JohnW wrote:The duration of your bond fund is 18 years; that’s an important characteristic for bond investing because it’s the weighted (by £) average of all the future periods that a bond pays out until redemption at maturity. So if most of the money comes to you at maturity as principal, because interest rates are very low and thus coupon payments are very small, then the duration will be similar (but shorter) than the ‘time to maturity’. Keep 18 years in mind for your circumstances (which you haven’t told us).

A rough and ready use of duration is to inform you how much your bond(s)/fund will drop in price with an interest rate rise. x% rise in interest rates will drop the bond’s value by x% times the duration in years. Your fund should fall 18% for each 1% rise in interest rates - very, very roughly, and not for long.

We’ll come back to that, but before you slit your throat at the prospects of further rate rises, just reflect on how good your portfolio is at present. A 60/40 equity/bond mix, yours, is widely considered very suitable for many investors; we don’t know enough about you to pontificate, but it’s not a bad setup for anyone with a good few years to go. Secondly, what sort of bonds should be in the 40%? There are good reasons to think yours are perfect (however unfortunate the timing of purchase was). High quality bonds have poor returns compared to riskier assets; you just have to accept it if you’re going to hold bonds (and most investors probably should). The risks of bonds are: #1 credit risk (you’ve got that covered with UK treasury as the issuer); #2 interest rate risk (the longer the duration, the more the risk as per the formula above, but also the better the yield usually). The only protection against this is short duration, lower paying bonds); and #3 unexpected inflation (you’ve got that covered as well as anyone can with linkers in the currency you spend, although you’ve added the risk that would come with unexpected deflation).

As long as your investing horizon is long enough to suit 18 year duration bonds, you’ve got a bond holding as good as anyone’s. Some would argue that having only linkers does not give you the protection against deflation that nominal bonds do, but inflation is much more common than deflation, and usually more damaging to your spending capacity. You won’t find many people holding only linkers as their bonds, but the logic of their argument is often not there and the size of the effect they’re worried about likely small. Hopefully we’ll hear some discussion on this.

So, I contend, the only ‘worry’ you have is does the 18 years match your investing horizon? At age 60 it probably still does if you’re planning to live off an ‘at risk’ portfolio of stocks and bonds; beyond 60 years, maybe an 18 year duration bond fund is too long, so what’s a solution?

It’s a truth universally acknowledged that a bond holding should duration match the spending horizon of the bond holder. If your spending needs are a long way off, you should have long bonds since they pay better; but since it exposes you to interest rate risk, no longer than your spending needs. You can roughly calculate your spending ‘duration’ as the average of those future spending years eg if you only need to spend for the next 5 years, the duration is (1+2+3..5)/5=3years. If your spending starts in 6 years and runs for 10 years, the duration is (1+2+3…10)/10 add 6=11.5 years.

Since a bond fund’s duration usually stays unchanged, but your spending duration naturally keeps getting shorter, in order to ‘duration match’ your bonds with your spending you might need/want another (bond) fund (could be cash) which when ‘mixed’ with your long (18 year) bond fund in their relative proportions gives a combined duration that matches your spending horizon. Here you can read about it: https://www.bogleheads.org/forum/viewtopic.php?t=318412

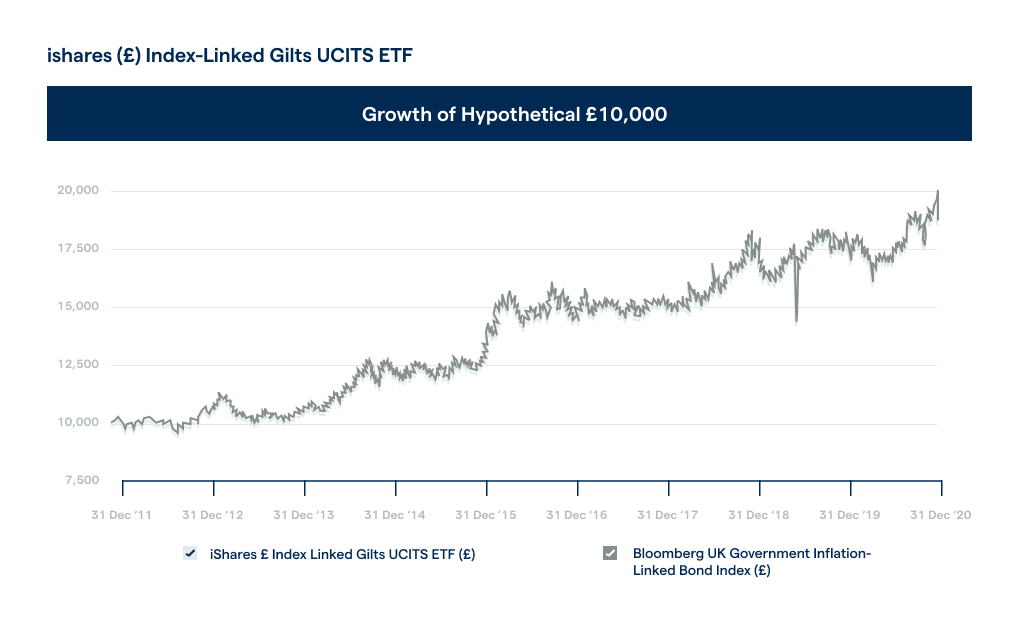

Finally, we come back to your 18% drop for every 1% rise in interest rates. How dramatic that fall is, whether it’s actually 12% not 18%, how quickly or slowly the fund recovers its value as the new higher paying bonds come on line varies with the prevailing economic circumstances. Have a look at this bond fund rising inexorably through rising and falling interest rate periods, where the ’18%’ formula just doesn’t seem apparent. https://www.bogleheads.org/forum/viewto ... 2#p5846789

And look at this theoretical analysis showing how your bond fund can recover, hopefully giving you some comfort. https://www.bogleheads.org/forum/viewtopic.php?t=360575

You might have stumbled on a genius portfolio, but make the next move well informed.is there a calculation that can be made to roughly determine the value of an ETF IL bond within that year or two?

I don’t think you can do that, as it relies on predictions, and here’s what we know about those: https://www.marketwatch.com/story/yes-1 ... 2014-10-21

An alternative viewpoint is that bonds should be held to duration match spending over a shorter time frame after which there is very high likelihood that equities will outperform significantly. The stats suggest that is 10 - 15 years.

That delivers certainty of cash irrespective of the shorter term volatility of equities. Whilst optimising outperformance probability.

The equity:bond split becomes an output, but will be more like 80:20 for a younger person, but tending towards 10:90 once one hits 70.

Chris