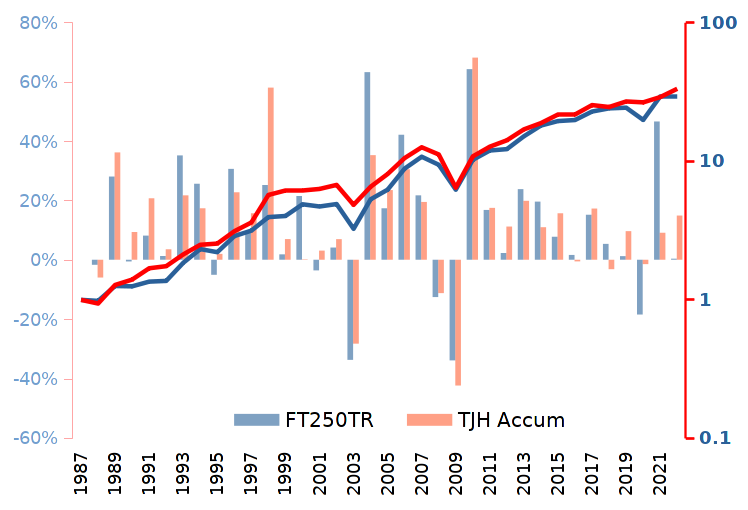

When you put aside individual stock selection and dividend/income management/focus, reducing such to a single click factor (FTSE250 index fund), perhaps drawing income using SWR that yields a regular inflation adjusted income (yearly, monthly, whatever you prefer), then that can lead to better secondary level analysis/management. For instance you can reliably short that portfolio via single clicks, either selling, or by adding a short FTSE250 if otherwise selling might induce a taxable capital gain event. And/or you might combine both long, short and leverage alternatives in weightings that for instance open up generally migrating funds from one account to another, such as from SIPP to ISA. With SIPP's you don't pay any tax on the way in, pay tax on the way out, with ISA you pay in out of taxed money, but are tax free on the way out. Pay in via SIPP, withdraw via ISA and you side step tax altogether. SIPP capital migrated into ISA also becomes accessible (spendable) where otherwise that might not be a option (can't draw/spend from SIPP until a certain age).

Or other such considerations, for instance I'm not a all-stock investor, instead I combine stock with gold - as a portfolio hedge. If you own your own home, have a decent pension income, then for some they might opine they need no bonds and go all-in on a stock. I'm somewhat in that category however I prefer the comfort of a portfolio hedge. Along the lines of a assumption that during a 30 year/whatever investment horizon period at times stocks might dive, whilst gold might do well at such time. If 66.6 initial stock value halves to 33.3, whilst 33.3 gold value doubles to 66.6, then rebalancing back to 67/33 stock/gold weightings has exposure back to as before, but where the number of shares held have been doubled-up. Which is a Martingale betting method, after each losing play (stocks halving/gold doubling), double-up on your stake (number of shares). All very conceptual, but where 67/33 stock/gold in effect runs along those lines. This US

PV example indicates how 67/33 stock/gold broadly compared in reward to all-stock, but did so with lower risk (higher Sharpe Ratio) across 1972 to recent.

Looking at Monte Carlo simulations, again US based data, and 100% stock with a 30 year 4% SWR had a 86% success probability, whereas for 67/33 stock/gold that increased to a 96% probability

PV MC. Many a 65 year old retiree will have a lower probability of actually living another 30 years.

This is another example (again US data), where instead of 67/33 stock/gold the position is held as thirds each in 2x stock/bonds/gold

PV, which might be preferred/useful in some cases such as with migration of capital between accounts or tax efficiencies in mind.

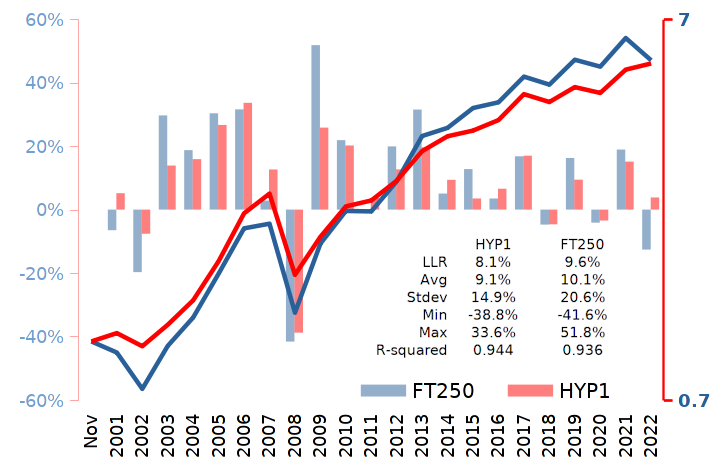

Much of the above might be irrelevant to the unconcerned, who prefer to just set and pretty much forget their investment portfolio. Whilst HYP might be appropriate for those who instead prefer to dabble, as a hobby, then there are alternatives such stock/dividends dabbling as the above (capital migration dabbling ...etc.).