The Growth Ten (G10) was an accident. I intended to create only a rough-and-ready yardstick for UK investment trusts which concentrated on capital gain: following the biggest generalists as they were at the turn of the millennium, mostly old stagers already.

I was not out to plug them. But it transpired on jobbing back to 2000 that a portfolio invested with equal amounts would have fared quite well, despite their dim reputation. So I began to treat the Ten as a tool for timorous wealth-builders, reporting on progress at The Motley Fool. Here is a quick update for the past four years.

Constituents:

Aberforth Smaller Companies (ASL)

Alliance (ATST)

BMO Global Smaller Companies (BGSC)*

F&C (FCIT)+

Law Debenture (LWDB)

Monks (MNKS)

Scottish (SCIN)

Scottish American (SAIN, prev. SCAM)

Scottish Mortgage (SMT)

Witan (WTAN)

* formerly F&C Global Smaller Companies (FCS)

+ formerly Foreign & Colonial (FRCL)

The G10 is for long-term holders who wish to accumulate without too much speculating. Most members focus on larger and more developed foreign markets, though not necessarily on the biggest and staidest companies therein; Scottish Mortgage and to a lesser extent Monks relish whizzy 'disruptors'. Besides there is a British specialist in smaller issues, Aberforth, and an overseas counterpart, BMO Global Smaller Companies.

One mainstream op, Law Debenture, has a trading arm. The broadest based ITs, Alliance, F&C, Scottish and Witan, together hold hundreds of positions. Alliance and Witan are funds of funds, cracking the whip over subcontracted managers. F&C and Scottish are do-it-yourselfers. Scottish American stresses dividend as well as asset growth more than the rest.

I have no idea how this olla podrida breaks down between countries, sectors or market cap size, or how it stands up against a world equity index. Nor do I care. Doubtless Wall Street, FAANGs, global brands and consumer staples play big parts. I leave the mostly sobersided folks who run such portfolios to their job. The 'Doris' principle of picking a spread and leaving it be applies here as with income baskets. No fooling around with rebalancing after purchase either.

Results to the calendar year end are comparable with those of my imaginary 'HYP06' High Yield Portfolio (see the Jan. 6 post on the HYP Practical board). They arise from the same £75,000 gross outlay-- £7,500 per trust-- on the same start date of Jan. 13, 2006. Below are values; percentage changes year by year; real change deflated by the Retail Prices Index/performance against the FT All Share Index in percentage points, where a minus value is underperformance.

CAPITAL (at Dec. 31)

2006: £81,604, +8.8, +4.4/-2.5

2007: £85,190, +4.4, +0.4/2.4

2008: £56,446, -33.7, -34.6/-1.0

2009: £72,365, +28.2, +25.8/1.2

2010: £90,109, +24.5, +19.7/11.6

2011: £80,336, -10.5, -15.6/-4.2

2012: £93,149, +15.9, +12.8/7.7

2013: £119,650, +28.4, +25.7/11.8

2014: £123,560, +3.3, +1.7/3.4

2015: £137,020, +5.8, +4.6/8.3

2016: £154,392, +18.1, +15.6/5.7

2017: £187,067, +21.2, +17.1/12.2

2018: £173,543, -7.2, -9.9/5.7

2019: £212,432, +22.4, +20./ 8.2

The G10 topped £200,000 for the first time in 2019, close to tripling its investment. It outperformed the All-Share Index by an average 5.7 percentage points pa on share price, by a cumulative 74% and in 11 of 14 years, including the past eight. The latest outperformance, of 8.2 points, was below 2017's record but above the whole-life average equalled in 2016 and 2018.

The compound annual growth rate between inception and Dec. 31 was 8.7% pa or c. 5.7% pa in real terms. The Basket of Seven achieved about 2% real. (It has thrived less since 2005 than in the prior reaction against the tech boom, whereas the G10 had got some fingers burned by internet mania.)

The FE Trustnet Risk Score for the Ten is 110 (skewed by SMT's 185), for the Seven 99. The FTSE 100 is the benchmark here on 100 where cash is 0. So the G10 is reasonably non-volatile, although it lost one-third of its worth in the darkest year of the global crisis and would be less cushioned by dividends in any general slump. For now, figures reflect the superior economics of much of the world beyond the UK and the weakness of its currency. Gearing in trusts helped modestly, given money's cheapness, although debt is usually under one-tenth of net assets.

The average discount of 4.3% at financial year ends in 2018-19 is below the 7% of 2000-19. It shrank by half a point from 2017-18. The tightest discount was 2.7% in 2015-16,after languishing in double figures for most of the previous 15 years. Then it was the fashion to predict extinction at the hands of voracious pension funds for big, boring global ITs. Such talk seems to have died out.

INCOME

This is a minor consideration. Scottish American is the only member with a HYP-sized yield, overlapping Murray International (MYI) in the B7 in that way. Monks pays almost nothing by design. Scottish Mortgage has downplayed the payout as it goes more and more for futurological punts.

Others have moved to quarterly distributions and begun to emphasise them more, perhaps responding to the retail-investor Zeitgeist, but that is relative: typically the G10 yields less than half the All-Share Index and far less than the Baskets of Seven or Eight. However, income growth has been spirited and can be treated as a reward en passant for patience.

Actual amounts produced including specials, plus nominal and real percentage changes each year:

2006: £1,377

2007: £1,679, +21.9, +17.9

2008: £1,850, +10.2, +9.3

2009: £1.948, +5.3, +2.9

2010: £1.849, -5.0, -9.8

2011: £1,994, +7.8, +3.0

2012: £2,210, +10.8, +7.7

2013: £2,362, +6.9, +4.2

2014: £2,428, +2.8, +1.2

2015: £2,587, +6.6, +5.4

2016: £2,585, -0.1, -2.6

2017: £2,729, +5.5, +1.4

2018: £3,069, +12.5, +9.8

2019: £3,241, +5.6, +3.4

The Growth Ten has disbursed £31,907 on a capital of £75,000, compared with £47,863 from the 'growth-of-income' B7. The latter's receipts never suffered a real decline between years, whereas the G10's fell in 2010 and less seriously in 2016 (1). But latest annual valuations put the G10 two-fifths ahead. Its combined cumulative return is £169,339, one-third more than the basket's £124,168.

Last year the Ten lifted dividends by 5.6%, or by 3.4% after inflation. This was below the average real rise of 4% pa (7% before inflation) over 13 years. Dividends in 2006-19 compounded at 6.8% pa nominal versus the B7's 7.8% from a much larger first-year haul.

The tradeoff with capital is obvious. Moreover, by keeping higher cover the Ten hold back more earnings for recycling, suitably for individual squirrellers. And G10 income remains parsimoniously dispensed: cover for payouts averaged 1.17 times in latest financial years, above the average this century of 1.10 times.

The aggregate revenue reserve has averaged 25 months of current payout since 2000, and has stayed near that ample level recently. Many income ITs get by on half as much. These stats give reason to think revenue will go on outpacing baskets' and buttressing ratings-- together with an inclination by governments such as Japan's and India's to encourage disbursement of corporate earnings.

Ongoing Charges Ratios vary a lot, but the trend is down. Averaging 0.9% this century, they were 0.64% in 2018-19, assisted by rising values but also by the need to compete against open-ended funds. SMT is notably cheap at 0.35%; Aberforth with its elaborate and academic research technique rather dear at 1.2%.

CONSTITUENTS

Briefly, individual trusts' contributions: share price change since launch; number of financial years share price trailed the index and average year-end discount or (premium) during past decade/Risk Score:

ASL: +132.1, 3, 11.5/138

ATST: +141.7, 1, 11.2/108

BGSC: +277.5, 1, 2.0/119

FCIT: +192.7, 2, 8.7/113

LWDB: +117.0, 3, (4.3)*/123

MNKS: +244.3, 3, 7.7/127

SAIN: +86.8, 4, (1.8)/113

SCIN: +92.6, 2, 12.4/99

SMT: +370.6, 3, 3.6/85

WTAN: +177.1, 1, 7.0/105

------------------------------------

G10: +183.2, 1, 6.7/110

* Magnified by overheads of fiduciary businesses

The most valuable member-- with eight wins in a row out of thirteen Dec. year ends before 2019-- has been BMO Smaller Companies. Four blue ribands went to Scottish Mortgage. The bottom marker most often was Scottish, nine times... of which eight were in 2012-19. What's that I hear about inevitable reversion to the mean?

No corporate actions would have required a response from a G10 owner since 2006. Boris rampages on, Doris sleeps on.

----------------------------------------------------------------------------------------------------------------------

(1) FWIW, income could have been 'derisked' to provide an initial spendable withdrawal rate of 1.5% pa-- rising to 2.54% with inflation protection, in three increments by 2015. Holding back that much, one-tenth of the inflow, would have filled a reserve presently worth 14 months'' indexed spendable income. The B7 accommodates 4.3%+RPI with 13 months' worth. However the G10 is not tasked to pay regular bills.

Got a credit card? use our Credit Card & Finance Calculators

Thanks to Rhyd6,eyeball08,Wondergirly,bofh,johnstevens77, for Donating to support the site

The Growth Ten: 2006-19

-

Luniversal

- 2 Lemon pips

- Posts: 157

- Joined: November 4th, 2016, 11:01 am

- Has thanked: 14 times

- Been thanked: 1163 times

-

Lootman

- The full Lemon

- Posts: 18931

- Joined: November 4th, 2016, 3:58 pm

- Has thanked: 636 times

- Been thanked: 6669 times

Re: The Growth Ten: 2006-19

Luniversal wrote:Scottish Mortgage has downplayed the payout as it goes more and more for futurological punts.

SMT's biggest holding is Amazon. If you think that is the "future" then you probably still do all your shopping at Woolworths.

-

Bouleversee

- Lemon Quarter

- Posts: 4654

- Joined: November 8th, 2016, 5:01 pm

- Has thanked: 1195 times

- Been thanked: 903 times

Re: The Growth Ten: 2006-19

Lootman wrote:Luniversal wrote:Scottish Mortgage has downplayed the payout as it goes more and more for futurological punts.

SMT's biggest holding is Amazon. If you think that is the "future" then you probably still do all your shopping at Woolworths.

He'll have a job since it doesn't exist any more.

-

monabri

- Lemon Half

- Posts: 8425

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: The Growth Ten: 2006-19

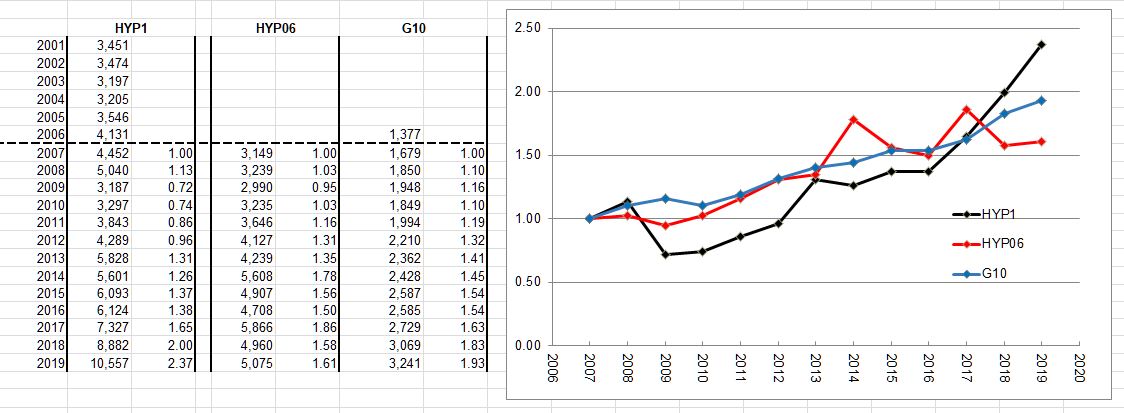

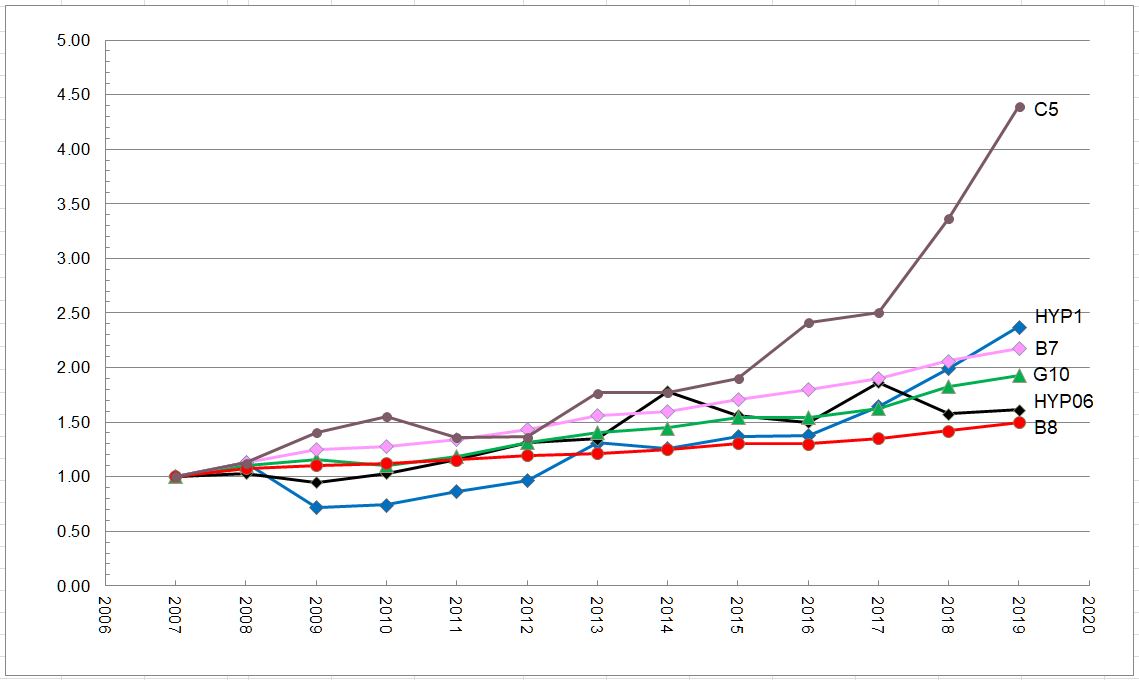

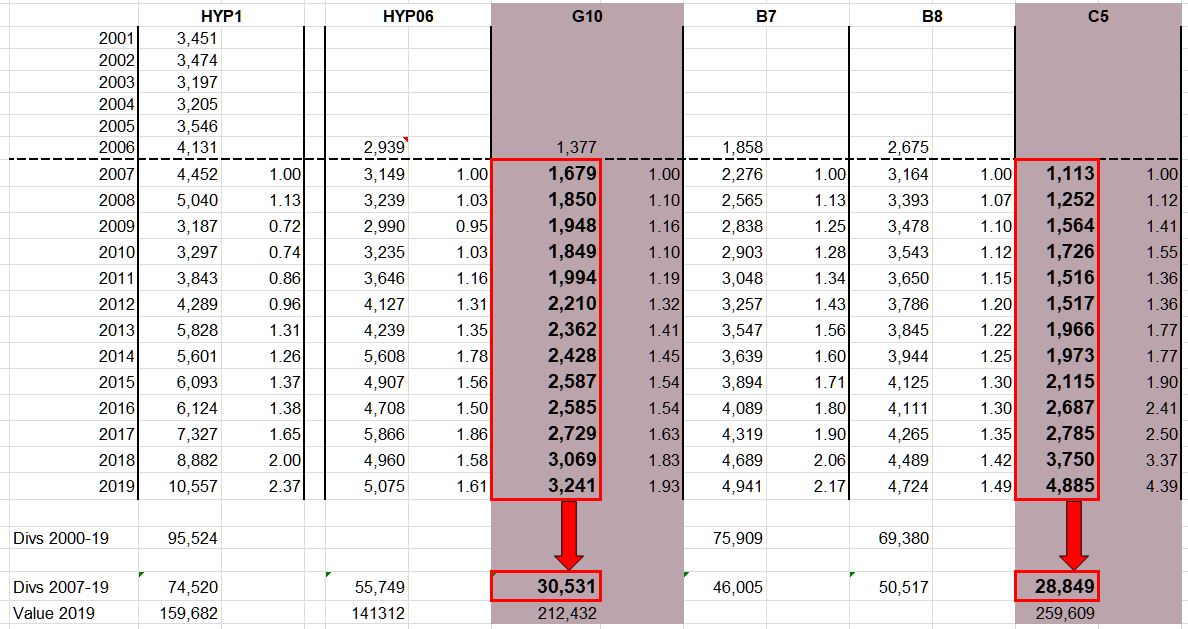

The G10 dividend growth compared to HYP1 & HYP06 with 2007 as a baseline - almost draw a straight line for G10

-

Luniversal

- 2 Lemon pips

- Posts: 157

- Joined: November 4th, 2016, 11:01 am

- Has thanked: 14 times

- Been thanked: 1163 times

Re: The Growth Ten: 2006-19

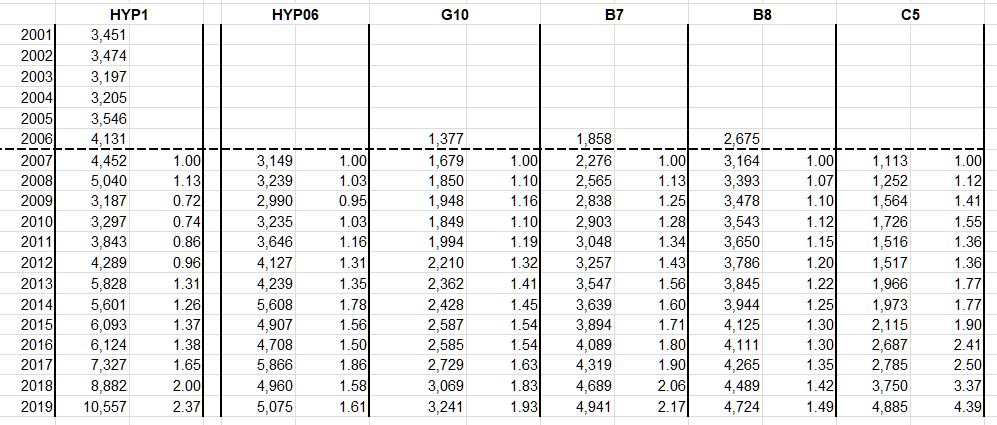

Thank you very much for this useful visualisation.

Might I ask that you add the income trendline for the Conviction Five as posted above, and also these comparable inflows for the Baskets of Seven and Eight?

B7

2006: 1858

2007: 2276

2008: 2565

2009: 2838

2010: 2903

2011: 3048

2012: 3257

2013: 3547

2014: 3639

2015: 3894

2016: 4089

2017: 4319

2018: 4689

2019: 4941

---------------

B8

2006: 2675

2007: 3164

2008: 3393

2009: 3478

2010: 3543

2011: 3650

2012: 3786

2013: 3845

2014: 3944

2015: 4125

2016: 4111

2017: 4265

2018: 4489

2019: 4724

Might I ask that you add the income trendline for the Conviction Five as posted above, and also these comparable inflows for the Baskets of Seven and Eight?

B7

2006: 1858

2007: 2276

2008: 2565

2009: 2838

2010: 2903

2011: 3048

2012: 3257

2013: 3547

2014: 3639

2015: 3894

2016: 4089

2017: 4319

2018: 4689

2019: 4941

---------------

B8

2006: 2675

2007: 3164

2008: 3393

2009: 3478

2010: 3543

2011: 3650

2012: 3786

2013: 3845

2014: 3944

2015: 4125

2016: 4111

2017: 4265

2018: 4489

2019: 4724

-

monabri

- Lemon Half

- Posts: 8425

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: The Growth Ten: 2006-19

Luniversal wrote:Thank you very much for this useful visualisation.

Might I ask that you add the income trendline for the Conviction Five as posted above, and also these comparable inflows for the Baskets of Seven and Eight?

picture to url

picture to url

-

monabri

- Lemon Half

- Posts: 8425

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: The Growth Ten: 2006-19 Versus Conviction 5

What's in the Conviction 5 (C5)?

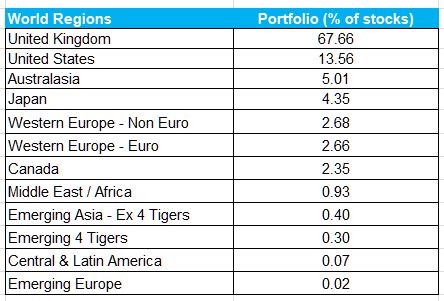

Using MorningStar's X-Ray Tool (see link below) and for an equal percentage of the C5 constituents (CGT,LTI,PNL,RICA & IIT), 'our' investment universe is predominantly UK at ~68% with the US coming in second at just under 14%.

The next table shows the breakdown of assets for each of the 5 components, showing the high proportion of bonds held in CGT & PNL.

One comparison that one could make is to the more internationally flavoured Conviction 10 (C10) which contains Aberforth Smaller Companies (ASL), Alliance (ATST), BMO Global Smaller Companies (BGSC), F&C (FCIT), Law Debenture (LWDB), Monks (MNKS) , Scottish (SCIN), Scottish American (SAIN, prev. SCAM), Scottish Mortgage (SMT) & Witan (WTAN)

Dividend Growth

In terms of recent dividend GROWTH RATE, C5 appears to be a clear winner (evidenced from the graph in an earlier posting in this thread above).

Dividends Paid

However, when one compares Dividends Paid, there is some, but not that much clear water between them over a fair number of years (2007 - 2019). G10 has delivered £30,531 versus a slightly less £28849 for C5.

Valuation

The C5 valuation (£259609) was captured on 20th January 2020 whilst G10 (£212432) on Jan 28th 2020...a £47k variation.

Thoughts :

I thought UK markets had more or less marked time for the last 10 years ? So, wouldn't one expect the "foreign fund" bearing Conviction 10 to have grown more in terms of total valuation but this appears not to be the case?

Let's have a look at whats in C10 "country wise".

Another comment - In addition, C5 contains a fair smattering of bonds (~25% of the C5 portfolio) which would limit dividend growth rates.

What's in C10 country-wise ?

note: Europe is mainly Europe but there is a small percentage of Middle East & Africa included in the mix - but not to a significant extent.

A quick assessment indicates the following comparative percentages (with a little rounding) :

Conclusions ...?

C5 has delivered not much less than G10 in terms of dividends paid but the current valuation is quite a bit better. Also, the dividend growth rate of C5 seems to be taking off!

I must admit to surprise..the C5 basket is strongly UK biased (TWICE that of G10). Perhaps the stabilising effect of ~25% bond content in C5 has contributed more strongly to overall performance than imagined? I think I'd have liked to have placed my bet on C5 rather than G10.

It is also apparent from the info in the 3rd table, that the superior dividend payments of HYP1 and HYP06 have limited their current valuations (*) but it is a case of if you add up the Jam you've consumed over the years (i.e. dividends) and the current valuation...have HYP1 & HYP06 suffered ..I'd say not significantly (especially if one were to factor in the value of having the money up front in the form of a divi to live off).

share picture

share picture

(*) The HYP01 valuation was mid-November 19. The valuation then would likely be less than in Jan 2020 when the C5/G10 baskets were reviewed.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

MorningStar X Ray Tool

http://tools.morningstar.co.uk/uk/xray/ ... geId=en-GB

Using MorningStar's X-Ray Tool (see link below) and for an equal percentage of the C5 constituents (CGT,LTI,PNL,RICA & IIT), 'our' investment universe is predominantly UK at ~68% with the US coming in second at just under 14%.

The next table shows the breakdown of assets for each of the 5 components, showing the high proportion of bonds held in CGT & PNL.

One comparison that one could make is to the more internationally flavoured Conviction 10 (C10) which contains Aberforth Smaller Companies (ASL), Alliance (ATST), BMO Global Smaller Companies (BGSC), F&C (FCIT), Law Debenture (LWDB), Monks (MNKS) , Scottish (SCIN), Scottish American (SAIN, prev. SCAM), Scottish Mortgage (SMT) & Witan (WTAN)

Dividend Growth

In terms of recent dividend GROWTH RATE, C5 appears to be a clear winner (evidenced from the graph in an earlier posting in this thread above).

Dividends Paid

However, when one compares Dividends Paid, there is some, but not that much clear water between them over a fair number of years (2007 - 2019). G10 has delivered £30,531 versus a slightly less £28849 for C5.

Valuation

The C5 valuation (£259609) was captured on 20th January 2020 whilst G10 (£212432) on Jan 28th 2020...a £47k variation.

Thoughts :

I thought UK markets had more or less marked time for the last 10 years ? So, wouldn't one expect the "foreign fund" bearing Conviction 10 to have grown more in terms of total valuation but this appears not to be the case?

Let's have a look at whats in C10 "country wise".

Another comment - In addition, C5 contains a fair smattering of bonds (~25% of the C5 portfolio) which would limit dividend growth rates.

What's in C10 country-wise ?

note: Europe is mainly Europe but there is a small percentage of Middle East & Africa included in the mix - but not to a significant extent.

A quick assessment indicates the following comparative percentages (with a little rounding) :

Conclusions ...?

C5 has delivered not much less than G10 in terms of dividends paid but the current valuation is quite a bit better. Also, the dividend growth rate of C5 seems to be taking off!

I must admit to surprise..the C5 basket is strongly UK biased (TWICE that of G10). Perhaps the stabilising effect of ~25% bond content in C5 has contributed more strongly to overall performance than imagined? I think I'd have liked to have placed my bet on C5 rather than G10.

It is also apparent from the info in the 3rd table, that the superior dividend payments of HYP1 and HYP06 have limited their current valuations (*) but it is a case of if you add up the Jam you've consumed over the years (i.e. dividends) and the current valuation...have HYP1 & HYP06 suffered ..I'd say not significantly (especially if one were to factor in the value of having the money up front in the form of a divi to live off).

share picture(*) The HYP01 valuation was mid-November 19. The valuation then would likely be less than in Jan 2020 when the C5/G10 baskets were reviewed.

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

MorningStar X Ray Tool

http://tools.morningstar.co.uk/uk/xray/ ... geId=en-GB

Re: The Growth Ten: 2006-19 Versus Conviction 5

monabri wrote:The next table shows the breakdown of assets for each of the 5 components, showing the high proportion of bonds held in CGT & PNL.

The numbers don't look right in that table for some of the funds. Ruffer's monthly from december indicates circa 40% equities, not 8.95%. Also, the PNL line isn't accounting for their gold holding (I'd expect circa 10% in the other column).

- 0x3F

-

monabri

- Lemon Half

- Posts: 8425

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: The Growth Ten: 2006-19 Versus Conviction 5

0x3F wrote:monabri wrote:The next table shows the breakdown of assets for each of the 5 components, showing the high proportion of bonds held in CGT & PNL.

The numbers don't look right in that table for some of the funds. Ruffer's monthly from december indicates circa 40% equities, not 8.95%. Also, the PNL line isn't accounting for their gold holding (I'd expect circa 10% in the other column).

- 0x3F

Thanks for pointing that out. I sourced the information from MorningStar ..I'm surprised at such a difference. What I was trying to uncover was a reason why C5 dividends were growing so strongly compared to the other baskets.

-

Luniversal

- 2 Lemon pips

- Posts: 157

- Joined: November 4th, 2016, 11:01 am

- Has thanked: 14 times

- Been thanked: 1163 times

Re: The Growth Ten: 2006-19 Versus Conviction 5

Many thanks for the expanded income graph.

Just to make it clear: capital values for the baskets, Growth Ten and Conviction Five are uniform to Dec. 31; HYP1 is pyad's calculation to approx. Nov. 10. Nearest working day in all models.

The reason for C5's takeoff in income relative to the rest of my portfolios is Lindell Train Investment Trust's 24.2% stake in its management company. LTI's income (£) and percentage share of the C5 total by years:

2019: 3420 70.0

2018: 2529 67.5

2017: 1833 65.8

2016: 1033 38.4

2015: 835 39.5

2014: 784 39.7

2013: 1725 36.9

2012: 481 31.7

2011: 423 27.9

2010: 423 24.5

2009: 423 27.1

2008: 244 19.8

2007: 203 18.2

2006: 203 22.1

As with capital, a C10 would have braked income by diluting LTI's contribution, without adding much devolatilisation. Five positions looks optimal and less trouble.

As the inverse of HYP, 'income does not matter'. It is less correlated with the health of the portfolio as a wealth-defender than HYP valuations are a measure of their capacity to go on paying dividends: conviction as an attitude is more freewheeling and income incidental.

The big barbell play in retiral is to divide one's fortune between a growth and an income strategy according to how much gratification is to be immediate or deferred- though late in life it may be more about self-preservation than pleasure, e.g. care costs.

A Conviction Four omitting LTI would have grown from £75,000 to £149,400 rather than £259,609, and income would have totalled £20,235 instead of £29,749. This demonstrates how one winner can transform a spread. It is a milder version of Hollywood economics: one blockbuster more than makes up for several turkeys or so-so performers.

Damage to a C5 caused by a loose cannon might have defeated the capital-preservation objective. Your selection should prioritise the trusts' professed desire to avoid downers. Lindsell Train may recently have galvanised results, but that is happenstance. It was chosen because it was shooting for long-term growth at moderate risk; nobody knew the management company would become a windfall. If Train and Lindsell lose lustre, the portfolio as a whole may jog on or another member may scintillate. All beside the point, as long as total worth marches with inflation.

Choose managers you believe are on the right lines. Never mind if they disagree among themselves or have somewhat differing priorities; they need not seek exactly what you want. Let them alone and hope the clash of opinion and practice provides a benign synthesis-- for you, most of the time, if not for them all the time.

PS: I do not take exercises such as Morningstar's X-ray seriously, since in my experience such breakdowns of the ultimate geographical origins of earnings are formalistic; notably in treating every British-registered global conglomerate as 'UK' for the split. But I also have doubts about how sectoral definitions are applied across and even within borders.

Breakdowns between asset classes are more reliable, but I am a sceptic about asset allocation in principle. IMHO it makes no sense to treat 'equities' as another option on all fours with property or gold when it straddles so much more profit-seeking activity, and might embrace gold-mining stocks or REITs anyway.

Just to make it clear: capital values for the baskets, Growth Ten and Conviction Five are uniform to Dec. 31; HYP1 is pyad's calculation to approx. Nov. 10. Nearest working day in all models.

The reason for C5's takeoff in income relative to the rest of my portfolios is Lindell Train Investment Trust's 24.2% stake in its management company. LTI's income (£) and percentage share of the C5 total by years:

2019: 3420 70.0

2018: 2529 67.5

2017: 1833 65.8

2016: 1033 38.4

2015: 835 39.5

2014: 784 39.7

2013: 1725 36.9

2012: 481 31.7

2011: 423 27.9

2010: 423 24.5

2009: 423 27.1

2008: 244 19.8

2007: 203 18.2

2006: 203 22.1

As with capital, a C10 would have braked income by diluting LTI's contribution, without adding much devolatilisation. Five positions looks optimal and less trouble.

As the inverse of HYP, 'income does not matter'. It is less correlated with the health of the portfolio as a wealth-defender than HYP valuations are a measure of their capacity to go on paying dividends: conviction as an attitude is more freewheeling and income incidental.

The big barbell play in retiral is to divide one's fortune between a growth and an income strategy according to how much gratification is to be immediate or deferred- though late in life it may be more about self-preservation than pleasure, e.g. care costs.

A Conviction Four omitting LTI would have grown from £75,000 to £149,400 rather than £259,609, and income would have totalled £20,235 instead of £29,749. This demonstrates how one winner can transform a spread. It is a milder version of Hollywood economics: one blockbuster more than makes up for several turkeys or so-so performers.

Damage to a C5 caused by a loose cannon might have defeated the capital-preservation objective. Your selection should prioritise the trusts' professed desire to avoid downers. Lindsell Train may recently have galvanised results, but that is happenstance. It was chosen because it was shooting for long-term growth at moderate risk; nobody knew the management company would become a windfall. If Train and Lindsell lose lustre, the portfolio as a whole may jog on or another member may scintillate. All beside the point, as long as total worth marches with inflation.

Choose managers you believe are on the right lines. Never mind if they disagree among themselves or have somewhat differing priorities; they need not seek exactly what you want. Let them alone and hope the clash of opinion and practice provides a benign synthesis-- for you, most of the time, if not for them all the time.

PS: I do not take exercises such as Morningstar's X-ray seriously, since in my experience such breakdowns of the ultimate geographical origins of earnings are formalistic; notably in treating every British-registered global conglomerate as 'UK' for the split. But I also have doubts about how sectoral definitions are applied across and even within borders.

Breakdowns between asset classes are more reliable, but I am a sceptic about asset allocation in principle. IMHO it makes no sense to treat 'equities' as another option on all fours with property or gold when it straddles so much more profit-seeking activity, and might embrace gold-mining stocks or REITs anyway.

-

1nvest

- Lemon Quarter

- Posts: 4432

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1350 times

Re: The Growth Ten: 2006-19 Versus Conviction 5

Luniversal wrote:A Conviction Four omitting LTI would have grown from £75,000 to £149,400 rather than £259,609, and income would have totalled £20,235 instead of £29,749. This demonstrates how one winner can transform a spread. It is a milder version of Hollywood economics: one blockbuster more than makes up for several turkeys or so-so performers.

I like that Hollywood economics simile

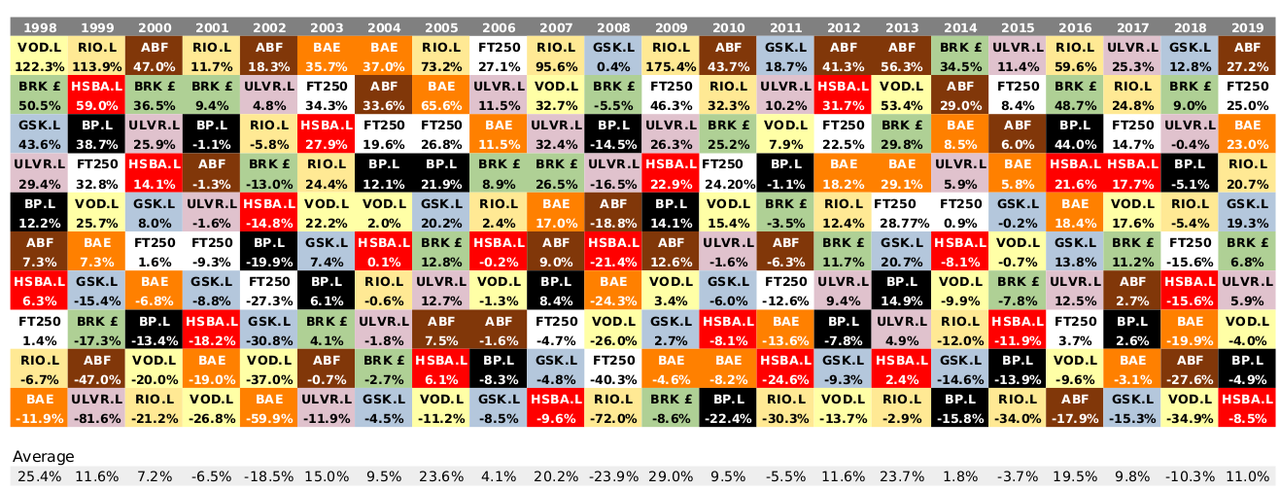

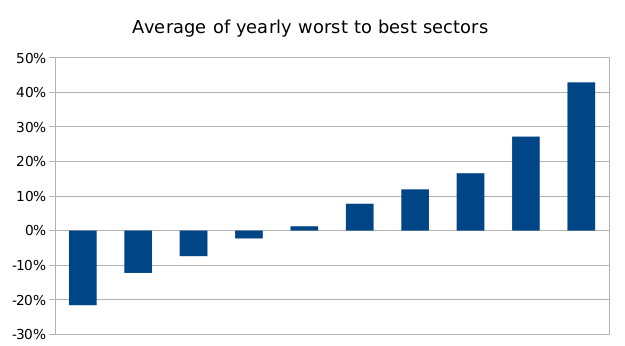

Comparing the following basket of 10 yearly equal weighted large cap sector diversified multinationals total return for the 2006 onward period to your C5 total return and it looks like those total returns broadly compared, despite several in that set of stocks being relatively poor performers : ULVR, BP, BAE, VOD, GSK in price only terms making barely 1% or less annualised gains since 1998, but somewhat better after dividends were included. Despite being individual dogs over the total period they were (excepting BP) the best performing asset in some years, helping to keep the average of the yearly 'best' being higher than the average of the yearly worst.

If would be interesting to see a comparison of the difference between yearly rebalancing C5 back to equal weightings compared to your existing not rebalanced results. In practice that needn't be to literal equal weightings but might involve once/year selling/reducing two, to add to two others (steer towards equal weightings). In the above 10-way set, that added around a 1%/year additional benefit compared to not rebalancing.

-

1nvest

- Lemon Quarter

- Posts: 4432

- Joined: May 31st, 2019, 7:55 pm

- Has thanked: 691 times

- Been thanked: 1350 times

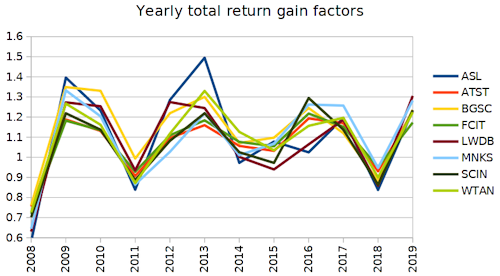

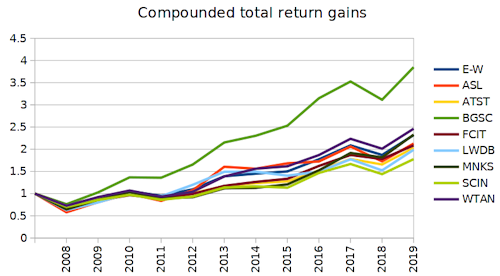

Re: The Growth Ten: 2006-19

From a limited test (lack of Yahoo data from 2008 and only for 8 of the 10)

Looks like the yearly gain/loss factors are quite correlated

And mostly compound out much the same, excepting one exception in that set/date range (BGSC) that had a relatively good year in one of the earlier years

As to answering my own question, yearly equal weight rebalancing (E-W) was near-as no difference in overall reward.

Looks like the yearly gain/loss factors are quite correlated

And mostly compound out much the same, excepting one exception in that set/date range (BGSC) that had a relatively good year in one of the earlier years

As to answering my own question, yearly equal weight rebalancing (E-W) was near-as no difference in overall reward.

Who is online

Users browsing this forum: No registered users and 24 guests