Newroad wrote:Indeed 1nvest.

Geopolitical diversification is one thing I certainly do have (in spades).

Not just for the risk mitigation, which you rightly mention, but also to give flexibility to the "active" 50% of the portfolios - so their managers can overweight where they think the greater opportunities to be - should they judge to do so.

Regards, Newroad

Yes thanks Newroad, you spiked my interest in IT's and since then I've looked at FCIT and PNL as a form of stock/bond pairing. Even discovered that PNL will pay all ii fees/costs if you only hold PNL within your ii account. Which led me on to reading about Freetrade as a low cost compliment brokerage. Haven't actioned any of that, at least not yet.

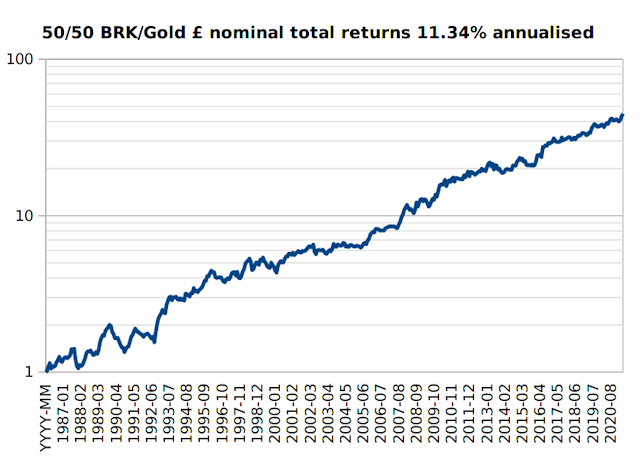

I guess my preferences grew out of the likes of Barclays Equity Gilt Study data that show how stock inflation adjusted price and income indexes can at times perform poorly, -75% declines in prices, -85% declines in dividends, over extended periods (20 years down-run, and continuing to stay down for decades). Along with other comments/observations such as Warren Buffett's 1979 Berkshire Hathaway Chairman Letter ...

One friendly but sharp-eyed commentator on Berkshire has

pointed out that our book value at the end of 1964 would have

bought about one-half ounce of gold and, fifteen years later,

after we have plowed back all earnings along with much blood,

sweat and tears, the book value produced will buy about the same

half ounce.

A function of money printing

..The rub has been that government has been

exceptionally able in printing money and creating promises, but

is unable to print gold

Which leads to the pondering of how one might actually feel if such situations occurred to ones own case (for real).

SWR withdrawals better ensure a regular inflation adjusted income. History also suggests that 4% SWR is relatively safe, but can lead to zero remaining after 30 years. 3% is safer ...etc. But when you look into the historic more stressful cases that does mean having to ignore capital values as at times the portfolio value can decline to 30% of former inflation adjusted value. At such times a 3% SWR is in effect 9% or more of the ongoing portfolio value, which I suspect might induce sleepless nights, even though historically from such lows recoveries subsequently occurred.

High to low 1980 to recent interest rate transition has been great for both stocks and bonds, even inflation bonds have provided 4% real type rewards. But in recently retiring that rising tide is/has peaked, for the 30/whatever years I might have remaining ???

There are many roads that can all lead to the same place, primary is taking a road that you are most comfortable with, less likely to bail out when stress levels rise/peak. All stock and drawing a low/safe SWR has great appeal, HYP as a annuity type style, treat the money as having been spent, ignore the capital and target just income production objective. All stock and a 3% SWR historically worked and more often left the most remaining at the end of 30 years, but I'm unsure as to how well or not I might actually handle a situation such as being down at 30% of former portfolio value and where drawing the next years income would push that down more toward 20% remaining. Separate cash reserves/pot to sustain you through times when stocks are down fails to recognise that cash also can be substantially down, i.e. high inflation was the culprit, in which case cash/bonds provided no protection, could even have made things worse.

A factor for me with IT's is that they can have great flexibility. PNL for instance can buy into pretty much whatever it likes in whatever amounts it likes and even add in leverage/gearing ..etc. Whilst I respect the managers abilities I however lack total trust. If for instance they deemed a low had occurred and opted to go for 200% long stock exposure in the belief that stocks only had one way to go then that's perfectly within their remit but could be disastrous. To reduce a whoops we got it seriously wrong you have to diversify, which entails overlap/duplication ..etc. Factors I may not want to or be able to manage in my dotage. Simplicity of own a home, a major accumulation index fund and some gold has the simplicity of just sell down either stock or gold each month for income according to whichever is the higher valued that likely will serve as well at sustaining income/spending objectives come what may.

I have see others mentioning their 8, 10, 20 ... whatever IT's but seeing your four spiked my interest for its relatively good balance/diversity. That does look well placed as-is to me.