I have come to consider my paid for home as an index linked (ish) bond paying the equivalent rent.

If you sell the house, what would you have to do?

W.

Got a credit card? use our Credit Card & Finance Calculators

Thanks to eyeball08,Wondergirly,bofh,johnstevens77,Bhoddhisatva, for Donating to support the site

Portfolio diversification & ITs

-

1nvest

- Lemon Quarter

- Posts: 4411

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1343 times

Re: Portfolio diversification & ITs

JohnW wrote:1nvest wrote:Diversification is more for risk reduction purposes. For some just three or four stocks might suffice. For example consider a investor who follows a Talmud advocated style asset allocation, third each :

land (UK home (£))

Is it right to consider your home an investment? You usually can't sub-divide the land to sell a corner to realise some cash; you can't sell it all without needing to replace it, or rent; but you can rent out the front room for a very modest return.

I'm not sure that counting it adds much to your diversification unless you plan to sell and move to a much lower cost country.

It's part of net wealth. When perceived as £ exposure, along with US stock $ and gold global currency then its a indicator for rebalancing between those currencies. For liquidity holding a UK REIT as part of 'UK land' exposure can suffice, but given the tendency for REIT's to correlate with stocks a UK stock fund could also be considered appropriate IMO. For instance £250K home value, £83K UK stock ... as the combined £ exposure, £333K of US stock, £333K of gold.

If your London home was bombed/destroyed during WW2 I suspect that it was a uninsured 'act of war' loss. The land value would still have been available so a a 16% type loss perhaps if the home value was third of net wealth and the land value was half of the total value.

Also often with rebalancing you may not actually have to rebalance in practice that often. During accumulation adding savings to the least value asset/during drawdown spending from the highest valued asset, along with dividends adding/supplementing that, and fundamentally you're comparing house price only/gold/stock price only levels, which each/all of those might broadly pace inflation - and where house value provides imputed rent benefit on top, stocks provide dividends on top, gold provides trading (rebalance) benefits on top, and that broadly all compare equally. If dividends or imputed rent or trading/volatility rewards were consistently different then investors would converge on the most rewarding. That isn't the case hence we have some that seek price appreciation, others that target income, yet others that target volatility (such as Traded Options traders).

-

JohnW

- Lemon Slice

- Posts: 517

- Joined: June 1st, 2019, 7:00 am

- Has thanked: 5 times

- Been thanked: 185 times

Re: Portfolio diversification & ITs

I agree that's a reasonable view. Just a big difference in being able to sell some of the bond fund but not some of the house, and maintenance costs.

Your own house saves you rent paying, so really it reduces your need for investments to fund your retirement, rather than having some of the characteristics of a typical investment.

Your own house saves you rent paying, so really it reduces your need for investments to fund your retirement, rather than having some of the characteristics of a typical investment.

-

1nvest

- Lemon Quarter

- Posts: 4411

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1343 times

Re: Portfolio diversification & ITs

Wuffle wrote:I have come to consider my paid for home as an index linked (ish) bond paying the equivalent rent.

If you sell the house, what would you have to do?

W.

Liability matching rent is a lot safer than not. Selling a home to rent instead and the risks are that rents could spike significantly at a time when investments had declined a lot - such as might occur over a period of rising interest rates/inflation. Being in effect both landlord and tenant and its pretty much irrelevant if landlords are winning/renters losing or vice-versa.

-

1nvest

- Lemon Quarter

- Posts: 4411

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1343 times

Re: Portfolio diversification & ITs

Fundamentally much of investing is about currency risk. For centuries money was backed by something finite and tangible - gold. Broadly there was equal measure of both inflation and deflation such that overall it averaged 0% inflation. When money was exchangeable for gold at a fixed rate it made more sense to hold money that you lent to the state (bought Gilts), that paid interest, as then that was like the state paying you in order for it to securely store your gold. You could spend the interest, and still see the same number of ounces of gold being preserved, or left interest to accumulate and end up with more ounces of gold.

From 1931 the coupling between money and gold was broken (in the UK) and others followed, with the US ending their coupling to the US Dollar starting in 1968, ending in 1971. Since then the US $ has declined relative to gold, massively so, at around a 7% annualised rate. Whilst the Pound has declined relative to the dollar, so declining around 9%/year relative to gold. But not in a nice linear/steady manner, but instead in a sporadic/volatile manner. Holding £, $ and global currency (gold) and rebalancing between them has been a means to bolster rewards. viewtopic.php?p=329934#p329934

If you opt for a third in each of those global (gold), primary reserve (US$) and domestic (£) currencies, then for the £'s and $'s you have to invest them somewhere, and it seems reasonable/logical for a UK domiciled investor to have £'s in UK land and $'s in stocks. Unless perhaps you tended to travel/live between the UK and US in which case you might have a property in both countries and own some shares in both countries, in around equal measure.

From 1931 the coupling between money and gold was broken (in the UK) and others followed, with the US ending their coupling to the US Dollar starting in 1968, ending in 1971. Since then the US $ has declined relative to gold, massively so, at around a 7% annualised rate. Whilst the Pound has declined relative to the dollar, so declining around 9%/year relative to gold. But not in a nice linear/steady manner, but instead in a sporadic/volatile manner. Holding £, $ and global currency (gold) and rebalancing between them has been a means to bolster rewards. viewtopic.php?p=329934#p329934

£1 invested in stock accumulation at the start of 1972 would have been £180 value at the end of 2019

£1 invested in gold at the start of 1972 would have been £80 value at the end of 2019

50/50 of both initially, bought and held would be valued at £130 at the end of 2019

50/50 yearly rebalanced and the value would have been £240 at the end of 2019. You'd be holding 33% more shares than at the start, and 3 times as many ounces of gold as at the start.

If you opt for a third in each of those global (gold), primary reserve (US$) and domestic (£) currencies, then for the £'s and $'s you have to invest them somewhere, and it seems reasonable/logical for a UK domiciled investor to have £'s in UK land and $'s in stocks. Unless perhaps you tended to travel/live between the UK and US in which case you might have a property in both countries and own some shares in both countries, in around equal measure.

Re: Portfolio diversification & ITs

I bought my one and only house in 2005.

Peak value of property vs gold.

You have to laugh.

(The OH fancied some jewellery a few years ago and had a couple of pieces made up in the jewellery Quarter in Brum in palladium on the jeweler recommendation. She hadn't heard of it.

You have to laugh).

Just to make an effort to stay on topic I like MYI, HINT for non UK stock diversification and at least an eye on value (less USA).

I get tempted to add region specific bits and bobs but probably ought to just leave them to it.

W.

Peak value of property vs gold.

You have to laugh.

(The OH fancied some jewellery a few years ago and had a couple of pieces made up in the jewellery Quarter in Brum in palladium on the jeweler recommendation. She hadn't heard of it.

You have to laugh).

Just to make an effort to stay on topic I like MYI, HINT for non UK stock diversification and at least an eye on value (less USA).

I get tempted to add region specific bits and bobs but probably ought to just leave them to it.

W.

-

1nvest

- Lemon Quarter

- Posts: 4411

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1343 times

Re: Portfolio diversification & ITs

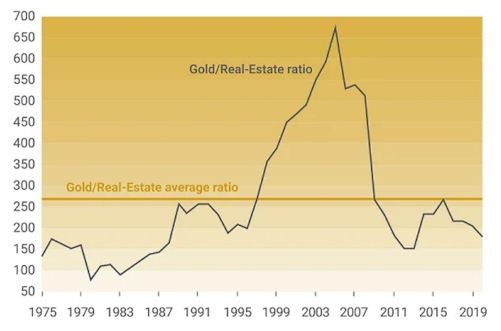

Wuffle wrote:I bought my one and only house in 2005.

Peak value of property vs gold.

UK gold/house ratio

suggests that the 700 ounces of gold it took to buy a house in/around that time, required only 150 ounces in/around 2013/2014. If the seller to you had held gold for those years, they'd have been able to buy nearly 5 times as many houses back again.

US Dow/Gold swung from around 1.3 ounces of gold required to buy the Dow in 1980 up to the Dow buying 44 ounces in the early 2000's

Nice if you have a crystal ball to know exactly when to rotate fully into individual assets, but in the absence of that, holding a third in each of stock, gold and home value along with yearly rebalancing will still capture a decent chunk of the benefits. 1980 to 2000 for instance 50/50 stock/gold saw 6 to 10 times more ounces of gold being held at the end of that period, and since the 2000's those ounces of gold have seen distinct increases in purchase power of other assets.

But many avoid gold, on the basis that a 1 ounce gold coin might have bought a Roman soldier a suit, as equally as it might buy a modern day man a suit - just broadly paces inflation. The oversight there however is that trading gold can yield distinct dividends over time. The cycles however are relatively long, can span decades. And when stocks are zigging (upward), the regrets of holding and increasing gold ounces that are progressively downwards in price tends to lead to capitulation to instead profit chase stocks, likely at the worst possible time.

-

1nvest

- Lemon Quarter

- Posts: 4411

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1343 times

Re: Portfolio diversification & ITs

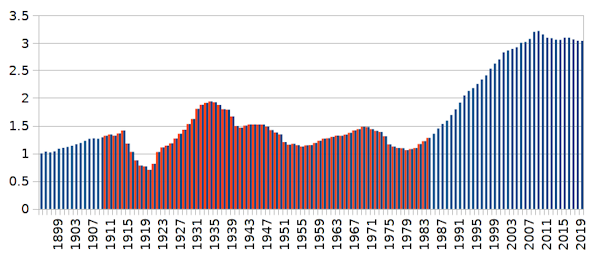

Between 1980 and 1999 it didn't really matter what you invested in, stocks or bonds did exceptionally well. Studies that utilise back-tests that span that period will be distorted by that. For example stocks made massive gains, getting on for 19% annualised type reward in the UK. Similar to the 17% in the US (the difference being down to the £'s relative decline compared to the US$)

As this chart indicates, even UK T-Bills (short term Gilts) increased by around three-fold over the 1980 to early 2000's in after inflation (real) terms.

So I got to wondering about relative performance over a more neutral period, and came up with 1910 to 1984 years (inclusive), where broadly T-Bills overall sideways traded, ended at around the same inflation adjusted value as at the start, and that yearly averaged around the broader overall average. In other words were broadly flat in inflation adjusted terms (albeit with volatility along the way).

As part of that I was led to a interesting article https://portfoliocharts.com/2015/11/17/ ... ates-work/ that indicates for those in drawdown, after factoring in such things as start date valuations, volatility ...etc. that broadly it didn't make much difference in the worst case whether you were stock heavy/bond light or bond heavy/stock light. But where perhaps in the average case stock-heavy yielded the higher average/best case outcomes. But where that is including the exceptional 1980 to 2000 period.

The mid 1960's to mid 1980's were a terrible time for stocks when in drawdown mode. Total returns before costs and taxes barely paced inflation such that any withdrawal (and paying taxes) were eating capital. Again the above chart indicates that T-Bills were also relatively poor, declining by around a third.

For those accumulating, increasingly lower prices as savings grow is great. On the flip side, for those in retirement increasing prices are great. For a investor who started accumulating liquid assets in the early 1970's, perhaps after earlier decades of having been predominately paying down a mortgage, and where they retired in/around 1980, then the conditions were near ideal. Perhaps a teacher (striving to fit a real world example) that was 50 in 1970 and had just paid off their house and started accumulating stocks/bonds and then retired at age 60 in 1980 (born 1920).

On the flip side it could prove that those that were accumulating from 1980, that were near or recently into retirement, it could very well be a case of their portfolio value declining in real total return terms, along with also being depended upon the portfolio to provide a income/drawdown. Putting all eggs into a single basket, such as stocks, or bonds, or maybe a combination of both, might not work as desired.

Perhaps too much emphasis is being placed on the assumption that stocks and/or bonds are the 'better' choice of assets. That at relatively high recent valuations wealth preservation and liability matching may prove to be the better choice. i.e. broader diversification. Perhaps some stock, some bonds, some gold, some inflation bonds, along with owning your own home so 'rent' is liability matched.

My thoughts are along the lines of perhaps owning a home alongside a Permanent Portfolio, but where the long dated bonds are held in Inflation Bonds (Index Linked Gilts) instead of conventional bonds may be better placed asset allocation for things to come.

Looking at the longer dated Index Link Gilts price motion compared to conventional Gilt price motion suggests broader similarities. Yes it seems crazy to buy into something that yields -2.4%/year type cost, but diluted down in being just 25% of the total portfolio value = 0.6%/year. Which might be considered as a form of portfolio insurance cost. That's less than what some pay in fund/IT 'management fees'

Unlike conventional bonds, where prices increase as nominal yields decline, prices decrease as nominal yields rise, with ILG's prices increase as real yields decline and decrease as real yields rise. If/when inflation rises so real yields will tend to increase, and see lower ILG prices, but more being received via higher inflation. If however the broader trend is for negative real yields, such as T-Bills losing value relative to inflation, then so ILG's will see even higher prices. What seems relatively expensive today could with hindsight been fair/cheap later.

Stocks to some extent are a form of undated variable coupon conventional bond.

Chuck out bonds altogether and a asset allocation of owning a home, some stock some gold ... is perhaps reasonable enough diversity for forward time (from current valuations). And backtesting that over the 1910 to 1984 'flat' years (with caveats that I wont detail here) indicates that did provide reasonable results. And held up better during 'down' (negative/declining real T-Bill) periods.

Gold might be considered as a even longer dated Index Linked Gilt, a undated zero coupon form of ILG.

I envy the likes of Warren Buffet and our local Terry (TJH) who seemingly lived through near ideal times for their age. Personally I'm more at the other end, just coming up to retirement, more a case of perhaps the perfect storm and where asset diversification more focused towards wealth preservation and assuming capital drawdown to service retirement income will become the 'norm' for that era and those that go with current 'traditional' asset allocations may suffer. On the plus side I'm blessed with a reasonable inflation linked occupational pension unlike those that the younger generation will benefit from. And for my sons in just starting out on their working life perhaps they'll be more inclined to see a repeat of their grandads generation of potentially accumulating stocks are relatively low price levels over time.

For me, now 'single' with two adult kids, a soon to be payable occupational pension at age 60, along with £10K/year x 7 years amount to cover (drawdown) until the £9K state pension also kicks in is enough for my lifestyle (given no more uni fees to cover etc.). A Permanent Portfolio for that £70K seems appropriate/reasonable. £22K to £25K/year disposable income type lifestyle. Own own home so no finding/paying rent issues. Which leaves a substantial amount that most likely will be passed over to the kids. If valuations/circumstances were lower/better I'd be more inclined to all-stock that for them. In the opinion however that both stocks and bond may struggle and that cost averaging in may prove to be the better, I'm more inclined to set them up with their own homes leaving them better placed to accumulate stocks over time out of new money (wages/savings) and for the remainder of liquid wealth holding a 50/50 stock/gold asset allocation. Writing off the Permanent Portfolio/drawdown amount, that would have family wealth at around 75% home values, 12.5% in each of stock and gold. Whilst I could envisage that 75% losing half or more, its a consumption asset, doesn't really matter, other than my own home value perhaps being called upon for twilight life care fees cover. Another option is to direct to home value being around 25%, and the rest in a Permanent Portfolio. Seeing the forecast by this Australian based version (that charges a whopping fee - so most certainly not a recommendation) https://corcapital.com.au/fund-fact-sheet/

along with "3% to 5% real gains for money you can't afford to lose" ... type claims against the PP, the 25% home/75% PP (broader diversification than stock/bonds) has considerable appeal.

As this chart indicates, even UK T-Bills (short term Gilts) increased by around three-fold over the 1980 to early 2000's in after inflation (real) terms.

So I got to wondering about relative performance over a more neutral period, and came up with 1910 to 1984 years (inclusive), where broadly T-Bills overall sideways traded, ended at around the same inflation adjusted value as at the start, and that yearly averaged around the broader overall average. In other words were broadly flat in inflation adjusted terms (albeit with volatility along the way).

As part of that I was led to a interesting article https://portfoliocharts.com/2015/11/17/ ... ates-work/ that indicates for those in drawdown, after factoring in such things as start date valuations, volatility ...etc. that broadly it didn't make much difference in the worst case whether you were stock heavy/bond light or bond heavy/stock light. But where perhaps in the average case stock-heavy yielded the higher average/best case outcomes. But where that is including the exceptional 1980 to 2000 period.

The mid 1960's to mid 1980's were a terrible time for stocks when in drawdown mode. Total returns before costs and taxes barely paced inflation such that any withdrawal (and paying taxes) were eating capital. Again the above chart indicates that T-Bills were also relatively poor, declining by around a third.

For those accumulating, increasingly lower prices as savings grow is great. On the flip side, for those in retirement increasing prices are great. For a investor who started accumulating liquid assets in the early 1970's, perhaps after earlier decades of having been predominately paying down a mortgage, and where they retired in/around 1980, then the conditions were near ideal. Perhaps a teacher (striving to fit a real world example) that was 50 in 1970 and had just paid off their house and started accumulating stocks/bonds and then retired at age 60 in 1980 (born 1920).

On the flip side it could prove that those that were accumulating from 1980, that were near or recently into retirement, it could very well be a case of their portfolio value declining in real total return terms, along with also being depended upon the portfolio to provide a income/drawdown. Putting all eggs into a single basket, such as stocks, or bonds, or maybe a combination of both, might not work as desired.

Perhaps too much emphasis is being placed on the assumption that stocks and/or bonds are the 'better' choice of assets. That at relatively high recent valuations wealth preservation and liability matching may prove to be the better choice. i.e. broader diversification. Perhaps some stock, some bonds, some gold, some inflation bonds, along with owning your own home so 'rent' is liability matched.

My thoughts are along the lines of perhaps owning a home alongside a Permanent Portfolio, but where the long dated bonds are held in Inflation Bonds (Index Linked Gilts) instead of conventional bonds may be better placed asset allocation for things to come.

Looking at the longer dated Index Link Gilts price motion compared to conventional Gilt price motion suggests broader similarities. Yes it seems crazy to buy into something that yields -2.4%/year type cost, but diluted down in being just 25% of the total portfolio value = 0.6%/year. Which might be considered as a form of portfolio insurance cost. That's less than what some pay in fund/IT 'management fees'

Unlike conventional bonds, where prices increase as nominal yields decline, prices decrease as nominal yields rise, with ILG's prices increase as real yields decline and decrease as real yields rise. If/when inflation rises so real yields will tend to increase, and see lower ILG prices, but more being received via higher inflation. If however the broader trend is for negative real yields, such as T-Bills losing value relative to inflation, then so ILG's will see even higher prices. What seems relatively expensive today could with hindsight been fair/cheap later.

Stocks to some extent are a form of undated variable coupon conventional bond.

Chuck out bonds altogether and a asset allocation of owning a home, some stock some gold ... is perhaps reasonable enough diversity for forward time (from current valuations). And backtesting that over the 1910 to 1984 'flat' years (with caveats that I wont detail here) indicates that did provide reasonable results. And held up better during 'down' (negative/declining real T-Bill) periods.

Gold might be considered as a even longer dated Index Linked Gilt, a undated zero coupon form of ILG.

I envy the likes of Warren Buffet and our local Terry (TJH) who seemingly lived through near ideal times for their age. Personally I'm more at the other end, just coming up to retirement, more a case of perhaps the perfect storm and where asset diversification more focused towards wealth preservation and assuming capital drawdown to service retirement income will become the 'norm' for that era and those that go with current 'traditional' asset allocations may suffer. On the plus side I'm blessed with a reasonable inflation linked occupational pension unlike those that the younger generation will benefit from. And for my sons in just starting out on their working life perhaps they'll be more inclined to see a repeat of their grandads generation of potentially accumulating stocks are relatively low price levels over time.

For me, now 'single' with two adult kids, a soon to be payable occupational pension at age 60, along with £10K/year x 7 years amount to cover (drawdown) until the £9K state pension also kicks in is enough for my lifestyle (given no more uni fees to cover etc.). A Permanent Portfolio for that £70K seems appropriate/reasonable. £22K to £25K/year disposable income type lifestyle. Own own home so no finding/paying rent issues. Which leaves a substantial amount that most likely will be passed over to the kids. If valuations/circumstances were lower/better I'd be more inclined to all-stock that for them. In the opinion however that both stocks and bond may struggle and that cost averaging in may prove to be the better, I'm more inclined to set them up with their own homes leaving them better placed to accumulate stocks over time out of new money (wages/savings) and for the remainder of liquid wealth holding a 50/50 stock/gold asset allocation. Writing off the Permanent Portfolio/drawdown amount, that would have family wealth at around 75% home values, 12.5% in each of stock and gold. Whilst I could envisage that 75% losing half or more, its a consumption asset, doesn't really matter, other than my own home value perhaps being called upon for twilight life care fees cover. Another option is to direct to home value being around 25%, and the rest in a Permanent Portfolio. Seeing the forecast by this Australian based version (that charges a whopping fee - so most certainly not a recommendation) https://corcapital.com.au/fund-fact-sheet/

Maximise return above change in CPI over 3 year periods without generating a negative return over any 12 month period

along with "3% to 5% real gains for money you can't afford to lose" ... type claims against the PP, the 25% home/75% PP (broader diversification than stock/bonds) has considerable appeal.

-

Bouleversee

- Lemon Quarter

- Posts: 4654

- Joined: November 8th, 2016, 5:01 pm

- Has thanked: 1195 times

- Been thanked: 903 times

Re: Portfolio diversification & ITs

I certainly think the best thing one can do is to help one's children to own a decent house, with as little mortgage as possible. My son, with very little income being self-employed in the travel trade, is certainly glad he has no mortgage to feed. However, an article in yesterday's Sunday Times ("Cash tills shut at Bank of Mum and Dad", which you should be able to get if you Google the heading) says that Nationwide are restricting parental contributions: "Buyers seeking lower deposit mortgages will need to prove that at least three-quarters of the cash they put down has come from their own savings." I don't know what happens if buyers are making large deposits. It doesn't make much sense anyway. What about savings deriving from parental gifts made over several years, inheritances from grandparents etc? How much savings from earnings do they think young people paying rent can make? If they are worried they will borrow more than they can service, they could always ask for a parental guarantee.

-

Arborbridge

- The full Lemon

- Posts: 10439

- Joined: November 4th, 2016, 9:33 am

- Has thanked: 3642 times

- Been thanked: 5272 times

Re: Portfolio diversification & ITs

Bouleversee wrote:I certainly think the best thing one can do is to help one's children to own a decent house, with as little mortgage as possible. My son, with very little income being self-employed in the travel trade, is certainly glad he has no mortgage to feed. However, an article in yesterday's Sunday Times ("Cash tills shut at Bank of Mum and Dad", which you should be able to get if you Google the heading) says that Nationwide are restricting parental contributions: "Buyers seeking lower deposit mortgages will need to prove that at least three-quarters of the cash they put down has come from their own savings." I don't know what happens if buyers are making large deposits. It doesn't make much sense anyway. What about savings deriving from parental gifts made over several years, inheritances from grandparents etc? How much savings from earnings do they think young people paying rent can make? If they are worried they will borrow more than they can service, they could always ask for a parental guarantee.

I heard on the Beeb that inheritance does not count: it is your own money. Why this does not apply to money given by parents, one would have to get Nationwide to explain - but they think it's different.

I guess they argue that savings demonstrate how much spare income you have, whereas money recently given doesn't - therefore their risk is different.

Ooh, sorry just realised this is OT - I forgot which thread I was on - hopefully it can stand.

Arb.

-

tjh290633

- Lemon Half

- Posts: 8267

- Joined: November 4th, 2016, 11:20 am

- Has thanked: 919 times

- Been thanked: 4130 times

Re: Portfolio diversification & ITs

Bouleversee wrote:I certainly think the best thing one can do is to help one's children to own a decent house, with as little mortgage as possible. My son, with very little income being self-employed in the travel trade, is certainly glad he has no mortgage to feed. However, an article in yesterday's Sunday Times ("Cash tills shut at Bank of Mum and Dad", which you should be able to get if you Google the heading) says that Nationwide are restricting parental contributions: "Buyers seeking lower deposit mortgages will need to prove that at least three-quarters of the cash they put down has come from their own savings." I don't know what happens if buyers are making large deposits. It doesn't make much sense anyway. What about savings deriving from parental gifts made over several years, inheritances from grandparents etc? How much savings from earnings do they think young people paying rent can make? If they are worried they will borrow more than they can service, they could always ask for a parental guarantee.

In our family it has been the grandparents who have helped our offspring onto the property ladder. Their last grandmother died just about the right time to provide deposits for their respective houses.

Back in 1961, when I bought our first house, the general rule seemed to be that you should save about the amount you would have to pay in a mortgage for a year before taking the mortgage out. My first mortgage cost me £11/10/0d or thereabouts each month. That would have saved about £135 in a year, interest being about 5% at the time. That, of course, is 5% of £2,700 which is approximately what that first house cost. Ideally you limited your mortgage to about 80%, which implies 4 years' saving or making higher monthly deposits. Our deposit was nearly 40%, on account of living with my in-laws for 3 years.

Perhaps the moral is that young people should not pay fancy rents before they own their own property.

TJH

-

Bouleversee

- Lemon Quarter

- Posts: 4654

- Joined: November 8th, 2016, 5:01 pm

- Has thanked: 1195 times

- Been thanked: 903 times

Re: Portfolio diversification & ITs

tjh290633 wrote:Bouleversee wrote:I certainly think the best thing one can do is to help one's children to own a decent house, with as little mortgage as possible. My son, with very little income being self-employed in the travel trade, is certainly glad he has no mortgage to feed. However, an article in yesterday's Sunday Times ("Cash tills shut at Bank of Mum and Dad", which you should be able to get if you Google the heading) says that Nationwide are restricting parental contributions: "Buyers seeking lower deposit mortgages will need to prove that at least three-quarters of the cash they put down has come from their own savings." I don't know what happens if buyers are making large deposits. It doesn't make much sense anyway. What about savings deriving from parental gifts made over several years, inheritances from grandparents etc? How much savings from earnings do they think young people paying rent can make? If they are worried they will borrow more than they can service, they could always ask for a parental guarantee.

In our family it has been the grandparents who have helped our offspring onto the property ladder. Their last grandmother died just about the right time to provide deposits for their respective houses.

Back in 1961, when I bought our first house, the general rule seemed to be that you should save about the amount you would have to pay in a mortgage for a year before taking the mortgage out. My first mortgage cost me £11/10/0d or thereabouts each month. That would have saved about £135 in a year, interest being about 5% at the time. That, of course, is 5% of £2,700 which is approximately what that first house cost. Ideally you limited your mortgage to about 80%, which implies 4 years' saving or making higher monthly deposits. Our deposit was nearly 40%, on account of living with my in-laws for 3 years.

Perhaps the moral is that young people should not pay fancy rents before they own their own property.

TJH

I don't think they do pay fancy rents if they can help it. Mine lived at home till they bought but then you have expensive rail fares. We used to invest for them and then did the same when we had grandchildren. The four grandchildren have shareholdings in bare trusts which were amounting to a useful sum pre Covid-19. That wouldn't go very far in the property market accessible to London now, however, and the first one is about to go to university so none in a position to get a mortgage and take advantage of the reduction in stamp duty. It remains to be seen how many of those holdings will still be there when needed and whether their prices will recover. I don't think many are producing dividends, though 3 cheers for Tate & Lyle.

-

jonesa1

- Lemon Slice

- Posts: 263

- Joined: May 27th, 2019, 9:47 am

- Has thanked: 103 times

- Been thanked: 142 times

Re: Portfolio diversification & ITs

Bouleversee wrote:

I don't think they do pay fancy rents if they can help it. Mine lived at home till they bought but then you have expensive rail fares. We used to invest for them and then did the same when we had grandchildren. The four grandchildren have shareholdings in bare trusts which were amounting to a useful sum pre Covid-19. That wouldn't go very far in the property market accessible to London now, however, and the first one is about to go to university so none in a position to get a mortgage and take advantage of the reduction in stamp duty. It remains to be seen how many of those holdings will still be there when needed and whether their prices will recover. I don't think many are producing dividends, though 3 cheers for Tate & Lyle.

Both my daughters have moved to London and pay pretty expensive rents. In part this was a choice to live somewhere rather more lively (at least it was before March this year) than their home town, but in larger part it was about going where they could find work. One daughter will be moving back home (temporarily) when her lease expires, now that she's able to work from home and a lot of the attraction of living in London has been suspended - it will also allow her to save some money. The reduction in demand for flats already seems to be feeding through to lower rents, it will be interesting to see if this is a long term change.

Return to “Investment Strategies”

Who is online

Users browsing this forum: No registered users and 27 guests