vand wrote:The irony of a 100% equity portfolio is that it doesn't improve safe withdrawals rates at all - so if you are holding cash because you aren't confident that you portfolio will survive a deep bear market or is susceptible to sequence risk, properly adjusting your asset mix is the better strategy. If you want to enjoy your money rather than continually worrying about the next bear market, I have, for a while, been saying that 70/20/10 stocks/bonds/gold is a very good starting point.

+1 but without the bonds. Bonds and cash deposits are loans, often where the borrower gets to set/change the rules, and pay relatively little. I see occupational+state pensions as a inflation bond ladder, that is fully exhausted the day you die.

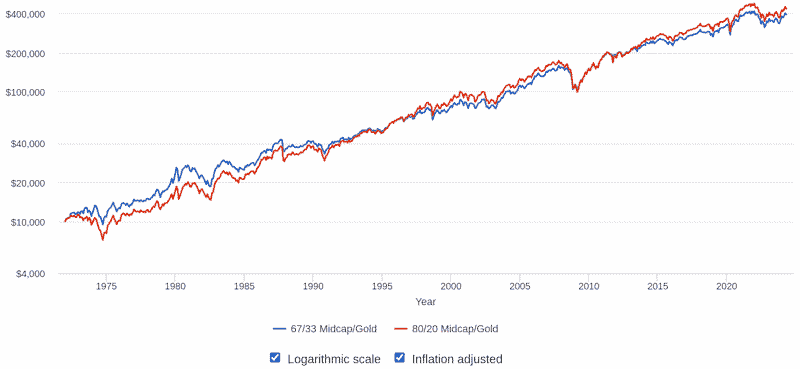

67/33 stock/gold is inclined to rise less during good times, fall less during bad times, and a degree of inverse correlations, whatever might drive stocks to halve could see the price of gold double. 67/33 stock/gold -> 33/67 stock/gold and rebalancing has you back to 67/33 stock/gold, no capital loss after stocks had halved, still holding 67/33 but where you're holding twice as many shares as before (less ounces of gold). At other times it swings the other way, end up with fewer shares, more ounces of gold.

Most wont be lumping in or out, will time average in (working/saving) and out (retired) over many years. Sometimes you'll be adding (removing) at lows, at other times highs, averages out. As such little cash needs to be held, just draw from whichever is the most up at the time. A couple of credit cards each with £5000/whatever limit is near instant £10,000 cash to hand. Daily spend using those, a week before the credit card payment date sell enough in your brokerage account and transfer the proceeds to your regular account in time to pay off the credit card bill.

Many might also own their own home, which adds to overall diversity.

A factor with stock funds is that they may benchmark/align to a index that discounts withholding taxes. SP500TRN ... US S&P500 total return net of 30% US default US dividend withholding taxes. If dividends were 4%, the index discounts 1.2%, so if the share price had remained unchanged across a year long period, the gross index total return gain of 4% would be recorded as a 2.8% Index total return gain, that actual funds might then compare/align their funds performance to. 2.8% index gain, fund achieved 2.1% gain in reflection of its 0.7% fund fees. Your £100,000 investment amount has £2100 credited (the broker actually owns the shares, not you), but discounts £10/month, £120/year in brokerage account fees. +£1980. But as part of sales pitches, by the taxman, market makers, brokers, fund managers ... etc that share a part of your money, will tend to use historic gross index total returns as enticement as to why you should invest in their products. Oh look if you'd invested in stocks you could have enjoyed a 4% SWR (withdrawal rate), but where after costs maybe more than half of that was actually directed towards others. The high wages, expensive buildings in expensive locations across the financial sector are a indication of just how good they are at filtering off little bits here and there of other peoples money to very good collective effect.