simoan wrote:Dod101 wrote:simoan wrote:Dod101 wrote:Gave up on Smithson today at £1.27. Should have done it long before but I still came out with a 27% profit. As I said earlier I do not like the governance nor the very high management charges and I will not just sit and watch the profits ebbing away.

Dod

This is remarkably short term thinking. You need to question the whole psychology of "I will not just sit and watch the profits ebbing away". I assume you only feel like this because it pays a very small or no dividend? Maybe if it was paying a 5% dividend you'd feel very differently, which makes no sense IMHO. A reduction in capital always matters, regardless of any income generated. You may well have just sold near near the bottom with the IT on a 11% discount! If you've ever read "The Art of Execution" (one of the great investing books IMHO) then this is a bona fide losing strategy. Although I'm not over the moon with some of the holdings, and never really have been (i.e. Domino's and Rightmove) I'd be more inclined to buy more than sell at such a discount, and may in fact do so myself.

All the best, Si

Yes I have read the Art of Execution and understand very well what it is saying. Call it short term thinking but as I said earlier in the thread, I am rather prejudiced against Terry Smith anyway, what with the very high charges, and as I said, I do not much like the corporate governance either.

Obviously, biases and prejudices are hard to overcome but generally are not helpful, and often harmful, for making good investment decisions. I'm not aware the corporate governance or charges of Smithson IT have changed adversely recently, so can't understand why that forms part of your reason for selling now.Dod101 wrote:I hold Scottish Mortgage and will continue to do so, for two reasons, one its charges are very low and secondly I took a lot out of it during its meteoric rise a couple of years ago. That is my only reason for buying out and out growth shares, and I made the mistake of not doing the same with Smithson.

Incidentally Smithson does not pay a dividend; Scottish Mortgage pays a very small one, partly from capital. I do not buy growth shares for the dividend though.

Dod

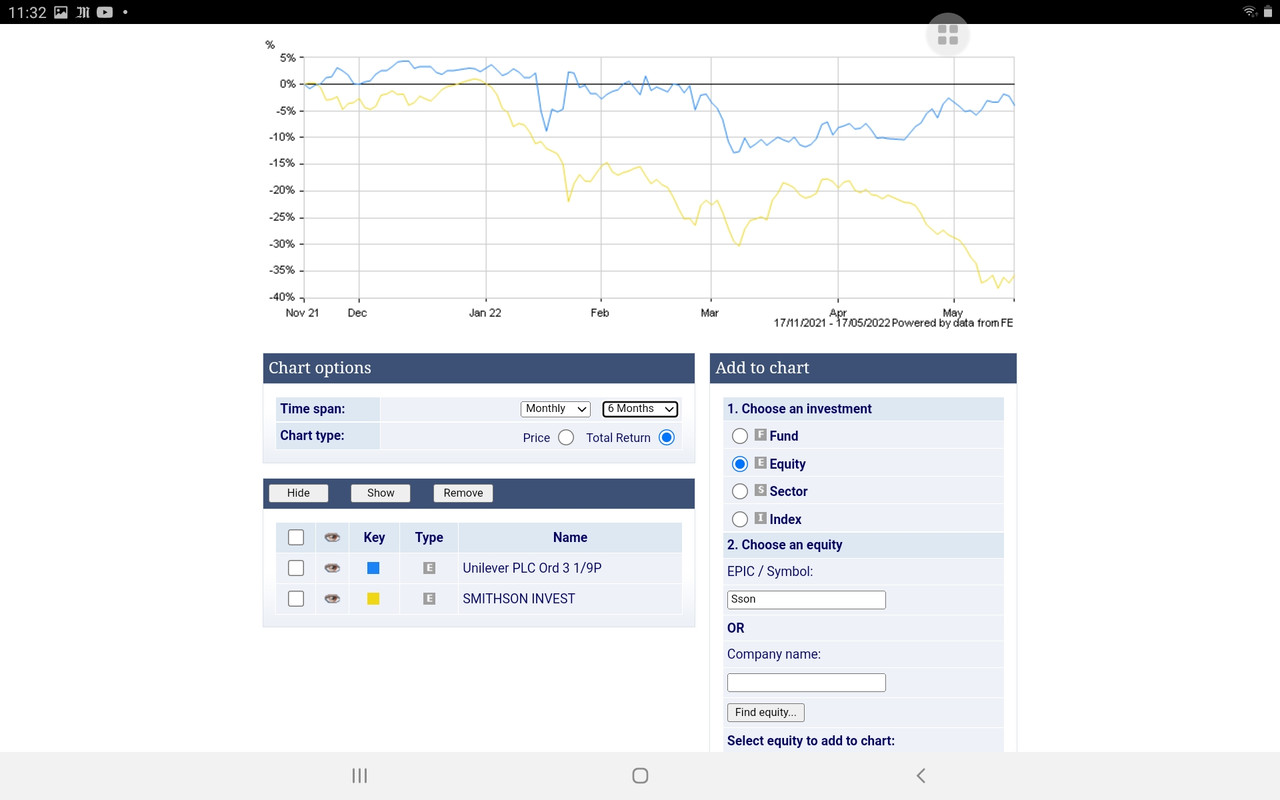

Again, you are displaying a bias because you have done well from Scottish Mortgage in the past. However, that doesn't mean it will do so well in the future, and I believe the long-term fund manager has retired recently, which is often not a positive sign for future performance. And in fact it has significantly underperformed Smithson in the past year.

As far as Scottish Mortgage is concerned we should not be discussing it on this Board, I guess, but the difference between it and Smithson is that I doubt very much that its performance depended on the recently retired James Anderson. Tom Slater who has assumed the role as manager, is very much from the same mould and in any case they have the entire team from the long established and successful Baillie Gifford behind them. As I said, that coupled with low charges and good corporate governance gives me confidence that I can just leave my investment there.

I knew when I invested about the high charges from Smithson but I had not really focussed on their corporate governance. So I missed a much bigger profit but I am still out with 27% or so which is better than a kick in the teeth. I hope current holders do well and I will watch with interest, but with no regrets whatever happens.

Dod