It amuses me to read some of those posts where posters write as if in tablets of stone handed down from on high. Life is not like that. At my age and having retired in my very early 50s I think I am entitled to draw my own conclusions. I had a feeling that it was 1nvest that quoted the early 1900s as a time of disaster

Dod

Got a credit card? use our Credit Card & Finance Calculators

Thanks to Wasron,jfgw,Rhyd6,eyeball08,Wondergirly, for Donating to support the site

Challenging the 4% Rule

-

Dod101

- The full Lemon

- Posts: 16629

- Joined: October 10th, 2017, 11:33 am

- Has thanked: 4343 times

- Been thanked: 7536 times

-

Steveam

- Lemon Slice

- Posts: 984

- Joined: March 18th, 2017, 10:22 pm

- Has thanked: 1797 times

- Been thanked: 538 times

Re: Challenging the 4% Rule

At age 90 I intend to start spending on wine, women and song … I might even throw in the odd Christmas cigar and switch on the central heating more than once a day.

Best wishes,

Steve

Best wishes,

Steve

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

Lootman wrote:1nvest wrote:For many they only want to work as long as necessary and have some years in retirement and the 4% SWR is a GUIDE, suggesting you need 25 times yearly retirement spending saved up in order to fund a average 30 year retirement period. The 4% SWR did however include some cases that fell short, around a 95% chance of success IIRC. So in some cases maybe your money only lasted 25 years, but for 65 year old retirees the odds are against you getting even to age 90.

As I understand it the 4% guideline assumes a normal retirement age, so age 66 as at present. If you retire younger that percentage should be lower. But conversely as you get older you can withdraw a higher percentage each year.

At age 90 you can probably safely withdraw 10% a year and not worry too much. Whether you would have anything to spend it on other than nursing care is another matter

Recent experiences of going around care homes has had a great incentive upon me to carry on drinking and smoking. Both retire and die earlier. On that basis my SWR guide figure is still much the same as the 'average'.

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

Dod101 wrote:It amuses me to read some of those posts where posters write as if in tablets of stone handed down from on high. Life is not like that. At my age and having retired in my very early 50s I think I am entitled to draw my own conclusions. I had a feeling that it was 1nvest that quoted the early 1900s as a time of disaster

Dod

In your case, as in most cases you were fortunate Dod. The primary risk is that of sequence of returns risk in the earlier retirement years. Get through those OK and likely your portfolio value will be up enough such that even if a big drop occurred its more a case of giving back other peoples money. The sort of position you're now well into. For others that retire just prior to large declines and a 4% SWR type amount, 25 years spending, could perhaps be halved, such from there you'd be looking at the equivalent of a 8% SWR. Even then often it works out, but is much more touch and go. A way to reduce that risk is to start with relatively little risk exposure (more bonds), and spend bonds so that you still in effect are averaging into stocks over time and see stock/bond ratio increasing on the stock side with time as you pass through/exit the 'danger zone'. How much stock/bond to start retirement with can be based on relative valuations at the time, however you might prefer to measure/value that. My own preferred measure for instance is suggesting a new retiree at the present time start with 55% bonds.

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

Lootman wrote:MrFoolish wrote:How would you factor in a defined benefit pension? Add the transfer value to your assets? Or subtract your yearly pension from your yearly expenditure? Presumably if you have not yet retired, the former method would be easier?

Same question about the state pension. Thanks.

If you believe in the 4% rule then the value of a pension is 25 times the amount it pays you annually.

On that basis my state pension will be worth just under a quarter of a million pounds, although that does not reflect the fairly generous triple lock feature.

In my case, around a 13K occupational pension (index linked), and a 7K (maybe 9K if I top up) state pension in 6 years time. Putting 6 x 7K/year aside as state pension in-fill that yields a present day and ongoing 20K/year inflation adjusted income from pensions. I don't value the capital value of that, see it just as a income stream. Desired yearly spending of around 30K, so 10K/year relative to a 4% SWR = 250K retirement pot (Bogle opted for 50/50 stock/bond for his retirement pot). Additional sums above that saw Bogle use a 80/20 stock/bond choice. I have a reasonable sized non-retirement pot, but nowhere near Bogles $80M net worth

-

Dod101

- The full Lemon

- Posts: 16629

- Joined: October 10th, 2017, 11:33 am

- Has thanked: 4343 times

- Been thanked: 7536 times

Re: Challenging the 4% Rule

1nvest wrote:Dod101 wrote:It amuses me to read some of those posts where posters write as if in tablets of stone handed down from on high. Life is not like that. At my age and having retired in my very early 50s I think I am entitled to draw my own conclusions. I had a feeling that it was 1nvest that quoted the early 1900s as a time of disaster

Dod

In your case, as in most cases you were fortunate Dod. The primary risk is that of sequence of returns risk in the earlier retirement years. Get through those OK and likely your portfolio value will be up enough such that even if a big drop occurred its more a case of giving back other peoples money. The sort of position you're now well into. For others that retire just prior to large declines and a 4% SWR type amount, 25 years spending, could perhaps be halved, such from there you'd be looking at the equivalent of a 8% SWR. Even then often it works out, but is much more touch and go. A way to reduce that risk is to start with relatively little risk exposure (more bonds), and spend bonds so that you still in effect are averaging into stocks over time and see stock/bond ratio increasing on the stock side with time as you pass through/exit the 'danger zone'. How much stock/bond to start retirement with can be based on relative valuations at the time, however you might prefer to measure/value that. My own preferred measure for instance is suggesting a new retiree at the present time start with 55% bonds.

Sequence of returns risk is a bigger one than the early 1900s scenario that you cite, at least I think so. I was fortunate that I was well into retirement before for instance the tech bubble burst in 2000. That was painful financially and gave me lessons that I have not nor will forget such as holding Cable and Wireless, and holding on ....and on....and on. I was sitting on a very substantial gain in mid 2000 with a total holding of around £30,000. It began to stumble and kept going down and I held on awaiting a recovery. I eventually bailed out at under £5,000. That was plain stupid on my part but I think any investor needs that sort of experience.

Had I retired in 1999, the tech bubble bursting the following year would have been a disaster.

Dod

-

Lootman

- The full Lemon

- Posts: 18938

- Joined: November 4th, 2016, 3:58 pm

- Has thanked: 636 times

- Been thanked: 6677 times

Re: Challenging the 4% Rule

Dod101 wrote:Had I retired in 1999, the tech bubble bursting the following year would have been a disaster.

Markets go up slowly and crash suddenly. One good thing about the fast declines is that they are over quickly. As I recall with both the dotcom crash and the financial crisis crash, a couple of years later and shares were off to the races again. The Covid crash was shorter - just a few months really.

So as long as you have a couple of years worth of living expenses in cash then you can avoid selling at firesale levels. And such down markets can be useful for taking tax losses or selling taxable holdings at a lower CGT liability.

I tend to see volatility as opportunity rather than a problem.

-

Dod101

- The full Lemon

- Posts: 16629

- Joined: October 10th, 2017, 11:33 am

- Has thanked: 4343 times

- Been thanked: 7536 times

Re: Challenging the 4% Rule

Lootman wrote:Dod101 wrote:Had I retired in 1999, the tech bubble bursting the following year would have been a disaster.

Markets go up slowly and crash suddenly. One good thing about the fast declines is that they are over quickly. As I recall with both the dotcom crash and the financial crisis crash, a couple of years later and shares were off to the races again. The Covid crash was shorter - just a few months really.

So as long as you have a couple of years worth of living expenses in cash then you can avoid selling at firesale levels. And such down markets can be useful for taking tax losses or selling taxable holdings at a lower CGT liability.

I tend to see volatility as opportunity rather than a problem.

I agree with all you say (at least in this post!) My problem with Cable and Wireless was that it did not recover. Recognising that risk and acting early would have saved me a lot of money (or in fact gained me a lot of money because most of what I nominally lost was actually a paper gain) Selling early and knowing when to is a great talent. Not sure that any of us have it except post the event!

Dod

-

Alaric

- Lemon Half

- Posts: 6068

- Joined: November 5th, 2016, 9:05 am

- Has thanked: 20 times

- Been thanked: 1419 times

Re: Challenging the 4% Rule

Lootman wrote:So as long as you have a couple of years worth of living expenses in cash then you can avoid selling at firesale levels. And such down markets can be useful for taking tax losses or selling taxable holdings at a lower CGT liability.

I tend to see volatility as opportunity rather than a problem.

If markets are falling and you have cash in hand, the "time to buy" is not today.

If retirement income is financed by a lump sum windfall or sale of something for cash, sequence of returns risk can in part be mitigated by holding cash and reinvesting slowly. I'm not sure we are ever going to see more reports, but a HYP proposed on Stockopedia and discussed on TLF may have demonstrated this given that the notional investment was taking place in March.April 2019. Anyone relying on that particular selection of investments for dividend income in 2020 would have been seriously disappointed, as indeed would someone putting a lump sum into a UK Tracker in 2019 with a view to taking the dividends as retirement income.

-

swill453

- Lemon Half

- Posts: 7989

- Joined: November 4th, 2016, 6:11 pm

- Has thanked: 989 times

- Been thanked: 3658 times

Re: Challenging the 4% Rule

Alaric wrote:If markets are falling and you have cash in hand, the "time to buy" is not today.

That's only true if you can time when they've stopped falling. This is usually only possible with hindsight.

Scott.

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

Alaric wrote:If retirement income is financed by a lump sum windfall or sale of something for cash, sequence of returns risk can in part be mitigated by holding cash and reinvesting slowly.

Consider that buy and hold is in effect the costless lumping in of a lump sum each and every day, and that implies that risk might be reduced by selling down at the point of transition from accumulation to retirement to reinvest that cash slowly.

On that basis a reasonable approach is to level down to sufficient stock/bond reflective of the relative valuation at that time. With some additional subsequent 'averaging-in' method to reinvest that cash. That averaging in could be as simple as 'spend bonds first'. A better approach IMO is the late (2001) Robert Lichello's AIM modified to not actually follow any sell trade signals (just updated Portfolio Control by half the indicated sell trade order size). AIM can also be used to identify a appropriate amount of %cash to transition to at the retirement point i.e. a ongoing paper AIM used as reference for how much %cash that AIM has at the time.

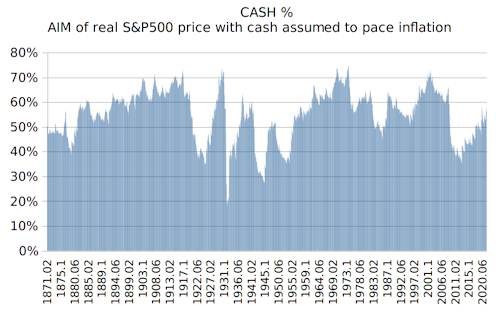

On that measure recent (end of October) indications were for 56% cash

How quickly or slowly that cash gets averaged in using AIM (with no actual sales) is subject to the the subsequent motion of market valuations, if a big dip does occur relatively quickly it might all be deployed relatively quickly, but have averaged down the average cost of stock. In other cases such as a sustained Bull run it can see cash taking a number of years to be deployed (buys/adds on pullbacks). Broadly/overall that tends to work relatively well, at least far better at reducing the downside risk, albeit at the sacrifice of some of good/great gains compared to having lumped all-in prior to a sustained Bull run.

When you reduce the risk of having lumped in at the worst possible time then the worst case SWR is also uplifted, as typically the worst case historic SWR arises out of a peak to trough period measure.

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

Dod101 wrote:Sequence of returns risk is a bigger one than the early 1900s scenario that you cite, at least I think so. I was fortunate that I was well into retirement before for instance the tech bubble burst in 2000. That was painful financially and gave me lessons that I have not nor will forget

.

.

Had I retired in 1999, the tech bubble bursting the following year would have been a disaster.

Not if you used something like the method I outlined in my prior post. For all of the common SWR worst cases, 1906, 1929, 1969, 2000 ... type start dates the paper AIM would have had you enter retirement with relatively high %cash, that in each of those cases saw that being deployed into subsequent lower share prices. End of 1999 and the paper AIM was indicating 64% cash. I suspect by March 2003 you'd have seen all of the cash deployed by AIM, so something like a comparison of this i.e. lower losses. And in losing less prior to transitioning to all-stock the subsequent gains might have been like this instead of lumped all-in at the 2000 high that saw this Overall differences to recent of having half the inflation adjusted start date amount compared to having twice the inflation adjusted start date amount (four times more - which to recent is like around a 6.5% higher CAGR).

-

TUK020

- Lemon Quarter

- Posts: 2045

- Joined: November 5th, 2016, 7:41 am

- Has thanked: 763 times

- Been thanked: 1179 times

Re: Challenging the 4% Rule

Steveam wrote:At age 90 I intend to start spending on wine, women and song … I might even throw in the odd Christmas cigar and switch on the central heating more than once a day.

Best wishes,

Steve

A pale imitation of the Snorvey Plan B, which involves cocaine and hookers (and probably ensures you don't have long enough to worry about sequence of returns risk)

-

kempiejon

- Lemon Quarter

- Posts: 3576

- Joined: November 5th, 2016, 10:30 am

- Has thanked: 1 time

- Been thanked: 1194 times

Re: Challenging the 4% Rule

TUK020 wrote:Steveam wrote:At age 90 I intend to start spending on wine, women and song … I might even throw in the odd Christmas cigar and switch on the central heating more than once a day.

Best wishes,

Steve

A pale imitation of the Snorvey Plan B, which involves cocaine and hookers (and probably ensures you don't have long enough to worry about sequence of returns risk)

Like Snorvey, should I get to 90 I'm gonna spend my capital on fast cars, fast women and expensive bourbon - the rest I'll just fritter away.

-

DrFfybes

- Lemon Quarter

- Posts: 3786

- Joined: November 6th, 2016, 10:25 pm

- Has thanked: 1193 times

- Been thanked: 1982 times

Re: Challenging the 4% Rule

kempiejon wrote:Like Snorvey, should I get to 90 I'm gonna spend my capital on fast cars, fast women and expensive bourbon - the rest I'll just fritter away.

I suspect by the time I reach 90 there will be no such thing as "fast cars".

Best look at that Mclaren now then

GeoffF100 wrote:Vanguard's "more flexible approach" is interesting:

https://www.vanguardinvestor.co.uk/arti ... retirement

Now those were interesting articles.

Ooooooh it is all too complicated. I think I might just buy an annuity

Paul

-

BT63

- Lemon Slice

- Posts: 432

- Joined: November 5th, 2016, 1:22 pm

- Has thanked: 59 times

- Been thanked: 121 times

Re: Challenging the 4% Rule

swill453 wrote:Alaric wrote:If markets are falling and you have cash in hand, the "time to buy" is not today.

That's only true if you can time when they've stopped falling. This is usually only possible with hindsight.

Scott.

Yes, bottoms are only possible with hindsight but it might be interesting to re-read something I said on another topic in spring 2020.

The topic was asking posters where they thought FTSE 100 would bottom as Covid escalated. I said 4200 and was wrong (the very lowest point was 4900; 17% higher), but to put it into context, below is all of what I said (link at the bottom; I also made comments later on the topic clarifying how much I was investing and at what levels I intended to increase buying or scale back buying):

April 2nd, 2020, 12:56 pm

I think.....

FTSE 100 will hit bottom around 4200.

Dow around 15000.

However, I also think FTSE is already undervalued therefore I am not going to wait/hope that I can go 'all-in' on the lowest low, so I am accumulating via index funds with multiple providers, set to buy on several fixed dates each month.

Savings and multiple cash ISAs, including my wife's, are being cashed out to fund this.

Once the savings are spent, if markets are still low I'll seriously consider taking on some borrowings to fund continuation of the heavy purchasing.

I appreciate that using my strategy won't get me the best value for money (probably an average price 15% higher than the very lowest price) but I won't be left behind if FTSE only reaches 4300 when my target was 4200.

viewtopic.php?f=88&t=22633&start=40

-

1nvest

- Lemon Quarter

- Posts: 4451

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 697 times

- Been thanked: 1369 times

Re: Challenging the 4% Rule

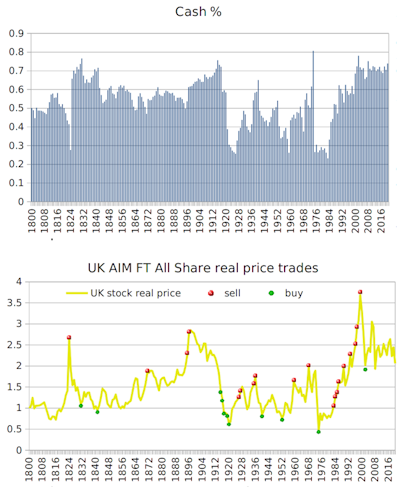

I mentioned Robert Lichello's AIM early and included a chart for US stock, comparing that to UK

suggests that the UK is relatively higher as of recent (AIM indicating a higher %cash to be appropriate). It also did a reasonable job of averaging in/out around the troughs/peaks

Considering that the Dow/Gold is around central 20 versus former 40 high, 1 low, that might suggest 50/50 stock/gold to be appropriate. If the stock is weighted 30/70 stock/cash (bonds) in reflection of AIM suggestion, then 15% stock, 35% short dated gilts, 50% gold is being indicated. Quite a defensive stance perhaps as suggested by relatively low interest rates and much money printing.

suggests that the UK is relatively higher as of recent (AIM indicating a higher %cash to be appropriate). It also did a reasonable job of averaging in/out around the troughs/peaks

Considering that the Dow/Gold is around central 20 versus former 40 high, 1 low, that might suggest 50/50 stock/gold to be appropriate. If the stock is weighted 30/70 stock/cash (bonds) in reflection of AIM suggestion, then 15% stock, 35% short dated gilts, 50% gold is being indicated. Quite a defensive stance perhaps as suggested by relatively low interest rates and much money printing.

-

Hariseldon58

- Lemon Slice

- Posts: 837

- Joined: November 4th, 2016, 9:42 pm

- Has thanked: 124 times

- Been thanked: 514 times

Re: Challenging the 4% Rule

It’s interesting that when people think about a SWR, much of the research concerns the US market and commentators often say the UK is different and point at portfolios only containing UK stocks and bonds.

There is no reason why a UK investor could not base their portfolio on US stocks or global stocks. The influence of the dollar is strong on UK stocks, mitigating the currency factor asa reason not to hold international stocks.

The sequence of returns issue can be mitigated by some cash/bonds to tide an investor over a difficult period in the markets. 15% or 20% would probably cover most investors for a few years spending to cover a crash.

The future is unknowable and an individuals risk attitudes will dictate how cautious they need to be.

Retiring almost exactly 14 years ago with a 90% plus equity portfolio allowed me to experience sequence of returns risk for real !!

It worked out fine, spending needs to be flexible and you may need to adjust your portfolio to adapt to the conditions. In my case in April 2008 I dumped an HYP component of the portfolio and some selective trading in Investment Trusts and subsequently index funds allowed me to recover fully by 2010 and move ahead substantially over the next few years.

With hindsight I would keep the equity down to about 80% or so. It’s cash flow that matters, enough cash / bonds to get through the other side.

14 years later and still a few years short of state pension, sequence of returns does not go away, my position is identical to some one retiring today with a similar portfolio size.

In late March last year a reasonable cash / bond portfolio was reassuring, it allowed me to reduce the bond quota for some trading gains. I have almost rebuilt the safety element of the portfolio…

Until life expectancy is down to around 10 years or so then, sequence of returns issues remain.

There is no reason why a UK investor could not base their portfolio on US stocks or global stocks. The influence of the dollar is strong on UK stocks, mitigating the currency factor asa reason not to hold international stocks.

The sequence of returns issue can be mitigated by some cash/bonds to tide an investor over a difficult period in the markets. 15% or 20% would probably cover most investors for a few years spending to cover a crash.

The future is unknowable and an individuals risk attitudes will dictate how cautious they need to be.

Retiring almost exactly 14 years ago with a 90% plus equity portfolio allowed me to experience sequence of returns risk for real !!

It worked out fine, spending needs to be flexible and you may need to adjust your portfolio to adapt to the conditions. In my case in April 2008 I dumped an HYP component of the portfolio and some selective trading in Investment Trusts and subsequently index funds allowed me to recover fully by 2010 and move ahead substantially over the next few years.

With hindsight I would keep the equity down to about 80% or so. It’s cash flow that matters, enough cash / bonds to get through the other side.

14 years later and still a few years short of state pension, sequence of returns does not go away, my position is identical to some one retiring today with a similar portfolio size.

In late March last year a reasonable cash / bond portfolio was reassuring, it allowed me to reduce the bond quota for some trading gains. I have almost rebuilt the safety element of the portfolio…

Until life expectancy is down to around 10 years or so then, sequence of returns issues remain.

Re: Challenging the 4% Rule

We post on the same boards?

Your retirement with 90% equities is a tough allocation for me to have handled-unless I was Mrs Warren Buffett with a huge portfolio !

Glad you made it through-there must have been some sleepless nights!

I was the other way -over 60% bonds at retirement

Different horses for same courses!

xxd09

Your retirement with 90% equities is a tough allocation for me to have handled-unless I was Mrs Warren Buffett with a huge portfolio !

Glad you made it through-there must have been some sleepless nights!

I was the other way -over 60% bonds at retirement

Different horses for same courses!

xxd09

-

Hariseldon58

- Lemon Slice

- Posts: 837

- Joined: November 4th, 2016, 9:42 pm

- Has thanked: 124 times

- Been thanked: 514 times

Re: Challenging the 4% Rule

xxd09 wrote:We post on the same boards?

Your retirement with 90% equities is a tough allocation for me to have handled-unless I was Mrs Warren Buffett with a huge portfolio !

Glad you made it through-there must have been some sleepless nights!

I was the other way -over 60% bonds at retirement

Different horses for same courses!

xxd09

I thinks that’s the essence of the problem, the search for an “answer” to the retirement drawdown question, it’s different for everyone, there is no single answer.

Personally I am eternally optimistic,I believe that things always pan out and I had no sleepless nights, from a rational outside perspective, I am almost certainly deluded ! Personally I would find 60% bonds excessively cautious, however it would actually work for me.

IE 35 years income required would be a reasonable guess as a maximum lifespan from here, 100/35 =2.85% per year drawdown, a 60% bond/ 40% equity portfolio would likely keep up with inflation and since my expenditure is in a range of 1.5% to 3% for a comfortable / luxury lifestyle, throw-in future state pensions for myself and Mrs Hari it would clearly be a sensible choice.

Equally my present 80%+ equity portfolio has sufficient margin of safety and will probably work out better, there is a chance that will not work out as well. However the last 14 years have given me a higher standard of living than I anticipated and inflation adjusted capital is over double the starting value, if I was to suffer a 50% permanent loss from here I would be no worse off than if I had taken the lower risk approach initially.

Return to “Retirement Investing (inc FIRE)”

Who is online

Users browsing this forum: No registered users and 38 guests