Have read other similar posts but was wondering what people’s thoughts are on how this portfolio I am planning to hold long term will fair.

Key Points

- Secure engineering job in early 30s

- £100,000 currently invested in S&S ISA with ii

- Total yearly contribution going forward - £20,000 ISA limit thus monthly - £1667

- Interactive Investor Platform Yearly Fees total £120

- Transaction fees as regular investor £0 for purchases – monthly investment

- Yearly rebalancing of portfolio asset allocation

- 100% equity

Initial Portfolio Allocations

Based on VRWL/ VRWP Allocations

North America 62.60%

Europe 16.30%

Pacific 10.80%

Emerging Markets 10.10%

Middle East 0.20%

Investment forecasts seems to suggest that EM/EU excluding UK more likely to outperform over the course of next 5 years. US despite dominating over the course of the past significant number of years with elevated valuations estimated to underperform.

VHVG VANGUARD FUNDS PLC FTSE DEVELOPED WORLD UCITS ETF 0.12% cost – 80% allocation

VFEG VANGUARD FUNDS PLC FTSE EMERGING MARKETS UCITS ETF 0.22% cost - 15% allocation

FTSE Developed Europe UCITS ETF 0.10% cost - 5% allocation

Total fees – inclusive of platform/ investments with £2000 addition throughout the year approximately - £289. Equivalent 1% IT/Fund fees would equate to approximately £1320 – I appreciate that there are cheaper options but 1% didn’t seem unduly unfair.

Based on a 5% annualised return: Portfolio will be worth very approximately £408,820. (~£5627 will have been spent on fees, with £108200 interest accrued). Not inflation adjusted.

Got a credit card? use our Credit Card & Finance Calculators

Thanks to jfgw,Rhyd6,eyeball08,Wondergirly,bofh, for Donating to support the site

Portfolio Critique

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

Your allocation fair enough, if you can stomach 100% equities. You are brave to overweight EM. Vanguard thinks the Euro Zone is undervalued. You could include a UK bias. The UK has a fair valuation according to Vanguard, there is no withholding tax on dividends, and a UK bias potentially reduces the volatility a little. Nonetheless, you may be better off with just the first two funds in their market weights.

I am sure that you can do better on costs. You can stagger your purchases, and perhaps use a cheaper broker than II. Your weights do not have to be exact. 1% costs would be a real killer.

5% return may be too optimistic. The equity risk premium was reckoned to be 2.9% by JP Morgan in a May FT article, and the market has gone up since then. With gilts yielding about 1%, that corresponds to an equity return of less than 4%, before costs and taxes.

With inflation at an average of about 4% (1% over the BOE target), you will be struggling to match inflation. Nonetheless, that would just be the central expectation. The expected return would be swamped by random volatility. The actual return will probably be much more or much less than the expectation.

I am sure that you can do better on costs. You can stagger your purchases, and perhaps use a cheaper broker than II. Your weights do not have to be exact. 1% costs would be a real killer.

5% return may be too optimistic. The equity risk premium was reckoned to be 2.9% by JP Morgan in a May FT article, and the market has gone up since then. With gilts yielding about 1%, that corresponds to an equity return of less than 4%, before costs and taxes.

With inflation at an average of about 4% (1% over the BOE target), you will be struggling to match inflation. Nonetheless, that would just be the central expectation. The expected return would be swamped by random volatility. The actual return will probably be much more or much less than the expectation.

-

mark85

- Posts: 15

- Joined: January 13th, 2022, 8:04 pm

Re: Portfolio Critique

Thank you for the reply.

A small home bias may seem reasonable though lifestrategy has underperformed over the past years in part due to this - from my understanding they have a significantly greater allocation to FTSE.

Charges don't seem unreasonable to me? Management costs work out at 0.13% across those 3 at current weightings with platform fee at £120 a year working out at 0.12% for 100k account with no platform purchase transaction costs. Platform fees are fixed so for 200k account would be 0.06% of account value. Apologies if I was unclear the 1% was a comparison to many actively managed funds such as fundsmith OCF 1.05% and the impact they would have on returns to relatively cheap trackers in this portfolio. Though if there is a cheaper or better way to do it I'm always open to ideas!!

Hmm that doesn't make for great reading however hopefully time in the market will pay off.

A small home bias may seem reasonable though lifestrategy has underperformed over the past years in part due to this - from my understanding they have a significantly greater allocation to FTSE.

Charges don't seem unreasonable to me? Management costs work out at 0.13% across those 3 at current weightings with platform fee at £120 a year working out at 0.12% for 100k account with no platform purchase transaction costs. Platform fees are fixed so for 200k account would be 0.06% of account value. Apologies if I was unclear the 1% was a comparison to many actively managed funds such as fundsmith OCF 1.05% and the impact they would have on returns to relatively cheap trackers in this portfolio. Though if there is a cheaper or better way to do it I'm always open to ideas!!

Hmm that doesn't make for great reading however hopefully time in the market will pay off.

Re: Portfolio Critique

I don’t think it’s too bad a portfolio

Have you the courage to stick with it?

Otherwise a global equities index tracker would do the same job in a cheaper ,easier to manage and in a more understandable way

Once you have saved a reasonable amount then bonds are required to reduce the volatility of your portfolio and let you sleep at night and help you stay the course

Your age minus 10 in bonds is a rough guide

(A global bond index tracker hedged to the pound would do the business)

xxd09

Have you the courage to stick with it?

Otherwise a global equities index tracker would do the same job in a cheaper ,easier to manage and in a more understandable way

Once you have saved a reasonable amount then bonds are required to reduce the volatility of your portfolio and let you sleep at night and help you stay the course

Your age minus 10 in bonds is a rough guide

(A global bond index tracker hedged to the pound would do the business)

xxd09

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

An argument in favour of a home bias is precisely that it has done badly in the past decade. The hope is that the old technology stocks that dominate the FTSE 100 are now less overpriced than the growth stocks that now dominate the global index, and that the FTSE 100 will outperform as a result. Nevertheless, it is probably best to trust the market and buy the market, i.e. about 0.9*VHVG + 0.1*VFEG. That is simpler too.

iWeb is cheaper than II, and is likely to be at least as safe. With a relatively small portfolio, by the standards of this board, you could afford to go with Freetrade. It is unlikely that they will go bust, and you will almost certainly be paid out in full by the FSCS if they do.

iWeb is cheaper than II, and is likely to be at least as safe. With a relatively small portfolio, by the standards of this board, you could afford to go with Freetrade. It is unlikely that they will go bust, and you will almost certainly be paid out in full by the FSCS if they do.

-

Hariseldon58

- Lemon Slice

- Posts: 835

- Joined: November 4th, 2016, 9:42 pm

- Has thanked: 124 times

- Been thanked: 514 times

Re: Portfolio Critique

For the OP I’d just go for an All World tracker.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

-

csearle

- Lemon Quarter

- Posts: 4834

- Joined: November 4th, 2016, 2:24 pm

- Has thanked: 4859 times

- Been thanked: 2122 times

Re: Portfolio Critique

Hi, Welcome to The Lemon Fool!mark85 wrote:Have read other similar posts but was wondering what people’s thoughts are on how this portfolio I am planning to hold long term will fair.

I hope you find what you are looking for here.

All the best,

Chris

-

monabri

- Lemon Half

- Posts: 8427

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: Portfolio Critique

Hariseldon58 wrote:For the OP I’d just go for an All World tracker.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

This one?

ISIN GB00BMJJJF91

https://www.hl.co.uk/funds/fund-discoun ... cumulation

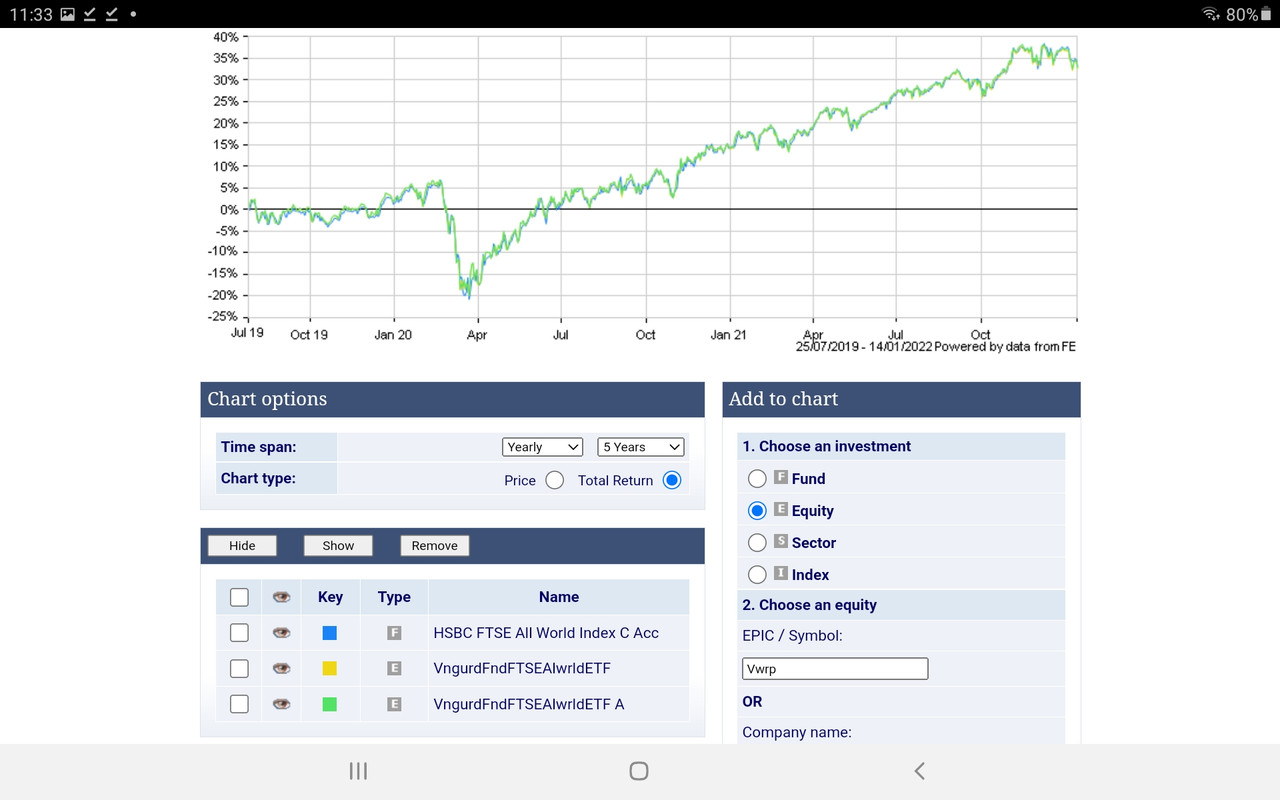

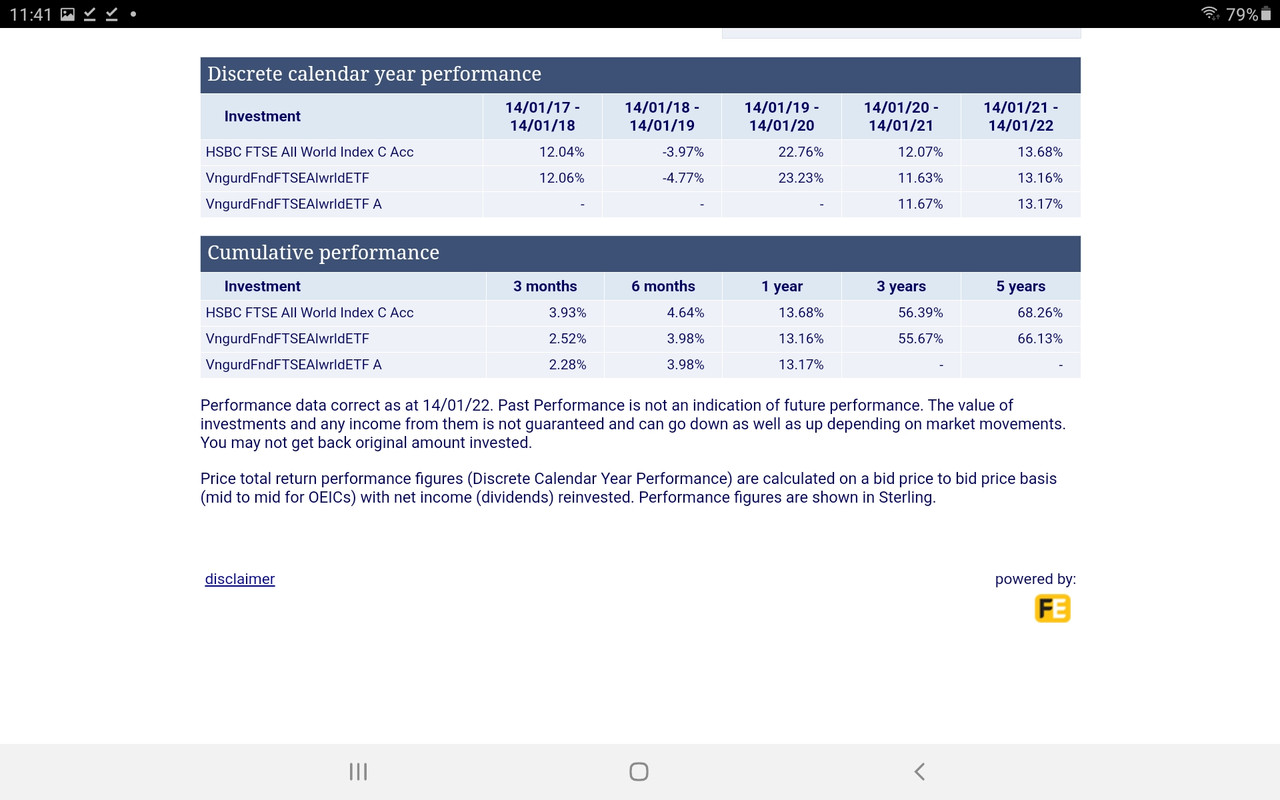

A comparison of total return ( 5 years) of VWRL, VWRP and the HSBC fund.

A comparison on shareprice , indicates very little difference between the 2 accumulation funds with the distribution fund ( VWRL) slightly lower as one would expect.

Best done in an ISA to avoid declaration of Excess Reportable Income ( ERI).

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

monabri wrote:Best done in an ISA to avoid declaration of Excess Reportable Income ( ERI).

The HSBC fund is UK domiciled, so there is no excess reportable income. Nonetheless, outside a tax shelter, you could find yourself up a gum tree if you have large capital gains and the fixed fee platforms dry up.

-

monabri

- Lemon Half

- Posts: 8427

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1549 times

- Been thanked: 3443 times

Re: Portfolio Critique

GeoffF100 wrote:monabri wrote:Best done in an ISA to avoid declaration of Excess Reportable Income ( ERI).

The HSBC fund is UK domiciled, so there is no excess reportable income. Nonetheless, outside a tax shelter, you could find yourself up a gum tree if you have large capital gains and the fixed fee platforms dry up.

Then for a UK investor investing outside of a tax sheltered account, would the HSBC fund above be more suitable than Vanguard's VWRP (and cheaper)?

I started to read a document from Canaccord Genuity Wealth Management (I've no association with them) which discusses ERI. It is a fairly complicated area when it comes to things like "relevant taxable date" for non tax sheltered accounts (as I see it, it is 6 months after the fund's reporting period is when the ERI is treated as being earned income - example, a UK resident holds investments in XYZ fund whose last day of its reporting period is 31st December 2021 will be deemed to have received the income on 30th June 2022 and thus the distribution would be included as taxable income in the 2022-2023 tax return). The information should be stated/found on a consolidated tax voucher. Then there is the subject of "equalisation" when investors buy funds part way through a fund's accumulation period. Thus one can reduce the declared income on a tax return but the amount needs to be checked via the fund manager (website).

edit: Just seen this

viewtopic.php?p=467982#p467982

-

Hariseldon58

- Lemon Slice

- Posts: 835

- Joined: November 4th, 2016, 9:42 pm

- Has thanked: 124 times

- Been thanked: 514 times

Re: Portfolio Critique

monabri wrote:Hariseldon58 wrote:For the OP I’d just go for an All World tracker.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

This one?

ISIN GB00BMJJJF91

https://www.hl.co.uk/funds/fund-discoun ... cumulation

.

Yes, thats the one, I hold this in an ISA. I have happily held VWRL in a taxable account but have been disposing of it over several years now, in CGT allowance sized chunks, which is a testament to a happy holder !

I wouldn’t expect there to a significant difference in performance over time. Ideally the lower charges should help a little over a long period but it also lowers my exposure to ETFs and Vanguard products.

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

monabri wrote:Then for a UK investor investing outside of a tax sheltered account, would the HSBC fund above be more suitable than Vanguard's VWRP (and cheaper)?

VWRP is expensive. It is cheaper to use:

VHVG VANGUARD FUNDS PLC FTSE DEVELOPED WORLD UCITS ETF 0.12% cost – 90% allocation

VFEG VANGUARD FUNDS PLC FTSE EMERGING MARKETS UCITS ETF 0.22% cost - 10% allocation

That works out at 0.13%, which is the same cost as the HSBC fund. Working out the ERI is not a problem, and there are no dividends to declare separately with these accumulation funds. You will have to calculate the equalisation with purchases of the HSBC fund, which is no easier than working out the ERI. The risk of holding that fund is that HSDL and II will follow the crowd and charge percentage platform fees for holding open ended funds like the HSBC one. That leaves ShareDeal Active, but would you want to invest (say) seven figures with Jarvis? Perhaps Vanguard will reduce its charges, but that would be no good if you are stuck in the HSBC fund. There are plenty of cheap platforms for ETFs, so you can sleep easy with those. You should not be ambushed with exorbitant charges.

-

Newroad

- Lemon Quarter

- Posts: 1096

- Joined: November 23rd, 2019, 4:59 pm

- Has thanked: 17 times

- Been thanked: 343 times

Re: Portfolio Critique

You're a hard man, Geoff.

Calling VWRP "expensive" Though it's no doubt true compared to some (including your own suggested combination) in a relative sense.

Though it's no doubt true compared to some (including your own suggested combination) in a relative sense.

I'm happy to keep VWRP (SIPP) and VWRL (ISA/JISA) - at some price point, simplicity has it's merits.

Regards, Newroad

Calling VWRP "expensive"

I'm happy to keep VWRP (SIPP) and VWRL (ISA/JISA) - at some price point, simplicity has it's merits.

Regards, Newroad

-

mark85

- Posts: 15

- Joined: January 13th, 2022, 8:04 pm

Re: Portfolio Critique

Hariseldon58 wrote:For the OP I’d just go for an All World tracker.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

Thank you for all the great advice. I think I will actually go with this. Seems very straightforward and easier to manage rather than buying multiple components vhvg/vfeg etc and with ii can set up monthly investment and just leave it ticking over for years.

-

Hariseldon58

- Lemon Slice

- Posts: 835

- Joined: November 4th, 2016, 9:42 pm

- Has thanked: 124 times

- Been thanked: 514 times

Re: Portfolio Critique

mark85 wrote:Hariseldon58 wrote:For the OP I’d just go for an All World tracker.

There is an HSBC All World tracker at .13% pa, it’s a fund but there are no costs to hold with ii.

A very small bias to EM and Europe is likely to make very little difference, I wouldn't overthink it, just invest monthly, year in and year out, you’ll get there.

Thank you for all the great advice. I think I will actually go with this. Seems very straightforward and easier to manage rather than buying multiple components vhvg/vfeg etc and with ii can set up monthly investment and just leave it ticking over for years.

Thats a good plan but you need to keep doing it through thick and thin !!!

I remember doing this through the dot com era, ignoring the obviously ( to me) over priced in 1999 and seeing everything go down in the crash that followed, keeping the faith and still investing every month, it worked out well !!! Good luck.

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

Newroad wrote:Calling VWRP "expensive"

Lets put some numbers in here. VWRP costs an extra 0.09%. On £1 million, that amounts to £1,000,000 * 0.09 / 100 = £900. That is a lot of money to give up every year to save a little work.

-

Newroad

- Lemon Quarter

- Posts: 1096

- Joined: November 23rd, 2019, 4:59 pm

- Has thanked: 17 times

- Been thanked: 343 times

Re: Portfolio Critique

Not arguing about the numbers, Geoff.

Although my VWRL/VWRP holdings are a little more modest than £1M

Just wondering whether your choice of adjective might have had an accompanying adverb.

Regards, Newroad

Although my VWRL/VWRP holdings are a little more modest than £1M

Just wondering whether your choice of adjective might have had an accompanying adverb.

Regards, Newroad

-

GeoffF100

- Lemon Quarter

- Posts: 4760

- Joined: November 14th, 2016, 7:33 pm

- Has thanked: 178 times

- Been thanked: 1377 times

Re: Portfolio Critique

Newroad wrote:Not arguing about the numbers, Geoff.

Although my VWRL/VWRP holdings are a little more modest than £1M

Just wondering whether your choice of adjective might have had an accompanying adverb.

Regards, Newroad

Perhaps "painfully" would be appropriate if your holdings are large enough.

-

Newroad

- Lemon Quarter

- Posts: 1096

- Joined: November 23rd, 2019, 4:59 pm

- Has thanked: 17 times

- Been thanked: 343 times

Re: Portfolio Critique

Maybe, Geoff.

Maybe.

Or, a bit like the Buffett 90/10 plan for his wife, maybe one wouldn't (need to) care?

Who knows? Not me, yet at least, anyway.

Regards, Newroad

Maybe.

Or, a bit like the Buffett 90/10 plan for his wife, maybe one wouldn't (need to) care?

Who knows? Not me, yet at least, anyway.

Regards, Newroad

-

mark85

- Posts: 15

- Joined: January 13th, 2022, 8:04 pm

Re: Portfolio Critique

GeoffF100 wrote:An argument in favour of a home bias is precisely that it has done badly in the past decade. The hope is that the old technology stocks that dominate the FTSE 100 are now less overpriced than the growth stocks that now dominate the global index, and that the FTSE 100 will outperform as a result. Nevertheless, it is probably best to trust the market and buy the market, i.e. about 0.9*VHVG + 0.1*VFEG. That is simpler too.

iWeb is cheaper than II, and is likely to be at least as safe. With a relatively small portfolio, by the standards of this board, you could afford to go with Freetrade. It is unlikely that they will go bust, and you will almost certainly be paid out in full by the FSCS if they do.

Was having a look at iweb, appears to have some poor reviews online but maybe this is more to do with simplistic platform it offers. Going with HSBC All World tracker at .13% pa how many trades would be optimal per year?

ii allows monthly investment with total yearly cost £120 a year or £1200 over 10 year period.

iweb - £100 opening fee, then £5 for each trade. Assuming quarterly investment rather than monthly, works out at £120 opening year then £20 a year each subsequent year. Over 10 year period works out at £300 total which is signifcantly cheaper.

Who is online

Users browsing this forum: Pendrainllwyn and 29 guests