Between 1980 and 1999 it didn't really matter what you invested in, stocks or bonds did exceptionally well. Studies that utilise back-tests that span that period will be distorted by that. For example stocks made massive gains, getting on for 19% annualised type reward in the UK. Similar to the

17% in the US (the difference being down to the £'s relative decline compared to the US$)

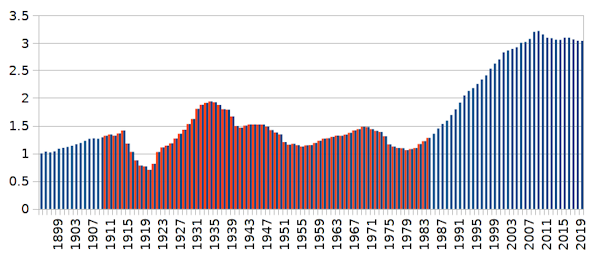

As this chart indicates, even UK T-Bills (short term Gilts) increased by around three-fold over the 1980 to early 2000's in after inflation (real) terms.

So I got to wondering about relative performance over a more neutral period, and came up with 1910 to 1984 years (inclusive), where broadly T-Bills overall sideways traded, ended at around the same inflation adjusted value as at the start, and that yearly averaged around the broader overall average. In other words were broadly flat in inflation adjusted terms (albeit with volatility along the way).

As part of that I was led to a interesting article

https://portfoliocharts.com/2015/11/17/ ... ates-work/ that indicates for those in drawdown, after factoring in such things as start date valuations, volatility ...etc. that broadly it didn't make much difference in the worst case whether you were stock heavy/bond light or bond heavy/stock light. But where perhaps in the average case stock-heavy yielded the higher average/best case outcomes. But where that is including the exceptional 1980 to 2000 period.

The mid 1960's to mid 1980's were a terrible time for stocks when in drawdown mode. Total returns before costs and taxes barely paced inflation such that any withdrawal (and paying taxes) were eating capital. Again the above chart indicates that T-Bills were also relatively poor, declining by around a third.

For those accumulating, increasingly lower prices as savings grow is great. On the flip side, for those in retirement increasing prices are great. For a investor who started accumulating liquid assets in the early 1970's, perhaps after earlier decades of having been predominately paying down a mortgage, and where they retired in/around 1980, then the conditions were near ideal. Perhaps a teacher (striving to fit a real world example) that was 50 in 1970 and had just paid off their house and started accumulating stocks/bonds and then retired at age 60 in 1980 (born 1920).

On the flip side it could prove that those that were accumulating from 1980, that were near or recently into retirement, it could very well be a case of their portfolio value declining in real total return terms, along with also being depended upon the portfolio to provide a income/drawdown. Putting all eggs into a single basket, such as stocks, or bonds, or maybe a combination of both, might not work as desired.

Perhaps too much emphasis is being placed on the assumption that stocks and/or bonds are the 'better' choice of assets. That at relatively high recent valuations wealth preservation and liability matching may prove to be the better choice. i.e. broader diversification. Perhaps some stock, some bonds, some gold, some inflation bonds, along with owning your own home so 'rent' is liability matched.

My thoughts are along the lines of perhaps owning a home alongside a Permanent Portfolio, but where the long dated bonds are held in Inflation Bonds (Index Linked Gilts) instead of conventional bonds may be better placed asset allocation for things to come.

Looking at the longer dated

Index Link Gilts price motion compared to

conventional Gilt price motion suggests broader similarities. Yes it seems crazy to buy into something that yields -2.4%/year type cost, but diluted down in being just 25% of the total portfolio value = 0.6%/year. Which might be considered as a form of portfolio insurance cost. That's less than what some pay in fund/IT 'management fees'

Unlike conventional bonds, where prices increase as nominal yields decline, prices decrease as nominal yields rise, with ILG's prices increase as real yields decline and decrease as real yields rise. If/when inflation rises so real yields will tend to increase, and see lower ILG prices, but more being received via higher inflation. If however the broader trend is for negative real yields, such as T-Bills losing value relative to inflation, then so ILG's will see even higher prices. What seems relatively expensive today could with hindsight been fair/cheap later.

Stocks to some extent are a form of undated variable coupon conventional bond.

Chuck out bonds altogether and a asset allocation of owning a home, some stock some gold ... is perhaps reasonable enough diversity for forward time (from current valuations). And backtesting that over the 1910 to 1984 'flat' years (with caveats that I wont detail here) indicates that did provide reasonable results. And held up better during 'down' (negative/declining real T-Bill) periods.

Gold might be considered as a even longer dated Index Linked Gilt, a undated zero coupon form of ILG.

I envy the likes of Warren Buffet and our local Terry (TJH) who seemingly lived through near ideal times for their age. Personally I'm more at the other end, just coming up to retirement, more a case of perhaps the perfect storm and where asset diversification more focused towards wealth preservation and assuming capital drawdown to service retirement income will become the 'norm' for that era and those that go with current 'traditional' asset allocations may suffer. On the plus side I'm blessed with a reasonable inflation linked occupational pension unlike those that the younger generation will benefit from. And for my sons in just starting out on their working life perhaps they'll be more inclined to see a repeat of their grandads generation of potentially accumulating stocks are relatively low price levels over time.

For me, now 'single' with two adult kids, a soon to be payable occupational pension at age 60, along with £10K/year x 7 years amount to cover (drawdown) until the £9K state pension also kicks in is enough for my lifestyle (given no more uni fees to cover etc.). A Permanent Portfolio for that £70K seems appropriate/reasonable. £22K to £25K/year disposable income type lifestyle. Own own home so no finding/paying rent issues. Which leaves a substantial amount that most likely will be passed over to the kids. If valuations/circumstances were lower/better I'd be more inclined to all-stock that for them. In the opinion however that both stocks and bond may struggle and that cost averaging in may prove to be the better, I'm more inclined to set them up with their own homes leaving them better placed to accumulate stocks over time out of new money (wages/savings) and for the remainder of liquid wealth holding a 50/50 stock/gold asset allocation. Writing off the Permanent Portfolio/drawdown amount, that would have family wealth at around 75% home values, 12.5% in each of stock and gold. Whilst I could envisage that 75% losing half or more, its a consumption asset, doesn't really matter, other than my own home value perhaps being called upon for twilight life care fees cover. Another option is to direct to home value being around 25%, and the rest in a Permanent Portfolio. Seeing the forecast by this Australian based version (that charges a whopping fee - so most certainly not a recommendation)

https://corcapital.com.au/fund-fact-sheet/Maximise return above change in CPI over 3 year periods without generating a negative return over any 12 month period

along with "3% to 5% real gains for money you can't afford to lose" ... type claims against the PP, the 25% home/75% PP (broader diversification than stock/bonds) has considerable appeal.