A HYP-othetical portfolio: Year 14 review

Posted: January 6th, 2020, 11:43 pm

HYP06 is a 'HYP-othetical' high yield portfolio, chosen in early 2011 and backtested from Jan. 13, 2006.

It was conceived as a lump-sum investment to gauge how a purist iteration of Stephen Bland's (aka pyad's) system would have faced the crash of 2007-08. Dividends were hammered for several years while the portfolio was young. Could it overcome early setbacks?

The deviser's guidelines were followed, except that 20 shares were fictitiously bought in equal amounts, rather than his 15. By 2011 most practitioners seemed to be seeking safety in numbers. All shares were in the FTSE 100 index and were the highest current yielders subject to fundamental filtering: chiefly, five years of rising dividends and not too much debt. Only one company could hail from each sector-- HYP's vital safety feature. No deviation or repetition allowed.

The result was full of perennially high-paying blue chips such as Tesco, Unilever, BATS and Vodafone. The demo was not meant to give brilliant results but characteristic ones: it plugged a chronological hole between Pyad's HYP1 of Nov. 2000 and the real-money Footsie HYP which I acquired in Jul. 2011.

HYP06 was to be subjected to 'light, judicious tinkering', such as selling a share if it stopped paying dividends but not if it cut them. There would be no trimming to correct biases which might evolve in supplying income. Later I would forgive what might transpire to be temporary lapses of payouts, e.g. Tesco.

The pretend portfolio, accounted to Dec. 31, has been front-tested almost twice as long as it was jobbed backward. Its progress was reported annually on The Motley Fool until 2016. An update for the ensuing four years follows:

MEMBERSHIP (deletions italicised)

BAe Systems (BA.)

BHP (BHP)- bought 2012

BOC International (BOC)- bid 2006

BAT Industries (BAT)

Centrica (CNA)

Compass (CPG)

Diageo (DGE)- bought 2008

DSG International (DSGI)- sold 2008 (dividend passed)

GKN (GKN)- sold 2009 (dividend passed)

GlaxoSmithKline (GSK)

IMI (IMI)- bought 2009

International Power (IPR)- bought 2006, bid 2012

Kelda (KEL)- bid 2006

Land Securities (LAND)

Legal & General (LGEN)

National Grid (NG.)

Next (NXT)- bought 2010

Pearson (PSON)

Persimmon (PSN)- sold 2008 (dividend passed)

Rexam (REX)- sold 2009 (dividend passed)

Royal Dutch Shell B (RDSB)

Scottish & Newcastle (SCTN)- bid 2008

Severn Trent (SVT)- bought 2008

South32 (S32)- BHP spinoff 2015

Standard Chartered (STAN)

Tesco (TSCO)

Unilever (ULVR)

Vodafone (VOD)

INCOME

2006 (from Jan. 13): £2,939

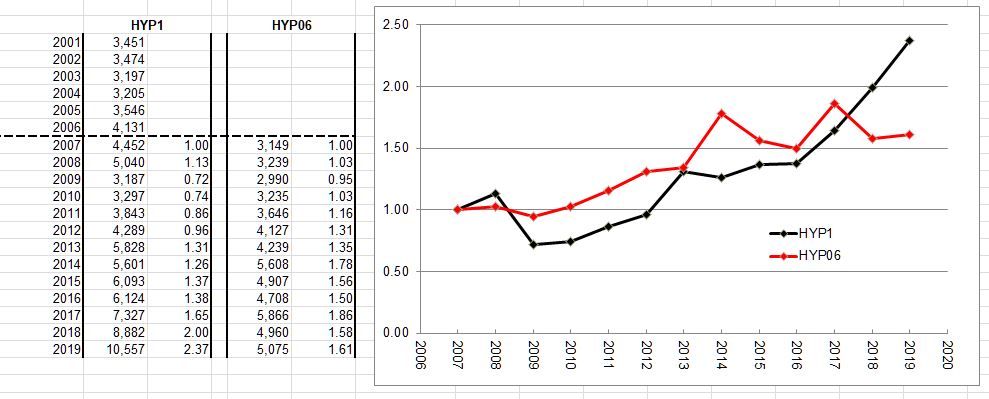

2007: £3,149 +7.1%

2008: £3,239 +2.9%

2009: £2,990 -2.7%

2010: £3,235 +8.2%

2011: £3,646 +12.7%

2012: £4,127 +13.2%

2013: £4,239 +2.7%

2014: £5,608 +32.3%

2015: £4,907 -12.5%

2016: £4,708 -4.1%

2017: £5.866 +24.6%

2018: £4.960 -15.4%

2019: £5,075 +2.3%

TOTAL TO DATE: £58,688

The same sum as Pyad used for HYP1, £75,000 gross, would have produced £5,075 in 2019, assuming £23 instant-withdrawal-account interest (at a beggarly 0.5%) on capital receipts from past corporate actions yet to be recycled.

Dividends totalled £5,052, a small rise from 2018, when they had shrunk by a worst-yet 15.4%. That was partly down to special payouts vanishing, especially from Next-- with only £3 from South32, the BHP spinoff, to swell the harvest in 2019. However regular payouts rose by 4.2%: twice the 2.1% increase for the Retail Prices Index in the year to Nov. 2019, assumed to be the same in the calendar year.

HYP06's cumulative income, 2006-19, is £58,688 (including £671 from uncommitted cash) or almost four-fifths what was invested: an average 5.6% pa yield. In 2019 the return on the capital's brought-forward market value was 4.2%, compared with an average 4.0% over HYP06's lifespan and 3.6% in 2018. Revenue compounded at 4.3% pa nominal, 1.3% real.

Year 14's income was worth one-fifth more than Year One's after deflation by the RPI. Income rose nominally in nine of 14 years. The biggest dip was the aforesaid 15.4% of 2018, followed by 12.5% in 2015.

CORPORATE ACTIONS

The newest capital changes are BHP's special distribution a year ago and National Grid's in Jun. 2017. Admin has been light. No bids since International Power seven years back, hence little sleep deprivation for the legendary Doris.

Pyad thought what he called market trading-- letting it sift and reorder portfolios-- would likely give better results than gratuitous fiddling. I agree.

A rule imposed by myself- to provide for uptake of rights issues and placings without injecting more capital- was that no brand-new share could be acquired until the Unallocated stash amounted to 150% of unit cost. For HYP06 the trigger was £5,625: one-twentieth of £75,000 plus 50%. Given my lifelong disdain for cash calls, I now think this stipulation is too stringent and have scrapped it for my real HYPs, preferring to redeploy windfalls pronto.

In HYP06 idle capital is £5,024, enough to finance a 21st constituent... perhaps WPP?

BALANCE

That holdings' value or income may diverge vexes many HYPers. Not me. My yardstick is that a stake worth more than twice average weight (5%, one-twentieth) is obese and one worth 2.5% is anorexic, but I lose no sleep if they wax or wane.

At year end the most valuable holding was Compass at 19.2% of HYP06's value, followed by Next (9.3%). Thus two positions cover more than a quarter of realisable value. Both, as we gave seen, are doughty payers and I will not touch them. Apart from South32, the five least valuable holdings-- all defined above as underweight-- are Centrica (1.3%), Vodafone (also 1.3%, but after capital reductions), Land Securities and Standard Chartered (1.6% apiece), and Tesco (2.1%). Their combined capital contribution is under 8%, a lot less than either of the two porkers.

Centrica and Vodafone do not look like upping dividends in the short term. Indeed Centrica's may go west. But since none of the five anorexics is a lost cause over ten or 20 years, they will be left to cure themselves or be plucked by predators.

Income is potentially less skewed since Compass and Next reverted to regular payouts only. In 2018 BAT was the biggest payer with 11.4% of the haul; this year it was top again with 11.8%, but in Year One Vodafone chipped in 16.4% and during the last decade Next was supplying almost one-quarter. The average annual top payout in 2006-19 was 12.1% of the total. I detect no sign of a constant deterioration which would bring dangerous over-dependence on an unvarying handful of members.

During the financial crisis which HYP06 was notionally pitted against, DSG International (Dixons), GKN and Rexam suspended dividends and were dumped. Alas, so was Persimmon. Had it been reprieved it would have titivated results with its Capital Return Plan, as with HYP1; inertia would have born fruit. More recently Tesco was the sole company to drop the divi, but it quickly returned to the list. I grow lazier and more indulgent.

DERISKING

One way to defend purchasing power is to fix a withdrawal rate and increase the sum spent only by inflation each year, regardless of how much faster receipts increase. The surplus goes into an income reserve against future cuts and suspensions. Once the reserve is full enough-- say one year of current spendable income-- a higher index-linked withdrawal rate can be contemplated.

For HYP06 the initial withdrawal was set at 3.55%+RPI, steered by an All-Share Index yield of 2.9% at the launch in Jan. 2006 and the portfolio's actual historic yield of 3.9% at end-2006 from the first 11.5 months' receipts. The withdrawal rate stuck for seven years; but by end-2013 ten months of spendable income reposed in the kitty and specials were flowing in. It appeared feasible to raise the rate to 4.26%+RPI, a 20% hike.

Receipts continued so buoyant that the enhanced rate did not prevent the income reserve rising from 9 to 16 months between Years 8 and 10. Another uplift was justifiable, by 15%, giving 4.90%+RPI. That has lowered the reserve to 14 months, which feels a plump enough cushion; nonetheless the dim immediate vista for divis militates against further rises. I could live with almost 5% plus cost-of-living protection for some time (1).

PROSPECTS

The outlook is squally: income growth is stumbling, at best slow. Partly that is my bad. Two replacements, Standard Chartered and BHP, proved inept despite their internationally diversificatory appeal.

Tesco had a great fall. There has been chopping at Pearson and Vodafone and a dollar-terms freeze lasting several years at Shell, though Pearson has begun restoration and the oil giant offers to do more for owners.

BATS, Compass and IMI braked dividend growth. National Grid promises little more than matching inflation. Glaxo is on a prolonged freeze. Land Securities is restoring its payout pianissimo while retail-exposed REITs are under scrutiny. Next overcame sales resistance more nimbly than most, shining this Christmas; it vaguely hints at restoring specials, though cash could go to those accursed buybacks.

The only constituents to lift payouts at 5% pa or more since 2015 are BATs, Compass, Land Securities, Legal & General and Unilever. The deceleration cracked open the income reserve for the first time, modestly, in 2018 and 2019: a total of £420 has been abstracted from an end-2017 balance of £6,788. There is 14 months' worth of index-linked payout in the kitty. It ought to suffice.

CAPITAL

2006 (Jan. 13): £75,000 before 1% purchase costs

2006: (Dec. 31) £86,941 +15.9%

2007: £89,948 +3.5%

2008: £71,587 -20.4%

2009: £76,848 +7.3%

2010: £90,581 +17.9%

2011: £95,192 +5.1%

2012: £105,428 +10.8%

2013: £126,767 +20.2%

2014: £126,439 -0.3%

2015: £119,199 -5.7%

2016: £130,544 +9.5%

2017: £137,178 +5.1%

2018: £121,984 -11.1%

2019: £141,312 +15.8%

High Yield Portfolios are where capital does not matter, but market values tell something about their horsepower as income generators. A selection whose dividend stream widely outpaces its realisable value may be running into trouble, chomping its capital covertly.

HYP06 has hit a new record year-end value: it would have been worth £141,312 at Dec. 31, a 15.8% rise after an 11.1% decline in 2018. Its previous peak value was £126,767, six years ago. The portfolio is now nominally worth 88% more than at its putative launch; in real terms, 38% more, not a mark of capital incineration. The most serious erosion between year ends was 20.4% in 2008, crisis time. Amid all the bumps HYP06's compound annual growth is 4.6% pa versus inflation of 3.0%.

For relativists, the portfolio beat the FTSE 100 index in nine of 14 years and by 1.3 percentage points last year, after trailing it in 2015-18 when big-divi blue chips were way out of vogue. HYP06's sole bad undershoot of the Footsie was in 2009, during the 'dash for trash' which benched HY shares; although it put on 7.3%, recovery plays fared far better. The latter-day spell of relative weakness was against momentum and growth picks. Now it is whispered that Value may arise from its coma, with Boris as resuscitator.

Four holdings were devalued last year: Centrica, Pearson, Shell and Vodafone. All were in my erstwhile Sturdy Seventeen, compiled in 2010. Centrica, Land Securities, Tesco and Vodafone are worth less than when bought in 2006. Sturdiness is becoming a memory, sooner than I guessed a decade ago.

---------------------------------------------------------------------------------------------------------------------

(1) Derisking produces current withdrawal rates of 6.0%+RPI for pyad's HYP1 after 19 years; 4.3% for the 'Basket of Seven' and 3.6% for the 'Basket of Eight' after the same span as HYP06. As in other comparative tests, derisked HYP income emerged materially greater than from collections of investment trusts, even after wider dividend variability from a HYP's narrower selection of equities. That is the method's best argument.

It was conceived as a lump-sum investment to gauge how a purist iteration of Stephen Bland's (aka pyad's) system would have faced the crash of 2007-08. Dividends were hammered for several years while the portfolio was young. Could it overcome early setbacks?

The deviser's guidelines were followed, except that 20 shares were fictitiously bought in equal amounts, rather than his 15. By 2011 most practitioners seemed to be seeking safety in numbers. All shares were in the FTSE 100 index and were the highest current yielders subject to fundamental filtering: chiefly, five years of rising dividends and not too much debt. Only one company could hail from each sector-- HYP's vital safety feature. No deviation or repetition allowed.

The result was full of perennially high-paying blue chips such as Tesco, Unilever, BATS and Vodafone. The demo was not meant to give brilliant results but characteristic ones: it plugged a chronological hole between Pyad's HYP1 of Nov. 2000 and the real-money Footsie HYP which I acquired in Jul. 2011.

HYP06 was to be subjected to 'light, judicious tinkering', such as selling a share if it stopped paying dividends but not if it cut them. There would be no trimming to correct biases which might evolve in supplying income. Later I would forgive what might transpire to be temporary lapses of payouts, e.g. Tesco.

The pretend portfolio, accounted to Dec. 31, has been front-tested almost twice as long as it was jobbed backward. Its progress was reported annually on The Motley Fool until 2016. An update for the ensuing four years follows:

MEMBERSHIP (deletions italicised)

BAe Systems (BA.)

BHP (BHP)- bought 2012

BOC International (BOC)- bid 2006

BAT Industries (BAT)

Centrica (CNA)

Compass (CPG)

Diageo (DGE)- bought 2008

DSG International (DSGI)- sold 2008 (dividend passed)

GKN (GKN)- sold 2009 (dividend passed)

GlaxoSmithKline (GSK)

IMI (IMI)- bought 2009

International Power (IPR)- bought 2006, bid 2012

Kelda (KEL)- bid 2006

Land Securities (LAND)

Legal & General (LGEN)

National Grid (NG.)

Next (NXT)- bought 2010

Pearson (PSON)

Persimmon (PSN)- sold 2008 (dividend passed)

Rexam (REX)- sold 2009 (dividend passed)

Royal Dutch Shell B (RDSB)

Scottish & Newcastle (SCTN)- bid 2008

Severn Trent (SVT)- bought 2008

South32 (S32)- BHP spinoff 2015

Standard Chartered (STAN)

Tesco (TSCO)

Unilever (ULVR)

Vodafone (VOD)

INCOME

2006 (from Jan. 13): £2,939

2007: £3,149 +7.1%

2008: £3,239 +2.9%

2009: £2,990 -2.7%

2010: £3,235 +8.2%

2011: £3,646 +12.7%

2012: £4,127 +13.2%

2013: £4,239 +2.7%

2014: £5,608 +32.3%

2015: £4,907 -12.5%

2016: £4,708 -4.1%

2017: £5.866 +24.6%

2018: £4.960 -15.4%

2019: £5,075 +2.3%

TOTAL TO DATE: £58,688

The same sum as Pyad used for HYP1, £75,000 gross, would have produced £5,075 in 2019, assuming £23 instant-withdrawal-account interest (at a beggarly 0.5%) on capital receipts from past corporate actions yet to be recycled.

Dividends totalled £5,052, a small rise from 2018, when they had shrunk by a worst-yet 15.4%. That was partly down to special payouts vanishing, especially from Next-- with only £3 from South32, the BHP spinoff, to swell the harvest in 2019. However regular payouts rose by 4.2%: twice the 2.1% increase for the Retail Prices Index in the year to Nov. 2019, assumed to be the same in the calendar year.

HYP06's cumulative income, 2006-19, is £58,688 (including £671 from uncommitted cash) or almost four-fifths what was invested: an average 5.6% pa yield. In 2019 the return on the capital's brought-forward market value was 4.2%, compared with an average 4.0% over HYP06's lifespan and 3.6% in 2018. Revenue compounded at 4.3% pa nominal, 1.3% real.

Year 14's income was worth one-fifth more than Year One's after deflation by the RPI. Income rose nominally in nine of 14 years. The biggest dip was the aforesaid 15.4% of 2018, followed by 12.5% in 2015.

CORPORATE ACTIONS

The newest capital changes are BHP's special distribution a year ago and National Grid's in Jun. 2017. Admin has been light. No bids since International Power seven years back, hence little sleep deprivation for the legendary Doris.

Pyad thought what he called market trading-- letting it sift and reorder portfolios-- would likely give better results than gratuitous fiddling. I agree.

A rule imposed by myself- to provide for uptake of rights issues and placings without injecting more capital- was that no brand-new share could be acquired until the Unallocated stash amounted to 150% of unit cost. For HYP06 the trigger was £5,625: one-twentieth of £75,000 plus 50%. Given my lifelong disdain for cash calls, I now think this stipulation is too stringent and have scrapped it for my real HYPs, preferring to redeploy windfalls pronto.

In HYP06 idle capital is £5,024, enough to finance a 21st constituent... perhaps WPP?

BALANCE

That holdings' value or income may diverge vexes many HYPers. Not me. My yardstick is that a stake worth more than twice average weight (5%, one-twentieth) is obese and one worth 2.5% is anorexic, but I lose no sleep if they wax or wane.

At year end the most valuable holding was Compass at 19.2% of HYP06's value, followed by Next (9.3%). Thus two positions cover more than a quarter of realisable value. Both, as we gave seen, are doughty payers and I will not touch them. Apart from South32, the five least valuable holdings-- all defined above as underweight-- are Centrica (1.3%), Vodafone (also 1.3%, but after capital reductions), Land Securities and Standard Chartered (1.6% apiece), and Tesco (2.1%). Their combined capital contribution is under 8%, a lot less than either of the two porkers.

Centrica and Vodafone do not look like upping dividends in the short term. Indeed Centrica's may go west. But since none of the five anorexics is a lost cause over ten or 20 years, they will be left to cure themselves or be plucked by predators.

Income is potentially less skewed since Compass and Next reverted to regular payouts only. In 2018 BAT was the biggest payer with 11.4% of the haul; this year it was top again with 11.8%, but in Year One Vodafone chipped in 16.4% and during the last decade Next was supplying almost one-quarter. The average annual top payout in 2006-19 was 12.1% of the total. I detect no sign of a constant deterioration which would bring dangerous over-dependence on an unvarying handful of members.

During the financial crisis which HYP06 was notionally pitted against, DSG International (Dixons), GKN and Rexam suspended dividends and were dumped. Alas, so was Persimmon. Had it been reprieved it would have titivated results with its Capital Return Plan, as with HYP1; inertia would have born fruit. More recently Tesco was the sole company to drop the divi, but it quickly returned to the list. I grow lazier and more indulgent.

DERISKING

One way to defend purchasing power is to fix a withdrawal rate and increase the sum spent only by inflation each year, regardless of how much faster receipts increase. The surplus goes into an income reserve against future cuts and suspensions. Once the reserve is full enough-- say one year of current spendable income-- a higher index-linked withdrawal rate can be contemplated.

For HYP06 the initial withdrawal was set at 3.55%+RPI, steered by an All-Share Index yield of 2.9% at the launch in Jan. 2006 and the portfolio's actual historic yield of 3.9% at end-2006 from the first 11.5 months' receipts. The withdrawal rate stuck for seven years; but by end-2013 ten months of spendable income reposed in the kitty and specials were flowing in. It appeared feasible to raise the rate to 4.26%+RPI, a 20% hike.

Receipts continued so buoyant that the enhanced rate did not prevent the income reserve rising from 9 to 16 months between Years 8 and 10. Another uplift was justifiable, by 15%, giving 4.90%+RPI. That has lowered the reserve to 14 months, which feels a plump enough cushion; nonetheless the dim immediate vista for divis militates against further rises. I could live with almost 5% plus cost-of-living protection for some time (1).

PROSPECTS

The outlook is squally: income growth is stumbling, at best slow. Partly that is my bad. Two replacements, Standard Chartered and BHP, proved inept despite their internationally diversificatory appeal.

Tesco had a great fall. There has been chopping at Pearson and Vodafone and a dollar-terms freeze lasting several years at Shell, though Pearson has begun restoration and the oil giant offers to do more for owners.

BATS, Compass and IMI braked dividend growth. National Grid promises little more than matching inflation. Glaxo is on a prolonged freeze. Land Securities is restoring its payout pianissimo while retail-exposed REITs are under scrutiny. Next overcame sales resistance more nimbly than most, shining this Christmas; it vaguely hints at restoring specials, though cash could go to those accursed buybacks.

The only constituents to lift payouts at 5% pa or more since 2015 are BATs, Compass, Land Securities, Legal & General and Unilever. The deceleration cracked open the income reserve for the first time, modestly, in 2018 and 2019: a total of £420 has been abstracted from an end-2017 balance of £6,788. There is 14 months' worth of index-linked payout in the kitty. It ought to suffice.

CAPITAL

2006 (Jan. 13): £75,000 before 1% purchase costs

2006: (Dec. 31) £86,941 +15.9%

2007: £89,948 +3.5%

2008: £71,587 -20.4%

2009: £76,848 +7.3%

2010: £90,581 +17.9%

2011: £95,192 +5.1%

2012: £105,428 +10.8%

2013: £126,767 +20.2%

2014: £126,439 -0.3%

2015: £119,199 -5.7%

2016: £130,544 +9.5%

2017: £137,178 +5.1%

2018: £121,984 -11.1%

2019: £141,312 +15.8%

High Yield Portfolios are where capital does not matter, but market values tell something about their horsepower as income generators. A selection whose dividend stream widely outpaces its realisable value may be running into trouble, chomping its capital covertly.

HYP06 has hit a new record year-end value: it would have been worth £141,312 at Dec. 31, a 15.8% rise after an 11.1% decline in 2018. Its previous peak value was £126,767, six years ago. The portfolio is now nominally worth 88% more than at its putative launch; in real terms, 38% more, not a mark of capital incineration. The most serious erosion between year ends was 20.4% in 2008, crisis time. Amid all the bumps HYP06's compound annual growth is 4.6% pa versus inflation of 3.0%.

For relativists, the portfolio beat the FTSE 100 index in nine of 14 years and by 1.3 percentage points last year, after trailing it in 2015-18 when big-divi blue chips were way out of vogue. HYP06's sole bad undershoot of the Footsie was in 2009, during the 'dash for trash' which benched HY shares; although it put on 7.3%, recovery plays fared far better. The latter-day spell of relative weakness was against momentum and growth picks. Now it is whispered that Value may arise from its coma, with Boris as resuscitator.

Four holdings were devalued last year: Centrica, Pearson, Shell and Vodafone. All were in my erstwhile Sturdy Seventeen, compiled in 2010. Centrica, Land Securities, Tesco and Vodafone are worth less than when bought in 2006. Sturdiness is becoming a memory, sooner than I guessed a decade ago.

---------------------------------------------------------------------------------------------------------------------

(1) Derisking produces current withdrawal rates of 6.0%+RPI for pyad's HYP1 after 19 years; 4.3% for the 'Basket of Seven' and 3.6% for the 'Basket of Eight' after the same span as HYP06. As in other comparative tests, derisked HYP income emerged materially greater than from collections of investment trusts, even after wider dividend variability from a HYP's narrower selection of equities. That is the method's best argument.