7/8 baskets, for comparison, but I couldn't find the yearly incomes....especially important in those dark years when income dropped in HYPxx).

When one looks at the individual selections, I was expecting to see many of HYP1's choices in HYP06. Did you (L'Uni) deliberately try to select a bunch of shares that did not feature in HYP1?

(1) I keep expecting HYP1's income to come a purler, but year after year it pulls a rabbit out of the hat: Rio Tinto getting through the mining cycle with less damage than other big diggers, Persimmon accelerating its distribution programme, BATS coming on (until recently) like a corporate ATM.

But above all we must grasp what a flying start HYP1 had. Nov. 2000 was a golden moment for nailing down income streams from blue chips spurned during the stampede into TFT stocks. The equivalent today would be to buy 15 on an average historic yield of >=8.5% when the Footsie yielded 4.3%. That fatness of initial return can cover many a mishap down the road, but the choice is not like 19 years ago. Neither, perhaps, is the level of dividend security.

(2) I hope shortly to post a comparison between the two income-oriented baskets, their 'Universe of 24' pool of income ITs, the Growth Ten, the Conviction Five and HYP06-- all from HYP06's starting date in Jan. 2006.

(3) HYP06's shares were picked purely on merit, after an exhaustive review of the Footsie which tried to ignore hindsight about what would happen between 2006 and 2011. (Hence four shares soon to pass their dividends were included.) A lot had changed in the five years since HYP1 was drawn: the criteria were the same, the environment very different. For one thing, the dotcom crash had done its worst.

Flash forward five years to Jul. 2011. My LuniHYP100 contained only eight of the 20 shares in HYP06. The global crisis had intervened.

-

Gengulphus

- Lemon Quarter

- Posts: 4255

- Joined: November 4th, 2016, 1:17 am

- Been thanked: 2628 times

Re: A HYP-othetical portfolio: Year 14 review

I've only come across this post long after it was posted, due to my absence from TLF between November 27th last year and May 20th.

There was clearly at least one other difference from pyad's guidelines when he devised HYP1, since they said very clearly "Just to recap: my suggestion is that you simply buy and hold forever, ignoring press comment on your shares, resisting the temptation to meddle once the initial decision has been taken. There may be occasions when something has to be done, for example if a share is taken over for cash which has to be reinvested, but in general leaving the portfolio completely alone is probably the best policy for a large number of income investors." Your report indicates very clearly that HYP06 has sold a share for not paying dividends on four occasions, for DSGI International, GKN, Persimmon and Rexam - this is something HYP1 has never done, despite having a number of occasions on which it could have done so. I strongly suspect that has turned out to be to HYP06's disadvantage, since what it's lost by no longer being invested in Persimmon seems likely to have outweighed any conceivable advantage obtained by selling the other three. But I'm not expressing an opinion on whether it's a good policy in general: it doesn't look to have been so far, but just four occasions on which the policy has applied is far too small a sample size to base every a moderately firm conclusion on. So I'm just noting that how HYP06 has been run differs from the guidelines used for HYP1 in at least one other way besides choosing 20 shares rather than 15.

More importantly, since HYP06 was chosen in early 2011, its constituents were chosen at a time when what they did from 13 January 2006 to early 2011 was already known. It would be easy for that knowledge to influence which shares were chosen, either consciously or unconsciously, and although I have little doubt that Luniversal did a good job of avoiding letting it influence his choices consciously, that leaves the possibility of unconscious influence open. All he can have done to try to avoid that is to think of as many ways for the choice to be influenced by the knowledge of what had already happened to the shares chosen as possible, do his best to avoid them, and hope that any ways that he had missed and any inadequacies in his methods of avoiding the ways he had thought of weren't big enough to bias the results significantly.

Or more briefly, one has to suspect that HYP06's performance from 13 January 2006 to the date it was chosen in early 2011 was influenced by hindsight bias, and it was impossible for Luniversal to come up with a way to construct HYP06 that eliminates that suspicion. Even if he had chosen to construct it entirely mechanically on the basis of only data that had been available on 13 January 2006, hindsight bias could still creep in, because he would have had to choose the method and mechanical criteria used to select the shares to invest in, and that choice could have been influenced (again quite possibly unconsciously) by knowledge of what methods had performed relatively well between then and early 2011.

Suspicion isn't proof, of course, but it is grounds for further investigations. An obvious investigation is to look how HYP06 has performed in the 'backtesting' period from 13 January 2006 to early 2011 against how it has performed subsequently. I don't have the data required for that, but I do have the data from Luniversal's post for similar periods, namely a comparison between its performance in the years 2006-2010 (both ends inclusive) and its performance in 2011 and subsequent years. So start with its income and capital performances in 2006-2010, which I'll compare with HYP1's performances for the similar period 13 November 2005 to 13 November 2010, normalised to make its capital value also start at £75 (since HYP1's year 5 report says that its capital value was £98,367 on 13/11/2005, this multiplies all of HYP1's figures by £75,000/£98,367 = about 0.762451):

(*) Sources for the unnormalised figures on which this column is based are 2005, 2006, 2007, 2008, 2009, 2010. Note that at least AFAIAA, pyad never produced a report on HYP1 in 2008, and although the link I've given for its 2008 value describes itself as reporting on HYP1, it was in fact kool4kats reporting on CHYP1 - it's just that at the time, it appeared to be the only version of HYP1 still in existence and so didn't appear to need a different name to pyad's version. There were some differences from pyad's version due to the takeovers of Scottish & Newcastle, Resolution and Alliance & Leicester in 2008: pyad had (unknown to us at the time) replaced them with Pearson, Persimmon and some top-ups, while we replaced them with GlaxoSmithKline, Aviva and Vodafone. The earliest of those replacements had only had any effect on the portfolios for around six months - a short enough period that I think CHYP1's 2008 capital value is a reasonable guide to HYP1's, but there is undoubtedly some difference. I've therefore preceded the 2008 HYP1 capital value with "~" and made it grey in the table, and done the same for figures derived from it.

Overall, HYP06 comes out pretty well in this comparison: it delivered slightly more income overall, and probably more importantly, the annual income was much less volatile (ranging from 2,939 to £3,239 over the five years, compared with £2,430 to £3,843 for HYP1) and rose overall by over 10% instead of falling overall by over 20%. And on capital, it did modestly better as well.

So what about the years that HYP06 has actually been existence, i.e. 2011 to 2019? (And about half of 2020 so far, of course, but I only have the data from this thread's OP, so all I can say is that I expect 2020 to be interesting for both HYP1 and HYP06!) Here are the similar income and capital value tables for both HYP06 and HYP1, both normalised to an initial capital value of £75k near the start of 2011:

(*) Sources for the unnormalised figures on which this column is based are 2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017, 2018, 2019. I should note that I had trouble with the 2013 link, due apparently to the Wayback Machine having problems with a cookie. This was on Firefox, and trying it on Internet Explorer instead didn't run into the same problem, so obviously it's browser dependent... Also, if need be, the data is obtainable even in Firefox by viewing the page source, albeit with some difficulty locating it among all the enclosing HTML...

So in the years that it has actually existed, HYP06 has done somewhat worse than HYP1 on total income. Its annual income has jumped forwards and backwards quite a bit (5 increases and 3 falls, 2 of them double-digit percentage falls), whereas HYP1's has been a smoother increase (7 increases and one small fall). There has also been a strong overall tendency for HYP06's income to rise less than HYP1's, as reflected in their overall increases by 39.2% and 174.7%, though HYP1's income started from a lower base, and the jumping backwards and forwards of HYP06's income has meant that it hasn't been anything like a smooth and steady progression! On capital, HYP06 was doing appreciably better than HYP1 at the end of 2019 and has been ahead or only very slightly behind every year, but its lead of 11.3% at the end of 2019 isn't all that convincing given that it had a similar lead at the end of 2013 which vanished within the following two years.

All in all, I reckon there are two quite striking differences between how HYP06 performed relative to HYP1 in the 'backtesting' years 2006-2010 and the 'really existed' years 2011-2019: it achieved a markedly better overall dividend increase in 2006-2010 and a markedly worse overall dividend increase in 2011-2019, and it had a noticeably smoother dividend progression in 2006-2010 and a noticeably rougher dividend progression in 2011-2019. On the overall level of income, it did better in 2006-2010 and worse in 2011-2019, but the differences are quite small and I think within the range of normal statistical variations; on capital, it's done better in both periods, but again I think the differences are within the range of normal statistical variations.

Overall, therefore, I'm afraid I suspect rather more strongly than at the start of this exercise that HYP06's selection in early 2011 was affected by hindsight bias, specifically by selecting shares on the basis of knowledge about their dividend safety and growth prospects that wasn't available in 2006. That's still not proof, of course, just increased suspicions... As observed above, this year is going to be interesting, as it's going to be the first major crisis that hits both portfolios while they're both actually in existence.

Gengulphus

Luniversal wrote:HYP06 is a 'HYP-othetical' high yield portfolio, chosen in early 2011 and backtested from Jan. 13, 2006.

It was conceived as a lump-sum investment to gauge how a purist iteration of Stephen Bland's (aka pyad's) system would have faced the crash of 2007-08. Dividends were hammered for several years while the portfolio was young. Could it overcome early setbacks?

The deviser's guidelines were followed, except that 20 shares were fictitiously bought in equal amounts, rather than his 15. ...

There was clearly at least one other difference from pyad's guidelines when he devised HYP1, since they said very clearly "Just to recap: my suggestion is that you simply buy and hold forever, ignoring press comment on your shares, resisting the temptation to meddle once the initial decision has been taken. There may be occasions when something has to be done, for example if a share is taken over for cash which has to be reinvested, but in general leaving the portfolio completely alone is probably the best policy for a large number of income investors." Your report indicates very clearly that HYP06 has sold a share for not paying dividends on four occasions, for DSGI International, GKN, Persimmon and Rexam - this is something HYP1 has never done, despite having a number of occasions on which it could have done so. I strongly suspect that has turned out to be to HYP06's disadvantage, since what it's lost by no longer being invested in Persimmon seems likely to have outweighed any conceivable advantage obtained by selling the other three. But I'm not expressing an opinion on whether it's a good policy in general: it doesn't look to have been so far, but just four occasions on which the policy has applied is far too small a sample size to base every a moderately firm conclusion on. So I'm just noting that how HYP06 has been run differs from the guidelines used for HYP1 in at least one other way besides choosing 20 shares rather than 15.

More importantly, since HYP06 was chosen in early 2011, its constituents were chosen at a time when what they did from 13 January 2006 to early 2011 was already known. It would be easy for that knowledge to influence which shares were chosen, either consciously or unconsciously, and although I have little doubt that Luniversal did a good job of avoiding letting it influence his choices consciously, that leaves the possibility of unconscious influence open. All he can have done to try to avoid that is to think of as many ways for the choice to be influenced by the knowledge of what had already happened to the shares chosen as possible, do his best to avoid them, and hope that any ways that he had missed and any inadequacies in his methods of avoiding the ways he had thought of weren't big enough to bias the results significantly.

Or more briefly, one has to suspect that HYP06's performance from 13 January 2006 to the date it was chosen in early 2011 was influenced by hindsight bias, and it was impossible for Luniversal to come up with a way to construct HYP06 that eliminates that suspicion. Even if he had chosen to construct it entirely mechanically on the basis of only data that had been available on 13 January 2006, hindsight bias could still creep in, because he would have had to choose the method and mechanical criteria used to select the shares to invest in, and that choice could have been influenced (again quite possibly unconsciously) by knowledge of what methods had performed relatively well between then and early 2011.

Suspicion isn't proof, of course, but it is grounds for further investigations. An obvious investigation is to look how HYP06 has performed in the 'backtesting' period from 13 January 2006 to early 2011 against how it has performed subsequently. I don't have the data required for that, but I do have the data from Luniversal's post for similar periods, namely a comparison between its performance in the years 2006-2010 (both ends inclusive) and its performance in 2011 and subsequent years. So start with its income and capital performances in 2006-2010, which I'll compare with HYP1's performances for the similar period 13 November 2005 to 13 November 2010, normalised to make its capital value also start at £75 (since HYP1's year 5 report says that its capital value was £98,367 on 13/11/2005, this multiplies all of HYP1's figures by £75,000/£98,367 = about 0.762451):

(*) Sources for the unnormalised figures on which this column is based are 2005, 2006, 2007, 2008, 2009, 2010. Note that at least AFAIAA, pyad never produced a report on HYP1 in 2008, and although the link I've given for its 2008 value describes itself as reporting on HYP1, it was in fact kool4kats reporting on CHYP1 - it's just that at the time, it appeared to be the only version of HYP1 still in existence and so didn't appear to need a different name to pyad's version. There were some differences from pyad's version due to the takeovers of Scottish & Newcastle, Resolution and Alliance & Leicester in 2008: pyad had (unknown to us at the time) replaced them with Pearson, Persimmon and some top-ups, while we replaced them with GlaxoSmithKline, Aviva and Vodafone. The earliest of those replacements had only had any effect on the portfolios for around six months - a short enough period that I think CHYP1's 2008 capital value is a reasonable guide to HYP1's, but there is undoubtedly some difference. I've therefore preceded the 2008 HYP1 capital value with "~" and made it grey in the table, and done the same for figures derived from it.

Overall, HYP06 comes out pretty well in this comparison: it delivered slightly more income overall, and probably more importantly, the annual income was much less volatile (ranging from 2,939 to £3,239 over the five years, compared with £2,430 to £3,843 for HYP1) and rose overall by over 10% instead of falling overall by over 20%. And on capital, it did modestly better as well.

So what about the years that HYP06 has actually been existence, i.e. 2011 to 2019? (And about half of 2020 so far, of course, but I only have the data from this thread's OP, so all I can say is that I expect 2020 to be interesting for both HYP1 and HYP06!) Here are the similar income and capital value tables for both HYP06 and HYP1, both normalised to an initial capital value of £75k near the start of 2011:

(*) Sources for the unnormalised figures on which this column is based are 2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017, 2018, 2019. I should note that I had trouble with the 2013 link, due apparently to the Wayback Machine having problems with a cookie. This was on Firefox, and trying it on Internet Explorer instead didn't run into the same problem, so obviously it's browser dependent... Also, if need be, the data is obtainable even in Firefox by viewing the page source, albeit with some difficulty locating it among all the enclosing HTML...

So in the years that it has actually existed, HYP06 has done somewhat worse than HYP1 on total income. Its annual income has jumped forwards and backwards quite a bit (5 increases and 3 falls, 2 of them double-digit percentage falls), whereas HYP1's has been a smoother increase (7 increases and one small fall). There has also been a strong overall tendency for HYP06's income to rise less than HYP1's, as reflected in their overall increases by 39.2% and 174.7%, though HYP1's income started from a lower base, and the jumping backwards and forwards of HYP06's income has meant that it hasn't been anything like a smooth and steady progression! On capital, HYP06 was doing appreciably better than HYP1 at the end of 2019 and has been ahead or only very slightly behind every year, but its lead of 11.3% at the end of 2019 isn't all that convincing given that it had a similar lead at the end of 2013 which vanished within the following two years.

All in all, I reckon there are two quite striking differences between how HYP06 performed relative to HYP1 in the 'backtesting' years 2006-2010 and the 'really existed' years 2011-2019: it achieved a markedly better overall dividend increase in 2006-2010 and a markedly worse overall dividend increase in 2011-2019, and it had a noticeably smoother dividend progression in 2006-2010 and a noticeably rougher dividend progression in 2011-2019. On the overall level of income, it did better in 2006-2010 and worse in 2011-2019, but the differences are quite small and I think within the range of normal statistical variations; on capital, it's done better in both periods, but again I think the differences are within the range of normal statistical variations.

Overall, therefore, I'm afraid I suspect rather more strongly than at the start of this exercise that HYP06's selection in early 2011 was affected by hindsight bias, specifically by selecting shares on the basis of knowledge about their dividend safety and growth prospects that wasn't available in 2006. That's still not proof, of course, just increased suspicions... As observed above, this year is going to be interesting, as it's going to be the first major crisis that hits both portfolios while they're both actually in existence.

Gengulphus

-

1nvest

- Lemon Quarter

- Posts: 4446

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 696 times

- Been thanked: 1360 times

Re: A HYP-othetical portfolio: Year 14 review

Gengulphus wrote:There was clearly at least one other difference from pyad's guidelines when he devised HYP1, since they said very clearly "Just to recap: my suggestion is that you simply buy and hold forever, ignoring press comment on your shares, resisting the temptation to meddle once the initial decision has been taken.

Whilst the rewards can compare for meddle/not, the concentration risk can rise to be substantial. Contrived (hindsight/survived) example but for a initial equal weight buy and hold compared to yearly rebalancing back to equal weightings ...

If the rewards tend to be similar, but where equal weighted yearly rebalanced reduces single stock exposure risk back to equal levels, is it not sounder to meddle? Even if its not regular yearly rebalancing back to equal weightings, but perhaps just reducing a holding once its weighting had become 'uncomfortably high'.

-

tjh290633

- Lemon Half

- Posts: 8286

- Joined: November 4th, 2016, 11:20 am

- Has thanked: 919 times

- Been thanked: 4137 times

Re: A HYP-othetical portfolio: Year 14 review

1nvest wrote:If the rewards tend to be similar, but where equal weighted yearly rebalanced reduces single stock exposure risk back to equal levels, is it not sounder to meddle? Even if its not regular yearly rebalancing back to equal weightings, but perhaps just reducing a holding once its weighting had become 'uncomfortably high'.

Of course it is sounder to meddle. I decided to do this back in 1997, when LLoyds-TSB had risen to about 16% of my portfolio, and Zeneca was about 12%, which worried me. On the basis that I was running my own unit fund, I decided that what was sauce for the professionals should also be sauce for me, and I set a limit of 10% on any one holding. As the portfolio grew in number of holdings, I reduced the limit, first to twice the median holding value and then to 1.5 times the median holding value. The number of occasions when I have to act on a heavyweight holding are relatively few, although 2019-20 called for 8 such actions as the markets became volatile. In 2018-19 there was only one and in 2017-18 there were two.

TJH

-

Gengulphus

- Lemon Quarter

- Posts: 4255

- Joined: November 4th, 2016, 1:17 am

- Been thanked: 2628 times

Re: A HYP-othetical portfolio: Year 14 review

1nvest wrote:If the rewards tend to be similar, but where equal weighted yearly rebalanced reduces single stock exposure risk back to equal levels, is it not sounder to meddle? Even if its not regular yearly rebalancing back to equal weightings, but perhaps just reducing a holding once its weighting had become 'uncomfortably high'.

Just to be clear, as I said, "I'm not expressing an opinion on whether [meddling is] a good policy in general" and "I'm just noting that how HYP06 has been run differs from the guidelines used for HYP1 in at least one other way besides choosing 20 shares rather than 15". Basically, the sample sizes are far too small, and there are too many other differences between HYP1 and HYP06 that might influence the comparison. This is just one comparison of a non-meddling HYP and a meddling HYP, and other differences include the different amounts of diversification, being managed by different people using different selection criteria and the different ways in which the two portfolios have handled cash: HYP1 has generally paid normal dividends out immediately as income and reinvested corporate action proceeds immediately; HYP06 has the 'derisking' cash management policy Dod101 describes in the OP. (I should perhaps clarify that I only mentioned the meddling vs non-meddling difference in my last post because that's the only one I've spotted on which HYP06 clearly goes explicitly against what was said about HYP1 when it was selected, rather than only against how HYP1 turned out to be run in practice.)

The reason why I didn't express an opinion on whether meddling is a good policy in general is simply that I haven't formed such an opinion. I'm certain that meddling can be used to reduce the variability of HYP returns - but that means both reducing the 'you might get lucky' returns and increasing the 'you might get unlucky' returns (*). What it does to statistically expected returns, I don't know, even after watching reports on HYPs on this board and its TMF predecessor for getting on for 20 years now. I've seen some hints that it probably decreases them, but not by all that much - in particular, not by enough to be likely to be statistically significant, even if I had been systematically gathering data from people's HYP reports rather than just watching them. I do know that it wouldn't be at all surprising theoretically if meddling reduces variability but also reduces returns a bit - higher risk and higher returns are theoretically linked, provided the risks are intelligently taken. But then again, I don't have all that much faith in the theory concerned, and indeed regard some of it as quite clearly wrong...

That's not IMHO a subject to go into any deeper than that on this board, given that its focus is practical, not theoretical. At the purely practical level, it's enough for me to have decided that even if meddling costs me something on investment returns, that cost looks very likely to be low enough that I'm happy to pay it to get the lower variability of returns. If it doesn't cost me anything on returns, so much the better! But that decision is certainly based on my preferences and financial circumstances: other HYPers' mileages may differ, and so it's not an opinion about meddling in general, just about it as it applies to me.

(*) Though note that meddling can only reduce the imbalances between companies and between sectors, effectively increasing the diversification of the HYP and so reducing its vulnerability to company-specific and sector-specific events. It can't reduce vulnerability to economy-wide events, and so (as I'd imagine just about all HYPers are experiencing at present) the "you might get unlucky" returns can still drop quite a long way. E.g. my past experience in the 2008-2009 financial crisis was that my HYP income dropped by about a third between the 2008/2009 and 2009/2010 tax years: that was partly my own fault, as in the lead-up to it, I'd let my HYP build up to around 35% financial companies by being a bit too willing to buy 'irresistable bargains'. With hindsight, if I'd been more careful to diversify well, my HYP income would still have dropped by around a quarter - which would have been better, but still a very significant drop. For what it's worth, I'm expecting the drop between the 2019/2020 and 2020/2021 tax years to be considerably worse... (I should perhaps add that these drops are essentially between dividend income totals in records I've kept for Income Tax return purposes, with just a little bit of extra analysis added to distinguish between dividends received from my HYP shares and my non-HYP shares. In particular, they're for totals of dividends paid in the tax year rather than of dividends that have been declared or gone ex-dividend in the tax year - which means that the onset of COVID-19 related cuts and cancellations is almost perfectly synchronised to the tax-year boundary, and so their impact doesn't (or hardly) get softened by partially affecting one change between tax years and partially another.)

Gengulphus

Return to “HYP Practical (See Group Guidelines)”

Who is online

Users browsing this forum: No registered users and 53 guests