1. https://www.marketwatch.com/story/the-s ... 2021-01-08

2. http://www.philosophicaleconomics.com/2 ... t-returns/

current-ish: https://fred.stlouisfed.org/graph/?g=qis

3. https://www.advisorperspectives.com/ima ... 8ce69e.png

4. https://www.visualcapitalist.com/the-bu ... r-concern/

5. https://www.multpl.com/shiller-pe

6. https://www.gmo.com/americas/research-l ... ast-dance/ (Jan 2021)

Got a credit card? use our Credit Card & Finance Calculators

Thanks to eyeball08,Wondergirly,bofh,johnstevens77,Bhoddhisatva, for Donating to support the site

food for bears

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

{kind=link}

-

NotSure

- Lemon Slice

- Posts: 916

- Joined: February 5th, 2021, 4:45 pm

- Has thanked: 681 times

- Been thanked: 314 times

Re: food for bears

But it's different this time!

Seriously though, as pointed out in your links, by all traditional metrics shares have never been more expensive. I am pretty nervous - a good chunk of my pension contributions are in global trackers, and US growth stocks make up a large percentage of this.

However, is at least a part of this down to what genuinely is different this time - zero interest rates and QE? I can still remember when BTL landlords would not touch a property that didn't yield 10%. They figured in a good year (5% mortgage rate) they would profit after costs, they could survive a bad year (10% mortgage rates) and appreciation was just the cherry on the cake. People were locking in 5% IR as it felt like the deal of the century at the time.

So historically, a P/E of 15 was OK, 20 seemed a bit steep and 30 was a bubble. Not sure that argument holds now, or in the foreseeable future.

Personally, I'm leaving my pension as it is (when you take a weighted average of the funds, it equates to something like a Vanguard LS80). My logic is if I take a big hit, so be it - I'll be in good company - whereas if I try to be 'clever' and take a big hit, I'd never forgive myself. But in the ISA I have started recently, I cannot resist a bias towards 'value' - UK, HY, EM, Asia Pacific.

Strange days - everyone knows the price of everything is at nose-bleed levels, but the assumption is that the conditions that have caused this are unlikely to change. Take a brave person (e.g. Grantham) to fight it.

Seriously though, as pointed out in your links, by all traditional metrics shares have never been more expensive. I am pretty nervous - a good chunk of my pension contributions are in global trackers, and US growth stocks make up a large percentage of this.

However, is at least a part of this down to what genuinely is different this time - zero interest rates and QE? I can still remember when BTL landlords would not touch a property that didn't yield 10%. They figured in a good year (5% mortgage rate) they would profit after costs, they could survive a bad year (10% mortgage rates) and appreciation was just the cherry on the cake. People were locking in 5% IR as it felt like the deal of the century at the time.

So historically, a P/E of 15 was OK, 20 seemed a bit steep and 30 was a bubble. Not sure that argument holds now, or in the foreseeable future.

Personally, I'm leaving my pension as it is (when you take a weighted average of the funds, it equates to something like a Vanguard LS80). My logic is if I take a big hit, so be it - I'll be in good company - whereas if I try to be 'clever' and take a big hit, I'd never forgive myself. But in the ISA I have started recently, I cannot resist a bias towards 'value' - UK, HY, EM, Asia Pacific.

Strange days - everyone knows the price of everything is at nose-bleed levels, but the assumption is that the conditions that have caused this are unlikely to change. Take a brave person (e.g. Grantham) to fight it.

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

More food for bears - no paragraphs, just graphs.

https://am.jpmorgan.com/content/dam/jpm ... ets-us.pdf

Absolutely worth sitting down and going through the whole thing. Very, very interesting.

https://am.jpmorgan.com/content/dam/jpm ... ets-us.pdf

Absolutely worth sitting down and going through the whole thing. Very, very interesting.

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

1. Current CAPE SP500 is 39.2. Historical average 15.8. https://www.multpl.com/shiller-pe

2. Current PER SP500 estimated at 29, historical average around 15. https://www.multpl.com/s-p-500-pe-ratio

3. Current price/sales SP500 is 3.15x. Long term 1.5x.

4. [1-3] all suggest that if the market were to mean-revert right now the SP500 would lose 50% in real terms.

5. If the SP500 were to overshoot the mean to historical lows, we'd be looking at 80%+ drop in real terms.

6. Buffett ratio of total US market cap vs GDP at 213%, vs historical trend of 120%, i.e. 71% overvalued. Implying 44% drop to mean revert.

7. Household stockmarket holdings as % of portfolios is now equal to all time high of the dotcom era.

https://fred.stlouisfed.org/graph/?g=qis

8. 2-year government debt in Australia spiked from 0.1% to 0.8% in just one day last week, after the central bank decided not to defend against the market movement. Yikes. Potentially a big impact on fixed rate mortgages, short-term company debt costs if it doesn't drop back, or if we see this in other debt markets.

9. Property & construction are about 30% of the Chinese economy and are looking into a bad debt tsunami and new property tax. May impact some UK companies - HSBC, Standard Chartered, miners? May broadly impact world economy. Multiple large chinese property developers have defaulted on some debt or missed payments and are in pre-default.

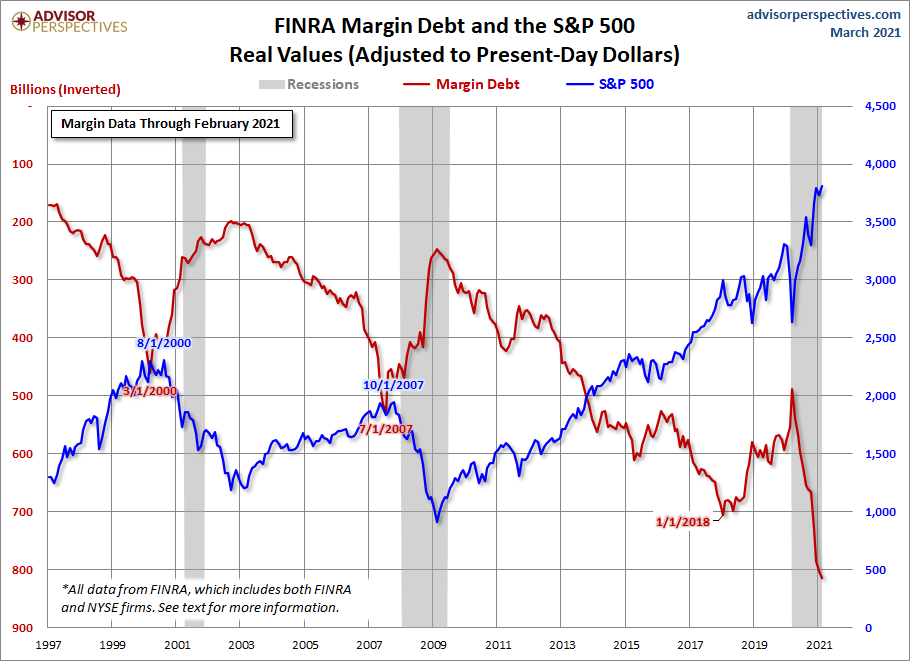

10. Use of margin debt vs SP500 level is now at an all-time record high far above any past mania or bubble. This does not include growth in use of options which I understand to be very high and often combined with margin (and I'm told, funded by a credit card.... smh). Note that this metric is measured against the SP500 which itself is already at an all-time high. If you measure against something more stable during bubbles - e.g. GDP, or aggregate sales of the SP500 - this figure for use of margin will look completely off-the-chart insane. Finally note this chart is dated for September and the market has zoomed up even higher since then.

https://www.advisorperspectives.com/ima ... 59a77b.png

11. Economic backdrop. Companies facing margin pressure from labour costs, corporation tax rising globally, logistics costs, input prices rising, energy costs, long-term interest rate costs starting to rise, difficulty trading generally (staff sick/isolating, logistics difficulties getting parts, selling outputs). Tax on individuals is also rising at the same time as e.g. long-term mortgage rates and general inflation. Inflation has generally been bad for stock price growth in real terms.

12. Fear and Greed index: https://money.cnn.com/data/fear-and-greed/

72/100: GREED. Showing 'extreme greed' and risk-taking on many metrics.

13. Greed & mania in individual stocks is widespread in the SP500.

https://finviz.com/map.ashx?t=sec&st=pe

https://finviz.com/map.ashx?t=sec&st=ps

14. TSLA price to earnings ratio around 360x. Eh. WTF. WTF!

15. Global logistics chaos and 10-20x higher costs not expected to clear until 2023.

16. Interest rate decisions this week from various central banks, talk of moving forward rate rises and tapering by many months from late 2022/2023 into 2021 or early 2022. Previous discontinuances of QE (tapering) has led to 'taper tantrum' stockmarket corrections.

17. Stimulus program in the USA to be far, far smaller than originally proposed.

18. Yield curve is flattening, yield curve inversion historically predicts recession. 20y treasury yield already inverted above 30y. (https://www.bloomberg.com/news/articles ... year-bonds)

Right now, it feels good to be mostly in short-term (1-3 year) government bonds.

Best of luck to those 100% long in the market, you will probably need it.

comp

2. Current PER SP500 estimated at 29, historical average around 15. https://www.multpl.com/s-p-500-pe-ratio

3. Current price/sales SP500 is 3.15x. Long term 1.5x.

4. [1-3] all suggest that if the market were to mean-revert right now the SP500 would lose 50% in real terms.

5. If the SP500 were to overshoot the mean to historical lows, we'd be looking at 80%+ drop in real terms.

6. Buffett ratio of total US market cap vs GDP at 213%, vs historical trend of 120%, i.e. 71% overvalued. Implying 44% drop to mean revert.

7. Household stockmarket holdings as % of portfolios is now equal to all time high of the dotcom era.

https://fred.stlouisfed.org/graph/?g=qis

8. 2-year government debt in Australia spiked from 0.1% to 0.8% in just one day last week, after the central bank decided not to defend against the market movement. Yikes. Potentially a big impact on fixed rate mortgages, short-term company debt costs if it doesn't drop back, or if we see this in other debt markets.

9. Property & construction are about 30% of the Chinese economy and are looking into a bad debt tsunami and new property tax. May impact some UK companies - HSBC, Standard Chartered, miners? May broadly impact world economy. Multiple large chinese property developers have defaulted on some debt or missed payments and are in pre-default.

10. Use of margin debt vs SP500 level is now at an all-time record high far above any past mania or bubble. This does not include growth in use of options which I understand to be very high and often combined with margin (and I'm told, funded by a credit card.... smh). Note that this metric is measured against the SP500 which itself is already at an all-time high. If you measure against something more stable during bubbles - e.g. GDP, or aggregate sales of the SP500 - this figure for use of margin will look completely off-the-chart insane. Finally note this chart is dated for September and the market has zoomed up even higher since then.

https://www.advisorperspectives.com/ima ... 59a77b.png

{kind=link}

11. Economic backdrop. Companies facing margin pressure from labour costs, corporation tax rising globally, logistics costs, input prices rising, energy costs, long-term interest rate costs starting to rise, difficulty trading generally (staff sick/isolating, logistics difficulties getting parts, selling outputs). Tax on individuals is also rising at the same time as e.g. long-term mortgage rates and general inflation. Inflation has generally been bad for stock price growth in real terms.

12. Fear and Greed index: https://money.cnn.com/data/fear-and-greed/

72/100: GREED. Showing 'extreme greed' and risk-taking on many metrics.

13. Greed & mania in individual stocks is widespread in the SP500.

https://finviz.com/map.ashx?t=sec&st=pe

https://finviz.com/map.ashx?t=sec&st=ps

14. TSLA price to earnings ratio around 360x. Eh. WTF. WTF!

15. Global logistics chaos and 10-20x higher costs not expected to clear until 2023.

16. Interest rate decisions this week from various central banks, talk of moving forward rate rises and tapering by many months from late 2022/2023 into 2021 or early 2022. Previous discontinuances of QE (tapering) has led to 'taper tantrum' stockmarket corrections.

17. Stimulus program in the USA to be far, far smaller than originally proposed.

18. Yield curve is flattening, yield curve inversion historically predicts recession. 20y treasury yield already inverted above 30y. (https://www.bloomberg.com/news/articles ... year-bonds)

Right now, it feels good to be mostly in short-term (1-3 year) government bonds.

Best of luck to those 100% long in the market, you will probably need it.

comp

-

GoSeigen

- Lemon Quarter

- Posts: 4406

- Joined: November 8th, 2016, 11:14 pm

- Has thanked: 1603 times

- Been thanked: 1593 times

Re: food for bears

compscidude wrote:16. Interest rate decisions this week from various central banks, talk of moving forward rate rises and tapering by many months from late 2022/2023 into 2021 or early 2022. Previous discontinuances of QE (tapering) has led to 'taper tantrum' stockmarket corrections.

ISTM that taper tantrum refers to the bond market reaction not stock market. In the past tapering has been bullish for stocks.

GS

-

dealtn

- Lemon Half

- Posts: 6091

- Joined: November 21st, 2016, 4:26 pm

- Has thanked: 442 times

- Been thanked: 2337 times

Re: food for bears

compscidude wrote:

8. 2-year government debt in Australia spiked from 0.1% to 0.8% in just one day last week, after the central bank decided not to defend against the market movement. Yikes. Potentially a big impact on fixed rate mortgages, short-term company debt costs if it doesn't drop back, or if we see this in other debt markets.

...

Right now, it feels good to be mostly in short-term (1-3 year) government bonds.

Really?

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

> Really?

Absolutely.

What kind of price movement do you see on a 2-year bond when the yield goes up 8x in a single day, from 0.1 to 0.8%?

Only 1.4%.

Consider, a whole-stockmarket daily move of 1.4% wouldn't raise an eyebrow on any world market.

The vast bulk of the 2-year's value is the return of capital, not the coupon.

Anyway, why am I in short-dated government bonds?

Basically, almost everything does badly when rates start to rise, and cash/short-term bonds do least badly.

Corp bonds? oh oh.

Long-dated treasuries? oh oh

Stocks? oh oh

Housing/real estate? oh oh

Why not just use cash then? (after all a 0% move surely beats a -1.4% move!)

Well, bonds are *negatively* correlated with the stockmarket. All things being equal they go in opposite directions mostly. This negative correlation, rather than simple diversification, is the principle behind e.g. 60-40 stock-bond funds. And if it takes a while to play out you get the coupon on a 2 year.

But cash is also an excellent choice if you think the market is toppy. Cash is a zero-coupon bond, after all.

Thanks for your query

comp

Absolutely.

What kind of price movement do you see on a 2-year bond when the yield goes up 8x in a single day, from 0.1 to 0.8%?

Only 1.4%.

Consider, a whole-stockmarket daily move of 1.4% wouldn't raise an eyebrow on any world market.

The vast bulk of the 2-year's value is the return of capital, not the coupon.

Anyway, why am I in short-dated government bonds?

Basically, almost everything does badly when rates start to rise, and cash/short-term bonds do least badly.

Corp bonds? oh oh.

Long-dated treasuries? oh oh

Stocks? oh oh

Housing/real estate? oh oh

Why not just use cash then? (after all a 0% move surely beats a -1.4% move!)

Well, bonds are *negatively* correlated with the stockmarket. All things being equal they go in opposite directions mostly. This negative correlation, rather than simple diversification, is the principle behind e.g. 60-40 stock-bond funds. And if it takes a while to play out you get the coupon on a 2 year.

But cash is also an excellent choice if you think the market is toppy. Cash is a zero-coupon bond, after all.

Thanks for your query

comp

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

> In the past tapering has been bullish for stocks.

No.

2013 taper tantrum

https://www.theguardian.com/business/20 ... t-sell-off

https://www.ftadviser.com/investments/2 ... r-tantrum/

2018 ECB tapering of QE in December 2018 & subsequent stockmarket correction.

https://edition.cnn.com/2018/12/31/inve ... index.html

2021 discussion e.g.

https://www.theguardian.com/business/ni ... very-story

"‘Taper tantrum’ by stock markets points to gaps in the easy recovery story"

https://www.ftadviser.com/investments/2 ... r-tantrum/

"In addition, the tapering of asset purchases may be viewed as the first step in a process of tightening the monetary conditions, culminating in higher interest rates, which would be expected to slow the economic growth rate, hurting the prospects of many equities and also causing bond prices to fall."

My own thoughts:

And of course there is no rational reason to believe that effective withdrawal of money from the market (e.g. extra supply of bonds as QE reverses, less demand for capital assets as QE ends/tapers) or alternatively, simply viewing it as no longer suppressing rates, would ever be positive for stocks.

DCF is discounted by interest rates, after all, and as you raise rates the DCF value of every single stock goes down.

No.

2013 taper tantrum

https://www.theguardian.com/business/20 ... t-sell-off

"Stock markets worldwide plummeted on Thursday, after the Federal Reserve chairman, Ben Bernanke, rattled investors by signalling an end to America's drastic recession-busting policy of quantitative easing."

https://www.ftadviser.com/investments/2 ... r-tantrum/

"In 2013, the response of the market to the first mention of tapering was a pronounced sell-off in equities and bonds."

2018 ECB tapering of QE in December 2018 & subsequent stockmarket correction.

https://edition.cnn.com/2018/12/31/inve ... index.html

"December was a particularly dreadful month: The S&P 500 was down 9% and the Dow was down 8.7% — the worst December since 1931. In one seven-day stretch, the Dow fell by 350 points or more six times. This year's Christmas Eve was the worst ever for the index."

2021 discussion e.g.

https://www.theguardian.com/business/ni ... very-story

"‘Taper tantrum’ by stock markets points to gaps in the easy recovery story"

https://www.ftadviser.com/investments/2 ... r-tantrum/

"In addition, the tapering of asset purchases may be viewed as the first step in a process of tightening the monetary conditions, culminating in higher interest rates, which would be expected to slow the economic growth rate, hurting the prospects of many equities and also causing bond prices to fall."

My own thoughts:

And of course there is no rational reason to believe that effective withdrawal of money from the market (e.g. extra supply of bonds as QE reverses, less demand for capital assets as QE ends/tapers) or alternatively, simply viewing it as no longer suppressing rates, would ever be positive for stocks.

DCF is discounted by interest rates, after all, and as you raise rates the DCF value of every single stock goes down.

Last edited by compscidude on November 2nd, 2021, 8:26 am, edited 1 time in total.

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

Following Monday's 10% rise in $TSLA (including 1% after hours), Tesla is now on a PER of roughly 392x vs. the broad long term market average of 14x and the current level of around 30x. This is mania. It will end badly for people buying in the last month (unless Elon issues a stack of new shares at these levels).

I note also that one of the cryptoscams that sprung up in October has just run off with all the money today (squidcoin). hehe. Imagine watching that show and not realising the probable outcome here.

I note also that one of the cryptoscams that sprung up in October has just run off with all the money today (squidcoin). hehe. Imagine watching that show and not realising the probable outcome here.

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

Another bear point:

Oil prices spiking upwards often lead to recessions soon after.

https://www.cnbc.com/2020/01/03/spiking ... -edge.html

Oil prices spiking upwards often lead to recessions soon after.

https://www.cnbc.com/2020/01/03/spiking ... -edge.html

-

TUK020

- Lemon Quarter

- Posts: 2042

- Joined: November 5th, 2016, 7:41 am

- Has thanked: 762 times

- Been thanked: 1178 times

Re: food for bears

compscidude wrote:

Right now, it feels good to be mostly in short-term (1-3 year) government bonds.

Best of luck to those 100% long in the market, you will probably need it.

comp

Thank you for alerting us how far out on the ledge we are.

Uncomfortable news, but good to be reminded of this from time to time.

Trying to divide my accounts into "might be needed in the near future" and "there for the long term", and increase the cash holding in the former

tuk020

-

odysseus2000

- Lemon Half

- Posts: 6428

- Joined: November 8th, 2016, 11:33 pm

- Has thanked: 1556 times

- Been thanked: 973 times

Re: food for bears

Over the last 20 years of the price of West Texas Intermediate crude, the current price is just above half way:

https://twitter.com/0_ody/status/145548 ... 40288?s=20

If the current COP climate talks in Glasgow do achieve anything it may include carbon taxes on oil usage which would tend to reduce oil demand as is the move to electric traction for road transport.

Regards,

https://twitter.com/0_ody/status/145548 ... 40288?s=20

If the current COP climate talks in Glasgow do achieve anything it may include carbon taxes on oil usage which would tend to reduce oil demand as is the move to electric traction for road transport.

Regards,

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

> Over the last 20 years of the price of West Texas Intermediate crude, the current price is just above half way:

Hello odysseus

Thanks for your reply

If you re-read my post (and the article), you'll see they both refer to the *rapid change upwards* in price causing recessions, not the absolute value.

For example, looking at your own link, a sudden jump upwards of similar size and speed to (2020-2021) took place starting early 2007.

What happened next?

That's my point. It *has* happened repeatedly in this way in history. The question is will it have the same effect this time as the previous times?

Hello odysseus

Thanks for your reply

If you re-read my post (and the article), you'll see they both refer to the *rapid change upwards* in price causing recessions, not the absolute value.

For example, looking at your own link, a sudden jump upwards of similar size and speed to (2020-2021) took place starting early 2007.

What happened next?

That's my point. It *has* happened repeatedly in this way in history. The question is will it have the same effect this time as the previous times?

-

GoSeigen

- Lemon Quarter

- Posts: 4406

- Joined: November 8th, 2016, 11:14 pm

- Has thanked: 1603 times

- Been thanked: 1593 times

Re: food for bears

compscidude wrote:> In the past tapering has been bullish for stocks.

No.

2013 taper tantrum

https://www.theguardian.com/business/20 ... t-sell-off"Stock markets worldwide plummeted on Thursday, after the Federal Reserve chairman, Ben Bernanke, rattled investors by signalling an end to America's drastic recession-busting policy of quantitative easing."

https://www.ftadviser.com/investments/2 ... r-tantrum/"In 2013, the response of the market to the first mention of tapering was a pronounced sell-off in equities and bonds."

2018 ECB tapering of QE in December 2018 & subsequent stockmarket correction.

https://edition.cnn.com/2018/12/31/inve ... index.html"December was a particularly dreadful month: The S&P 500 was down 9% and the Dow was down 8.7% — the worst December since 1931. In one seven-day stretch, the Dow fell by 350 points or more six times. This year's Christmas Eve was the worst ever for the index."

2021 discussion e.g.

https://www.theguardian.com/business/ni ... very-story

"‘Taper tantrum’ by stock markets points to gaps in the easy recovery story"

https://www.ftadviser.com/investments/2 ... r-tantrum/

"In addition, the tapering of asset purchases may be viewed as the first step in a process of tightening the monetary conditions, culminating in higher interest rates, which would be expected to slow the economic growth rate, hurting the prospects of many equities and also causing bond prices to fall."

My own thoughts:

And of course there is no rational reason to believe that effective withdrawal of money from the market (e.g. extra supply of bonds as QE reverses, less demand for capital assets as QE ends/tapers) or alternatively, simply viewing it as no longer suppressing rates, would ever be positive for stocks.

DCF is discounted by interest rates, after all, and as you raise rates the DCF value of every single stock goes down.

Withdrawal of money from the market as Comps describes it is profoundly bullish for stocks because it implies the economy is strong enough to generate inflation and warrant tightening of monetary policy. A strong economy is good for stocks, not bad.

Taper tantrum is what happened to bonds in 2013, not all the [rest] above. From the horse's mouth:

https://fredblog.stlouisfed.org/2021/08/no-taper-tantrum-this-time/

GS

Moderator Message:

Please try and remain polite. Telling a poster they are spewing forth nonsense certainly isn't. - Chris

Please try and remain polite. Telling a poster they are spewing forth nonsense certainly isn't. - Chris

-

odysseus2000

- Lemon Half

- Posts: 6428

- Joined: November 8th, 2016, 11:33 pm

- Has thanked: 1556 times

- Been thanked: 973 times

Re: food for bears

compsidude

Thanks for your reply

If you re-read my post (and the article), you'll see they both refer to the *rapid change upwards* in price causing recessions, not the absolute value.

For example, looking at your own link, a sudden jump upwards of similar size and speed to (2020-2021) took place starting early 2007.

What happened next?

That's my point. It *has* happened repeatedly in this way in history. The question is will it have the same effect this time as the previous times?

The big oil shocks of the 70s were massive price increases for hydrocarbons way beyond anything seen before, not moving around in a trading range.

In 2007 we were heading into the biggest financial crisis since the Great Depression. That was what mattered.

As of now we are in a global manipulation of markets by governments, the Great Reset. Meanwhile the human race is at war with carbon dioxide. Every politician doing his/her best to appear green and as in every war they are all spending like crazy. This is not the stuff of recessions, this is the stuff on the roaring 20's.

Regards,

-

TUK020

- Lemon Quarter

- Posts: 2042

- Joined: November 5th, 2016, 7:41 am

- Has thanked: 762 times

- Been thanked: 1178 times

Re: food for bears

GoSeigen wrote:Withdrawal of money from the market as Comps describes it is profoundly bullish for stocks because it implies the economy is strong enough to generate inflation and warrant tightening of monetary policy. A strong economy is good for stocks, not bad.

Taper tantrum is what happened to bonds in 2013, not all the [rest] above. From the horse's mouth:

https://fredblog.stlouisfed.org/2021/08/no-taper-tantrum-this-time/

GS

I thought the whole concept of stagflation was where inflation happened without the economic growth.

Is that not the danger we are facing now?

-

odysseus2000

- Lemon Half

- Posts: 6428

- Joined: November 8th, 2016, 11:33 pm

- Has thanked: 1556 times

- Been thanked: 973 times

Re: food for bears

TUK020 wrote:GoSeigen wrote:Withdrawal of money from the market as Comps describes it is profoundly bullish for stocks because it implies the economy is strong enough to generate inflation and warrant tightening of monetary policy. A strong economy is good for stocks, not bad.

Taper tantrum is what happened to bonds in 2013, not all the [rest] above. From the horse's mouth:

https://fredblog.stlouisfed.org/2021/08/no-taper-tantrum-this-time/

GS

I thought the whole concept of stagflation was where inflation happened without the economic growth.

Is that not the danger we are facing now?

We are at the cusp of at least two strong and powerful paradigm shifts that will impact the entire world:

1) Change to electric transport

2) AI

It is impossible to have stagflation in this environment.

Regards,

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

ody:

I respect that you have your own view on this. Impossible is a strong word, though, isn't it? And I don't think your view represents mainstream thought on this topic. Here are a few articles from the last few weeks.

Stagflation fears intensify in signs of slowing growth

The UK is at the sharp end of stagflationary concerns, with driver shortages compounding a surge in energy prices

https://www.ft.com/content/323f4d9f-016 ... 2c50c8d9a8

UK business confidence collapses as fears of ‘stagflation’ grow

Supply chain shortages and price rises could lead to the zero growth and high inflation seen in the 1970s

https://www.theguardian.com/business/20 ... ation-grow

Stagflation sensation

Is the world economy going back to the 1970s?

https://www.economist.com/finance-and-e ... s/21805260

Key Chinese manufacturing index shows signs of stagflation

https://www.dw.com/en/key-chinese-manuf ... a-59676606

Stagflation is coming: central banks and governments are right to be terrified

https://www.telegraph.co.uk/business/20 ... terrified/

The sequencing trap that risks stagflation 2.0

Today’s generation of central bankers is afflicted with the same sense of denial that proved problematic in the 1970s

https://www.ft.com/content/99eacd37-a2e ... c1ca7caa70

Supply chain crisis has central banks facing stagflation lite

https://www.bloomberg.com/news/features ... ation-lite

IMF to issue downbeat outlook as spectre of stagflation looms

https://www.theguardian.com/business/20 ... tion-looms

I hope this makes the case against your position thoroughly enough to merit a more detailed reply.

comp

paradigm shifts that will impact the entire world:

1) Change to electric transport

2) AI

It is impossible to have stagflation in this environment.

I respect that you have your own view on this. Impossible is a strong word, though, isn't it? And I don't think your view represents mainstream thought on this topic. Here are a few articles from the last few weeks.

Stagflation fears intensify in signs of slowing growth

The UK is at the sharp end of stagflationary concerns, with driver shortages compounding a surge in energy prices

https://www.ft.com/content/323f4d9f-016 ... 2c50c8d9a8

UK business confidence collapses as fears of ‘stagflation’ grow

Supply chain shortages and price rises could lead to the zero growth and high inflation seen in the 1970s

https://www.theguardian.com/business/20 ... ation-grow

Stagflation sensation

Is the world economy going back to the 1970s?

https://www.economist.com/finance-and-e ... s/21805260

Key Chinese manufacturing index shows signs of stagflation

https://www.dw.com/en/key-chinese-manuf ... a-59676606

Stagflation is coming: central banks and governments are right to be terrified

https://www.telegraph.co.uk/business/20 ... terrified/

The sequencing trap that risks stagflation 2.0

Today’s generation of central bankers is afflicted with the same sense of denial that proved problematic in the 1970s

https://www.ft.com/content/99eacd37-a2e ... c1ca7caa70

Supply chain crisis has central banks facing stagflation lite

https://www.bloomberg.com/news/features ... ation-lite

IMF to issue downbeat outlook as spectre of stagflation looms

https://www.theguardian.com/business/20 ... tion-looms

I hope this makes the case against your position thoroughly enough to merit a more detailed reply.

comp

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

ody:

And which have continued since. The spike from Q22020 to Q32021 (15 months) was from -$42 WTI to +$85 WTI.

That is a movement of $127.

How many examples of movements on that scale can you give me?

Which were followed by recessions?

And, taken from the low point of Q3 we still see a $50 rise in 12 months, and again: the same two questions.

Hoping to see precise facts and data in your reply, specific examples or counterexamples, not your intuition, if you don't mind.

The big oil shocks of the 70s were massive price increases for hydrocarbons way beyond anything seen before.

And which have continued since. The spike from Q22020 to Q32021 (15 months) was from -$42 WTI to +$85 WTI.

That is a movement of $127.

How many examples of movements on that scale can you give me?

Which were followed by recessions?

And, taken from the low point of Q3 we still see a $50 rise in 12 months, and again: the same two questions.

Hoping to see precise facts and data in your reply, specific examples or counterexamples, not your intuition, if you don't mind.

-

compscidude

- Lemon Pip

- Posts: 68

- Joined: November 6th, 2016, 10:07 pm

- Has thanked: 10 times

- Been thanked: 46 times

Re: food for bears

Goseigen, disregarding for the moment the completely unnecessary and inappropriate rudeness of your post,

As a matter of historical fact this is simply and provably not true. Fed tightening for example in the late 70s/early 80s in response to 'too much money / inflation' led rapidly to a famous bear market. This was absolutely not a vote of confidence in the economy by the fed. Sometimes, tightening is done since stimulus is no longer needed. Other times, it is done to prevent the patient dying from over-stimulus. Other times to avoid the risk of a situation where you are 'pushing on a string' and lose the tool of stimulus (i.e. Japanese Central Bank stimulus 1990s onwards, 'pushing on a string', 'liquidity traps').

Pushing on a string: https://www.investopedia.com/terms/p/pu ... string.asp

Liquidity trap: https://www.investopedia.com/terms/l/liquiditytrap.asp

Now, looking at 1981 as an example of central bank tightening, and 100% contrary to your claim:

https://www.forbes.com/sites/davidmarot ... t-of-1982/

Next example, 2018. European central bank tightening - voted for late June 2018, scheduled beginning Dec 2018 - (see https://www.reuters.com/article/us-euro ... SKBN1OB1SM) - led to a historically famous sharp 20% correction in stocks and various large market shocks, which I already pointed out, and you have simply ignored in your reply.

(In fact you simply ignored and did not directly address a single piece of data presented against you. Why aren't you responding directly to the various points I actually raise or facts I present? It's not a fair or reasonable way to discuss topics together if you simply pretend facts & history didn't happen, when people bring them up directly to counter your claims.)

=======

Responding to your FRED blog post. The blog post compares 2013 and 2021. It's appropriate to ask if Fed involvement in the market is comparable (the article appears to suggest the only relevant issue at play is 'talk of tapering').

Now, look at: https://www.federalreserve.gov/monetary ... trends.htm

This is also from the Fed. We can see that the aggregate intervention in the 6, 12, 18, 24 months preceding talk of tapering is significantly different - namely, far larger. The market is not 'free to move' in response to talk of tapering, as it is effectively pinned in place by a tsunami of money.

=======

Finally, my original post did not present the idea 'the market will go down due to talk of tapering'. Rather, it pointed to a tsunami of diverse issues unrelated to your reply except for a fraction of a sentence exclusively mentioned in point (16).

In short I have no idea why you are fighting a battle against an argument I didn't make, except in passing, as a fraction of a small fraction of my post.

Are you implicitly conceding that all the other 18-19 factors except for that sentence fragment are indeed looming over us in a scary beary manner?

In any event I have reported your post for its unnecessary rudeness and I invite you to repost without insults or trash talk and perhaps addressing more directly and thoroughly any of the posts I actually wrote.

comp

From the horse's mouth:

https://fredblog.stlouisfed.org/2021/08 ... this-time/

Withdrawal of money from the market as Comps describes it is profoundly bullish for stocks because it implies the economy is strong enough to generate inflation and warrant tightening of monetary policy.

As a matter of historical fact this is simply and provably not true. Fed tightening for example in the late 70s/early 80s in response to 'too much money / inflation' led rapidly to a famous bear market. This was absolutely not a vote of confidence in the economy by the fed. Sometimes, tightening is done since stimulus is no longer needed. Other times, it is done to prevent the patient dying from over-stimulus. Other times to avoid the risk of a situation where you are 'pushing on a string' and lose the tool of stimulus (i.e. Japanese Central Bank stimulus 1990s onwards, 'pushing on a string', 'liquidity traps').

Pushing on a string: https://www.investopedia.com/terms/p/pu ... string.asp

Liquidity trap: https://www.investopedia.com/terms/l/liquiditytrap.asp

Now, looking at 1981 as an example of central bank tightening, and 100% contrary to your claim:

https://www.forbes.com/sites/davidmarot ... t-of-1982/

With inflation running double digits the Federal Reserve under Volker raised the federal funds rate from 11.2% to 20% by June of 1981...This helped cause the 1980-1982 recession and a national unemployment rate of over 10%.

The S&P 500 bottomed 171 days later on August 12, 1982 at 102.42, down -27.11%.

Next example, 2018. European central bank tightening - voted for late June 2018, scheduled beginning Dec 2018 - (see https://www.reuters.com/article/us-euro ... SKBN1OB1SM) - led to a historically famous sharp 20% correction in stocks and various large market shocks, which I already pointed out, and you have simply ignored in your reply.

(In fact you simply ignored and did not directly address a single piece of data presented against you. Why aren't you responding directly to the various points I actually raise or facts I present? It's not a fair or reasonable way to discuss topics together if you simply pretend facts & history didn't happen, when people bring them up directly to counter your claims.)

The S&P 500 index peaked at 2930 on its September 20 close and dropped 19.73% to 2351 by Christmas Eve. Shanghai Composite dropped to a four-year low, escalating their economic downturn since the 2015 recession.

=======

Responding to your FRED blog post. The blog post compares 2013 and 2021. It's appropriate to ask if Fed involvement in the market is comparable (the article appears to suggest the only relevant issue at play is 'talk of tapering').

Now, look at: https://www.federalreserve.gov/monetary ... trends.htm

This is also from the Fed. We can see that the aggregate intervention in the 6, 12, 18, 24 months preceding talk of tapering is significantly different - namely, far larger. The market is not 'free to move' in response to talk of tapering, as it is effectively pinned in place by a tsunami of money.

=======

Finally, my original post did not present the idea 'the market will go down due to talk of tapering'. Rather, it pointed to a tsunami of diverse issues unrelated to your reply except for a fraction of a sentence exclusively mentioned in point (16).

In short I have no idea why you are fighting a battle against an argument I didn't make, except in passing, as a fraction of a small fraction of my post.

Are you implicitly conceding that all the other 18-19 factors except for that sentence fragment are indeed looming over us in a scary beary manner?

In any event I have reported your post for its unnecessary rudeness and I invite you to repost without insults or trash talk and perhaps addressing more directly and thoroughly any of the posts I actually wrote.

comp

Return to “Macro and Global Topics”

Who is online

Users browsing this forum: funduffer, Hallucigenia, PeterGray and 31 guests