StayinAlive wrote:mc2fool

If the answer is 35 or more then additional pre-2016 years won't help.

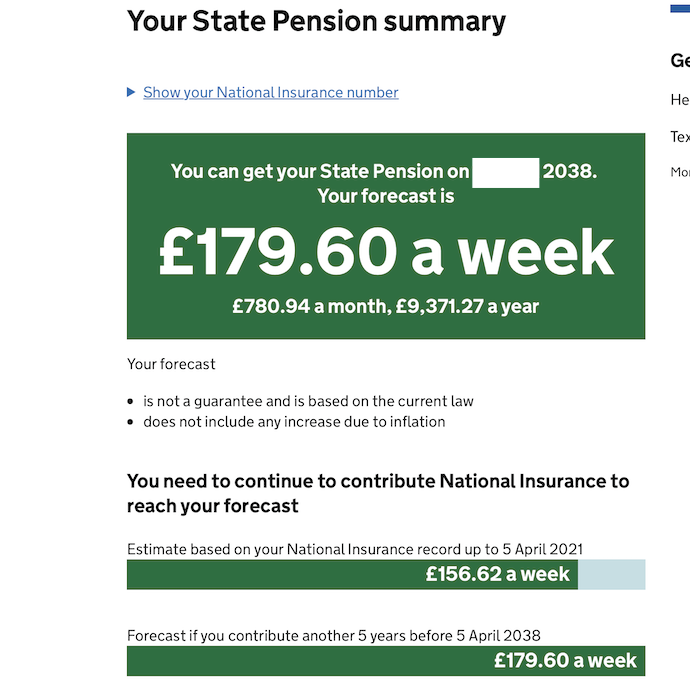

That's the bit that I did not realise - she has 37 pre-2016 years.

So, why does HMRC say the shortfall can be made up by voluntary contributions?

Yeah, that's been complained about for many yonks, and it's not just the pre-2016 thing. Even before the new state pension transition it would show the same for missing years even if you already had more than the 30 years (then) needed to get the full old state pension. The fact of having a gap and being able to pay to fill it is just unconnected with whether it'd be worth it to do so!

I'm still puzzled by the cost of £649.85, and even more puzzled by "

This shortfall may increase after 5 April 2023", 'cos, as I say, pre-2016 NICs are charged at the current rate (£824.20) and after 5 April 2023 the ability to pay pre-2016

terminates, it being a special provision for the transition to the new state pension. Normally (and after 5 April 2023) you can only pay the last 6 years. See

https://www.gov.uk/voluntary-national-insurance-contributions/ratesIn any case, it's irrelevant for your partner as she already has more than 35 pre-2016 years and so adding any more won't help. That applies to filling her 2014-15 partial year too.

So, she's left with the choice of paying class 3 NICs for any of the past 6 years and this one, or paying class 2 for last year and this year.

The cost of class 3 NICs is frozen at that of their year for two years and thereafter goes up to that of the current year, so the cheapest way with those is to pay 2020/21 (£15.30*52=£795.60) and 2021/22 (£15.40*52=£800.80). Pre 2020 and for this year, 2022/23, they're £15.85*52=£824.20.

https://www.gov.uk/government/publications/rates-and-allowances-national-insurance-contributions/rates-and-allowances-national-insurance-contributionsClass 2 rates, as already mentioned, are considerably cheaper, and while it's possible to also go back many years (albeit the cost is only frozen for one), the problem is that if she retrospectively declares herself as self-employed HMRC will ask her to refile her self assessment for those years, and may fine her for late filing (even if no additional tax was due).

So, as she only needs two years and has last year (which is still within the filing deadline) and this year to "earn" them, she can just register as self employed starting 6-Apr-2021 (and find a couple of relatives she can retrospectively do a "job" for!).

Start here:

https://www.gov.uk/register-for-self-assessment/self-employed (the only notable faff is that if she doesn't already she will have to file self assessments).