hiriskpaul wrote:TahiPanasDua wrote:A couple of snippets: a simple 60/40 stocks/bonds portfolio underperformed the S&P 500 alone by over 250% cumulatively over the past 25 years. The author claims the cure is worse than the disease often with hidden costs. Interventions against looming market crashes ultimately lead to lower compound returns than those crashes would have cost them. Markets have scared us far more than they have harmed us.

I have not found the article, but I really don't find these observations particularly illuminating. Take more risk (compensated risk) and you can expect a higher return and most of the time,

but not all of the time, that is what will happen.

Retirement years drawdown presents a great risk. A bad decade of negative total returns compounded with also drawing income can draw down the portfolio value to unrecoverable lows, potentially relatively quickly (handful of years). History is littered with those who bought into stocks, did well, hit a bad era and ended up capitulating such that they would have been better served if they'd just held T-Bills throughout. The average investor on average underperforms the 'average' by 2% annualised, greed/fear, bad behaviour can result in substantial risk exposure for very poor overall rewards/outcome.

Playing with the stock market is like playing chicken with a freight train... no matter how many times you win, you only get to lose once. -Mike Masters

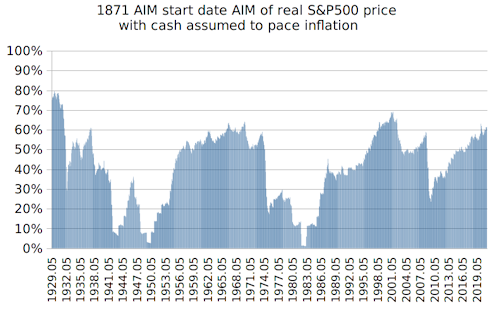

Taking the opposite stance can be highly rewarding. Mostly 'safe' but dipping in (and out) at opportune times can yield fantastic overall rewards. 25% annualised real type rewards over 20 year 'dipped-in' periods. Rather than running with constant fear of large declines, looking instead for there to be 'blood on the streets' as potentially highly rewarding opportunities.

In the 19th century investing was conceptually easy, money and gold were pegged, broadly there was no inflation, but with periods of clustered high inflation/deflation being the primary risk. The state paid you a decent real returns i.e. it made more sense to hold money deposited and earning interest than gold, as that bought back more gold as and when each T-Bill matured.

Following the collapse of the British Empire and transition over to the US$ as the primary reserve currency that benefit vanished. However a reasonable transition would have been over to a third each in £, $ and gold (or silver). With the currencies deposited into their respective T-Bills that still yielded a broad 2% real, enough such that a 4% SWR would see you through 30+ years, 3% would still have around half as much inflation adjusted capital remaining at the end of 30 years, 2% SWR would see 90% still intact after 30 years. But that ignores taxation risk, which tends to rise as/when inflation/interest rates spike. A more tax efficient alternative might have been to hold US$ invested in US stocks. That 'safe' choice combined with going heavily into opportunities as/when they presented (and later back out again) and rewards could have been bolstered significantly, higher overall actual real gains than all-stock, with considerably less risk.

Even without opportunistic dipping in/out, for all 30 year periods since the 1930's (yearly granularity), UK gilts, US stock, gold third each yearly rebalanced with a 3% SWR would on average seen more inflation adjusted capital available at the end of the 30 years than at the start. In the worst case 30 years only a modest decline. Partnered with dipping in/out at opportune times and the overall rewards on average would have exceeded that of a successful all-stocker.

Safe of ...

£ domestic, US$ primary reserve, and global currency gold currency diversification

Bonds, stocks, commodity asset diversification

Dive in when there's blood on the streets, revert back to 'safe' again when broad extreme greed is again apparent.

3% SWR if the intent is to leave some for heirs, otherwise 4% SWR. Regular/reliable inflation adjusted income stream. More often the residual portfolio value will see reasonable gains that support additional periodic discretionary withdrawals.

Bad 1970's where a 3% SWR was being applied saw the capital value of the residual having risen 7% annualised by 1980. The stock lows/gold high of 1980 when the Dow/Gold ratio was at near 1.0 levels and a transition over to all-stock and by the late 1990's when the Dow/Gold had risen to over 40 levels provided great gains. Rotation back during the 1990's into 'safe' and rewards to recent have still be reasonable and bad years seeing relatively light losses despite all of the dot com, financial and Covid crises. Rotating into stocks from 'safe' at each/any of those dips would have seen great subsequent 'rebound' rewards.

{kind=link}