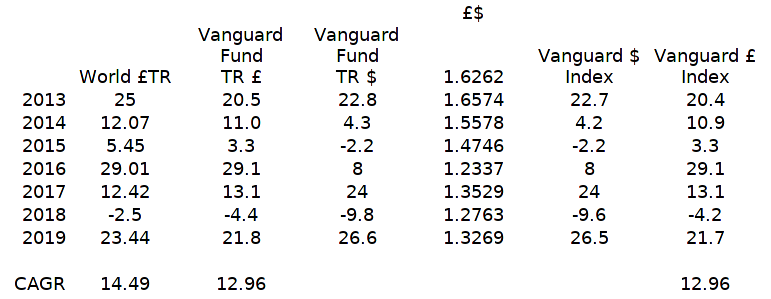

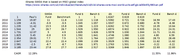

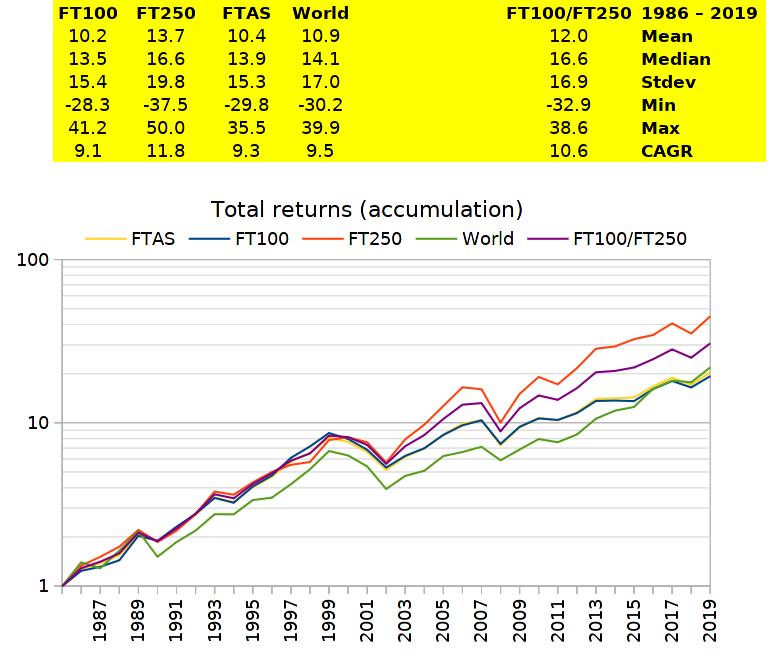

https://www.bogleheads.org/wiki/Global_ ... ex_returns and applied £/$ conversion.

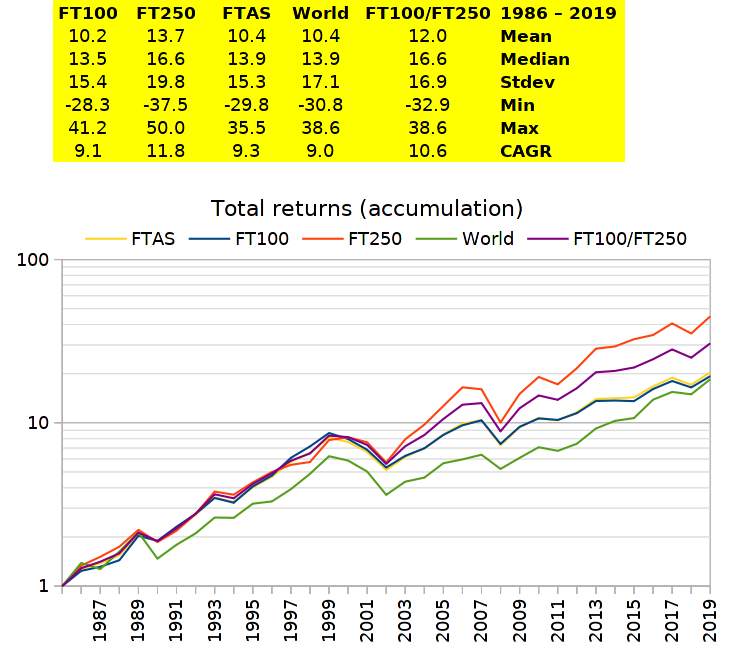

FTAS data was in part sourced from older Equity/Gilt study data and more recent from

http://www.swanlowpark.co.uk/ftseannualVolatility is considered a risk to some, a benefit to others, such as if you rebalance between high and low volatility holdings, or inversely correlated, where more movement tends to scale up combined benefits.

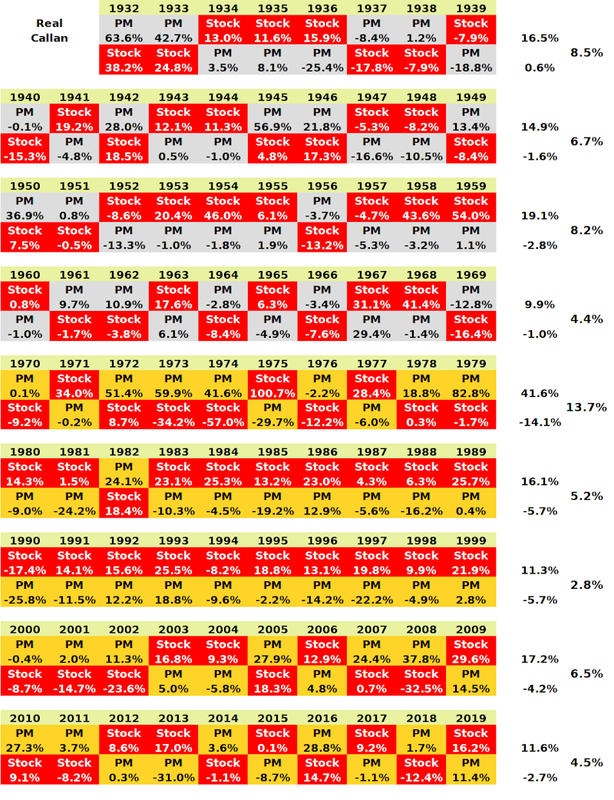

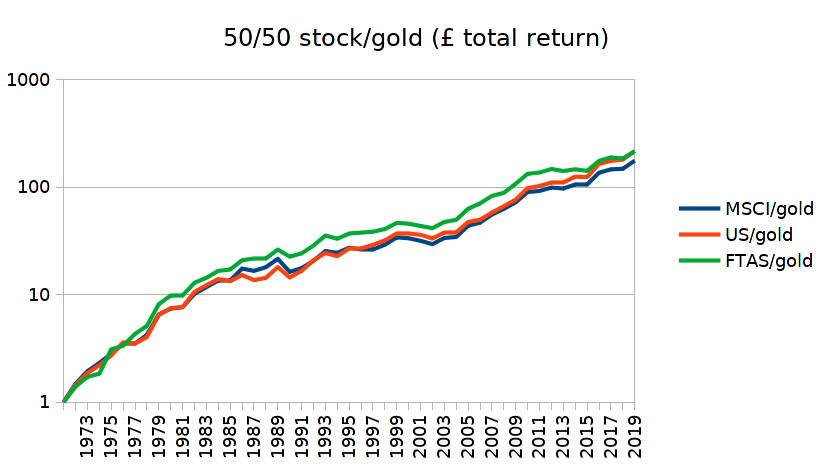

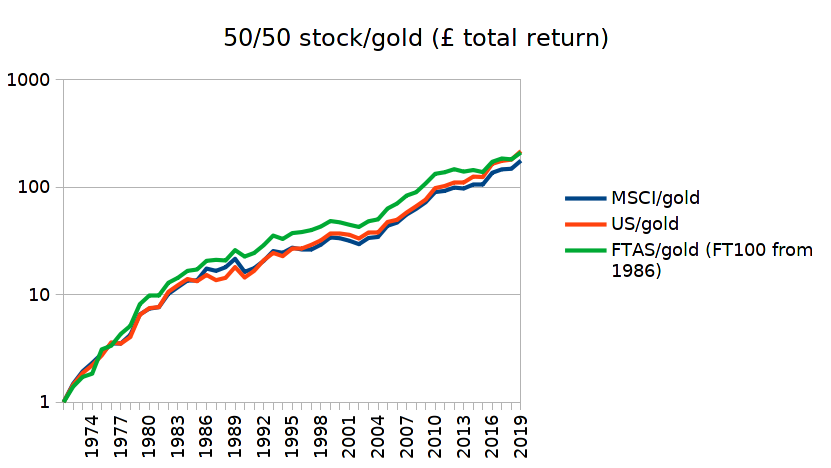

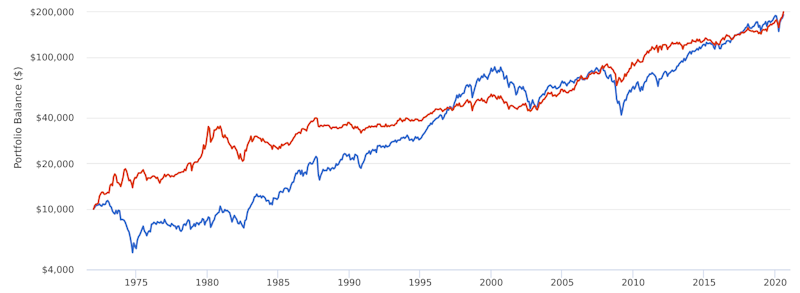

I consider a 50/50 barbell of stock/gold (silver 1932 to 1970 as the US still was pegging the $ to gold) to be a form of central currency unhedged global 'bond' bullet, which provides enough 'foreign' currency diversification. Stock in this chart is again FT Composite/FT All Share based data.

More recently I've been pondering whether rebalancing is even needed/appropriate. Could be enough to simply just add to the lagging asset value if saving/accumulating, or draw from the leading value asset in drawdown. Again that does introduce a higher standard deviation, but similar overall rewards. I particularly like that really passive option as with some magic wand waving I can buy and sell physical gold (coins) at effectively spot gold prices, so combined 50/50 with Vanguards FT All Share accumulation unit trust that has a 0.06% expense, that comes out at a 0.03% portfolio expense (that if I open a iWeb account and hold via that brokerage, there are no further costs). That wand waving however does take time/effort so I'd rather just be doing it the once rather than repeatedly (as one year gold was reduced to add to stocks and the next year stocks being reduced to buy back gold again - would involve further wand waving that might not be as easy as at present in the current low interest rate environment).

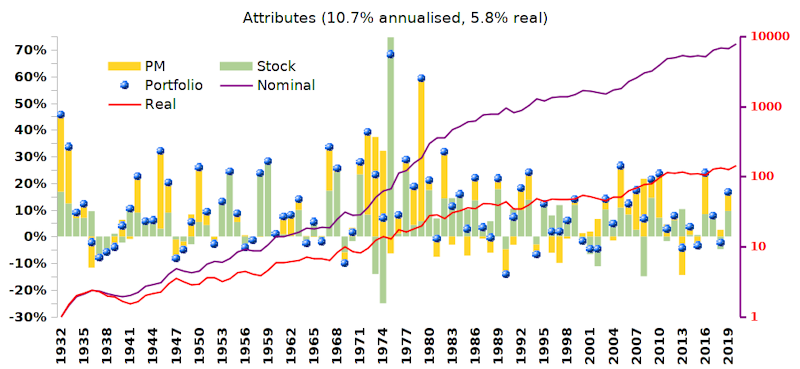

In the above chart the bars are staked and are the weighted gains, i.e. 50/50 stock/gold with stock up 20% would have a 10% stock bar in the chart. With 50% of the gold gain staked on top (or deducted from) the stock bar. The blue dots show each years actual 50/50 stock/gold gain/loss. The accumulation lines for nominal and real are relative to the right hand log scaled Y axis.

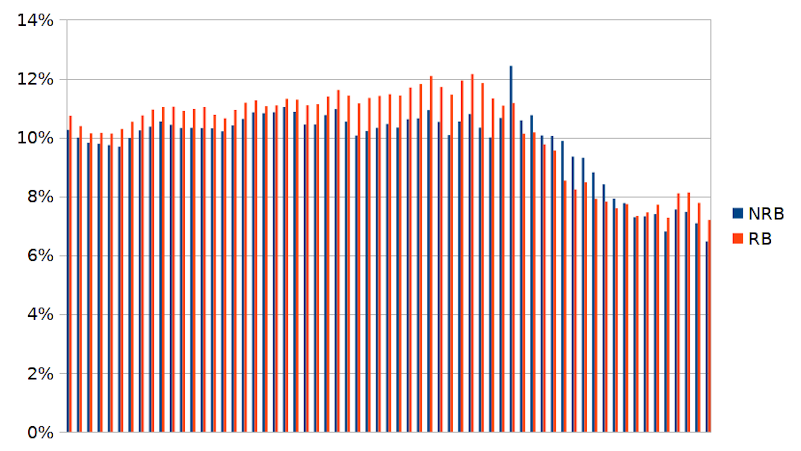

Looking at all start years since 1932 up to 1994 for 50/50 stock/gold either rebalanced, or not rebalanced running up to the most recent date (end of 2019) rebalancing did reward more than not rebalancing for many of cases, but not always. And rewards were close enough to tolerate some relative under-performance from not rebalancing in view of better cost/tax savings.

I quite like the totally passive choice of loading 50/50 into a accumulation stock index and gold, and not rebalancing other than just (retirement) drawing from either stocks or gold according to whichever was the higher capital value.

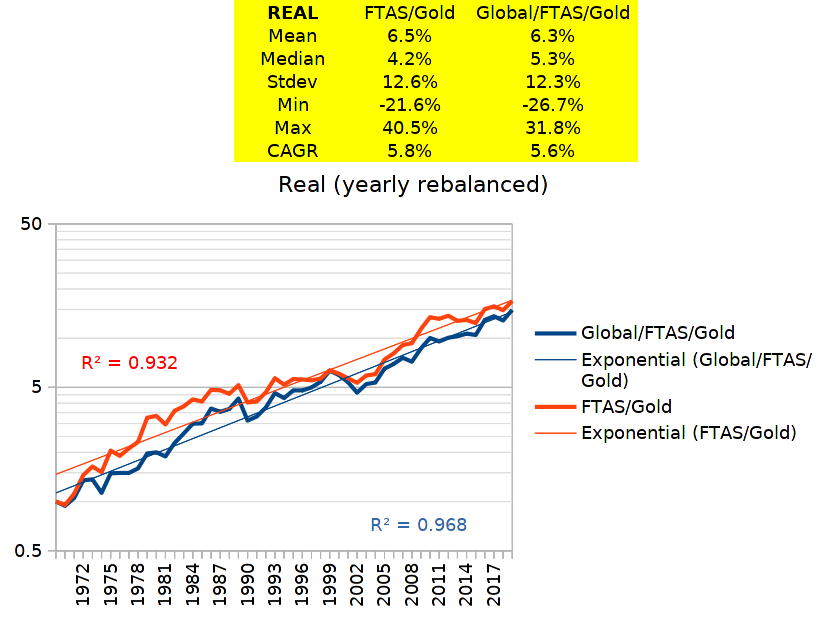

Still struggling however between whether the stock should be FTAS (Vanguards accumulation unit trust (0.06% expense)), or global (HSBC's global accumulation unit trust (0.13% expense)). The UK with the likes of Unilever that has sales in over 190 countries, global miners, global banks, global oil, global pharmaceuticals ...etc.) could already be global enough. Higher tax/cost savings. But I also like how a global holding would be dynamic enough to track the overall global drift that may occur over time. Plan is to open several different family members iWeb accounts and load into those, could end up perhaps with a three way equal initial split of FTAS/global/gold. Some rebalancing will occur between those accounts over time (capital flows), so there would be natural tendency to redirect each account towards being equal weighting of the three assets anyway.

https://www.markets.iweb-sharedealing.c ... 00B3X7QG63