Hi OLTB

OLTB wrote:This is an experiment that I set up two years ago to see if Harry Browne's 'Permanent Portfolio' would work in the modern era. Currently I run a HYP, IT portfolio and passive portfolio and wanted to see if a Permanent Portfolio strategy would be less hassle and better wealth-wise for me for one/two/all portfolios once I retire in about 14 years time.

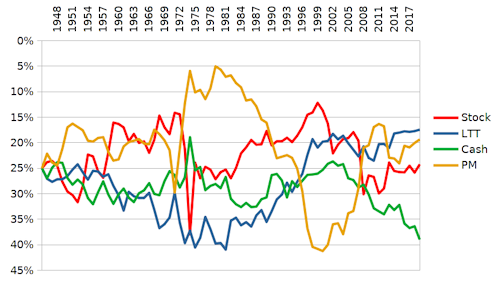

The Permanent Portfolio is a bit too heavy on 'bonds'. Combined 50% in a barbell of short dated Gilts and Long dated (20 year) Gilts equate to 50% in a 10 year Gilt bullet. 25% stock, 25% gold, 50% 10 year Gilt type allocation.

50/50 stock/gold is also a barbell of two extremes, that combine to be like a central - currency unhedged global bond, and a volatile one at that.

Really (very subjectively - as outlined below) both of those need more tilting towards 'equities'. 67/33 or 75/25 are nice choices IMO. 25% in US S&P500, 50% in UK FT250, 25% gold ... significantly reduces single stock/sector risk factors. Large cap indexes can end up holding 10% in single stocks, and perhaps 30% or more in single sectors. Mid cap (such as FT250) are much less prone to such concentration. And periodically such concentration backfires. Tech sector/stocks post dot com bubble bursting, Financial stocks post 2008/9 financial crisis. Even Japan post 1990's when massive giants faltered, but even after having halved or more they still remained large and dominated the Japanese stock index.

50% FT250 (£), 25% US$ (primary reserve currency), 25% gold (global currency and also a commodity) ... has you neutral on the currency front (half £ half foreign), whilst reducing down single stock/sector risk factors.

Whilst historically gold has acted as a drag factor, for instance a third S&P500, two thirds FT250 has pretty much compared to HYP's, at times having included gold does float the portfolio, helps smooth things down, and over other periods can be beneficial.

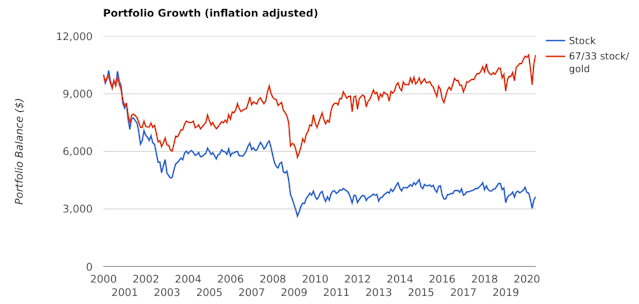

With (history depicted) caveats, including around 25% to 33% gold in a portfolio has provided more consistent rewards over all of time - at least going back to 1825. If you measure the 30 year real (after inflation) gains from all-stock, and compare that to 67/33 or 75/25 stock/gold for all 30 year periods, and then measure the median (average) of all of those, then the gains are very similar to that of all-stock, near-as identical. But the all-stock set is more volatile, sees wider deviations in the 30 year annualised gains. The 1980's/1990's strong Bull for all-stock has many assuming such historic pattern will persist into the future. It wont. Sometimes you miss the trees for the forest. Since 2000 (US data) drawing a 4% inflation adjusted amount from all stock compared to a 67/33 stock/gold blend ...

has seen remainder of the £10,000 start date inflation adjusted portfolio value decline. 2000 onward has been more like the 1970's when holding some gold was better than not. Over the 1980's/90's it was better to not have held gold - but the rewards were still reasonable if you did hold some gold but not as good as the great gains if you'd held all-stock. Over all of those cycles it was better to hold gold than not, and that pattern repeats back over very long term history. In some multiple decade periods gold will feel like a liability, where you are repeatedly reducing stocks that had made good gains, to add to gold, increasing the number of ounces being held, but where the price continued to decline. Over other periods however all of the accumulated ounces of gold could be a saviour for the portfolio, or at least have been 'handy' such as the above 2000 onward chart.

Consider 50/50 stock/gold barbell as a form of bond bullet, and the PP is a form of all bond. As-is 50/50 stock/gold. 75/25 stock/gold in contrast is more like a 50/50 stock/bond holding, and historically such 50/50 stock/bond has served investors well, tending to provide relatively consistent rewards over periods of both economic expansion and contraction (less cyclical in its rewards). Or even a third each S&P500, FT250 and Gold, for $, £ and global currency diversification, and a 33/67 type stock/bond type asset allocation. Personally I favour the 75/25 - as the tables/charts above, for 50/50 £/foreign type levels, as if the Pound is soaring being just a third in that is a bit too light for my liking.

I think you'll find the Permanent Portfolio, whilst tending to have low nominal yearly losses in bad years, usually single digit losses at most, is not exempted from large real (after inflation) losses/declines. A stable nominal value is nice if you only look at that, but what really matters is the real value. 50/50 stock/gold is nice in that more often one or the other will do well in most years, but there will be years when both decline (or rise). Perhaps better suited if you also own your own home and want to run with a Talmud type asset allocation of a third in land (home), business (stocks) and in-hand (gold). Home + imputed rent benefit compares reasonably to stock + dividends, so in that sense that is a 67/33 equity/gold type overall holding. For rebalancing that you can add/reduce additional UK stock holdings, maybe even of the REIT variety, as a form of liquid 'home' value. A nice aspect of owning a home is that you don't have to find/pay rent to others, your 'rent' is liability matched (de-risked). And if you're home value is £333K, and you have £666K liquid assets, invested 50/50 stock/gold, then there's a great probability that you could not only draw a £20K/year inflation adjusted reward from that as a disposable income (2% SWR), but also would have around £13K/year of imputed rent benefit included as well as part of that. And with such a low SWR you'd tend to also see real total wealth expansion over time - such that additional income might be periodically drawn out of those real gains.

Yet another consideration is pensions - which might be counted as a form of 'bond'. Someone who has £8K of state pension, £12K of occupational pension might not need to hold any bonds at all. The combined £20K/year income from those pensions might be considered as 'enough' from a bond like income production 'asset'. Fundamentally you need to consider such 'assets' as owning a house, pension incomes ...etc. as part of your overall asset diversification. Not restrict your view of diversification as being just a bunch of stocks with business activities in different sectors ... or whatever.

Fundamentally

1. If you own your own home, and also have a reasonable pension income, then all stock could be fine. HYP, or either 67/33 or 75/25 stock/gold, or even 50/50 stock/gold could serve you well.

2. If you rent and have no pension(s) then you're much more reliant upon a regular/consistent inflation adjusted investment income, then IMO all-HYP (stock) is a risk, A stock/bond blend helps de-risk that. But where the Permanent Portfolio is likely insufficiently rewarding enough. 67/33 or 75/25 stock/gold would be the choice IMO.

Commonality is the 67/33 or 75/25 choice. And where that can achieve the median all-stock type reward, but with less risk (volatility).