forrado wrote:1nvest wrote:After such great/fast gains its more often better to take some off the table. Japan had a great 1970's/1980's for instance, flat/down for a decade or two following that. Wall Street Crash was preceded by fantastic gains during the "roaring 20's" where stocks doubled, doubled again and doubled yet again - but then went on to halve, halved again and halved yet again. Buffett who is more usually a 10% reserves stylist is more recently up to 30% reserves.

Even more advisable for those about to / or who have already entered the drawdown phase.

"

When you’ve won the game - stop playing" is a quote that has been attributed to

Bill Bernstein, American

Modern Portfolio theorist and long-time supporter of passive investing. He advocates a matched liability strategy, one that matches future assets sales and income streams against the timing of expected future expenses.

In the absence of adequate pension provisions, being overly dependent on the performance of equites (often referred to as

sequencing risk exposure) as a means of generating distributions is not a comfortable place to be.

Liability matching 'rent' is easy. Own your own home, so you're not having to find/pay rent to others as you're both landlord and tenant - doesn't matter if rents soar or collapse.

Liability matching disposable income is the main factor. Inflation bonds (index linked gilts for instance) seem to be the ideal, but tend to be plentiful in times of low risk/can largely vanish at times of 'payout'. Remember that Gilts are loans to a individual who can print money, set interest rates and taxation levels. Whilst some states such as the US tend to respect support of their population and ensure such protections persist across times of 'payout', others such as the UK do not and are inclined to 'default' - more often partially via manipulation of taxes/policies.

The ideal would be a choice of a secure net 4% real 'inflation bond' so that individuals could precisely plan how much they needed to save and when that was drawn. Where the risk was solely longevity. Along with collective health insurance and support rather than the onus being thrown onto each individual. Sadly the trend is away from security/safety and far more towards individual risks, which means that individuals have to accumulate much more in order to get anywhere near being reasonably protected.

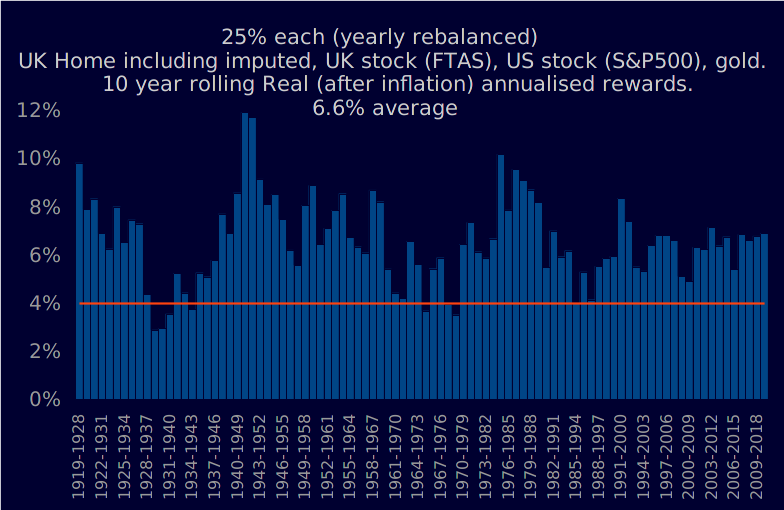

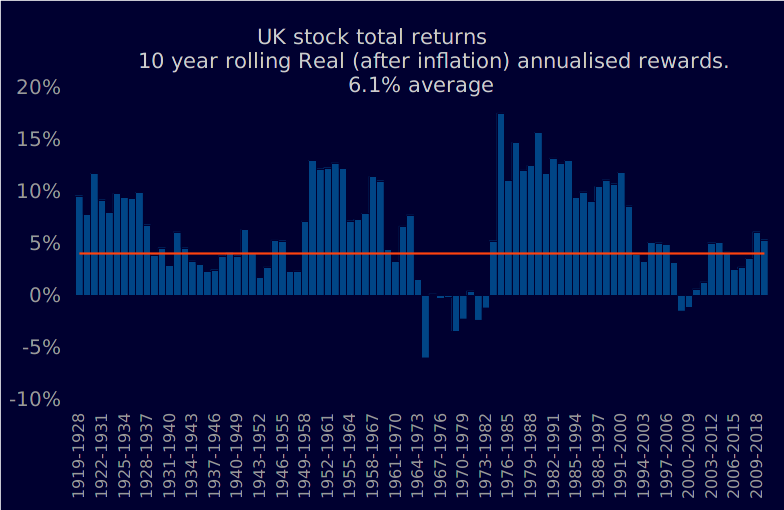

The closest safe 4% real type 'inflation bond' I've found is a quarter each of home, UK stocks, US stocks, gold. More consistently achieves 10 year inflation beating outcomes. A home is more aligned/correlated to gold, both can do well during periods of negative real yields. When real yields are negative those with a mortgage can in effect be being paid for holding such. UK and US stocks tend to correlate and do well during prosperity, when typically real yields are positive. Such a 4 way 'barbell cross' is reasonably neutrally balanced, half £ half foreign currencies (half primary reserve currency US$, half global currency (gold)), half land and commodity (gold) physical assets half equities. Home + imputed is somewhat similar to share price + dividends. 50/50 equity/gold barbell combines to be like a currency unhedged global bond bullet. If 75% of equities ... home/UK stock/US stock - do collapse in half, then the 25% in gold may typically rise 2.5 to 3 fold and negate the losses.

All very subjective, but if such a 'inflation bond' has reasonable 10 year consistency of positive real yield outcomes of the order 4% lower, 6% average - then that looks good enough. But as you say sequence of return risk should also be factored in. Applying a 3% SWR is safer, along with a possible discretionary additional 3% on top, Which isn't so bad as that also excludes imputed rent (which proportioned historically was worth another 1% i.e. 4% average historic rental yields) and that also factors in a higher inflation rate of 25% house price inflation, 75% CPI as the inflation rate. When you expand the capital base i.e. include home value as part of the portfolio that also lowers the SWR % figure, same amount of income £ value being drawn from from a 33% larger capital base (home value 25% of total).

Perhaps VUKE, CSP1, SGLN funds. Or if you fancy blending small cap (which the FT250 is in US scale) with large cap (US stocks) instead, then VMID instead of VUKE. CSP1, US S&P500 primarily for its accumulation i.e. dividends rolled up, as otherwise within ISA if dividends were paid in US$ you end up with two lots of currency conversions due to not being permitted to hold foreign currencies within a ISA. Personally I prefer the FT250 instead of FT100 and year on year that's also had a good (fiscal) year.

Of the order +60% US stock, +55% FT250, +2% house prices, -5% gold type fiscal year individual changes. 29% for the year including imputed rent, but without having actually looked at recent actuals. Bearing in mind that a year ago was a big down/trough ("start of Covid"). Slide across to calendar year measures and the FT250 for instance was down -5% for the year. From 2020 year start the end of March 2020 -37% downslide in FT250 required a +58% gain to get back to the -5% down break-even level - in nominal terms, even more after factoring in inflation.